/>i

/>iOn August 25, the SEC adopted rules1 implementing the pay for performance disclosure mandated by the Dodd-Frank Act. The rules, originally proposed in 2015 and subject to a reopened comment period earlier this year, require a company to disclose, in a proxy or information statement with executive compensation disclosure, how compensation actually paid related to company financial performance over a five-year period (or three-year period in the case of a smaller reporting company). These new disclosure requirements, which are intended to provide investors with more transparent, readily comparable and understandable disclosure of a company’s executive compensation, do not apply to emerging growth companies, registered investment companies, or foreign private issuers.

Tabular Disclosure – New Item 402(v) of Regulation S-K

Pay Versus Performance

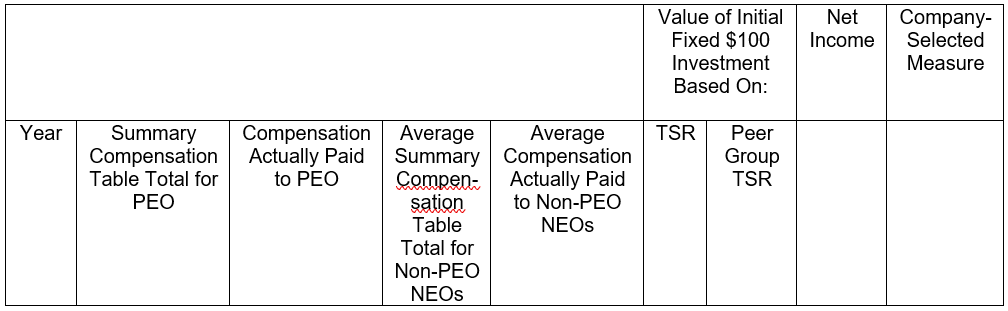

The new pay for performance table requires disclosure of the following items for the applicable period:

-

Summary Compensation Table Total for the Principal Executive Officer (PEO) (adding a column for each other PEO if there was more than one PEO during the fiscal year)

-

Compensation Actually Paid to the PEO (adding a column for each other PEO if there was more than one PEO during the fiscal year). The rules require adjustments to the amount reported in the Summary Compensation Table to:

-

deduct the aggregate change in actuarial present value of the executive’s accumulated benefit under all defined benefit and actuarial pension plans;

-

add, for all defined benefit and actuarial pension plans reported, the aggregate of “service cost” and “prior service cost” (as such terms are defined in the final rules, and in each case calculated in accordance with U.S. GAAP); and

-

deduct the grant date fair values reported for stock and option awards, and add fair values of these awards with other modifications intended to better align the timing of the disclosure and valuation with when each award is actually earned by the executive (in an effort to more clearly show the relationship between executive compensation and the company’s performance).

-

-

Average Summary Compensation Table Total for Non-PEO Named Executive Officers

-

Average Compensation Actually Paid to Non-PEO Named Executive Officers. The rules require the same adjustments with respect to pension benefits and equity awards described in the second bullet above regarding compensation actually paid to the PEO.

-

Company Total Shareholder Return (TSR) and Peer Group TSR, generally calculated in the same manner as done for the performance graph included in the company’s annual report.

-

Company Net Income

-

Company-Selected Measure, which in the company’s assessment represents the most important financial performance measure (that is not otherwise required to be disclosed in the table) used by the company to link compensation actually paid to the company’s named executive officers, for the most recently completed fiscal year, to company performance.

A company will also have to disclose in footnotes to the table: (i) each of the amounts deducted and added to arrive at compensation actually paid to the PEO and the other named executive officers; (ii) the names of the PEO and other named executive officers and the fiscal years in which they are included; and (iii) the assumptions made in the valuation of any equity awards that differ materially from those disclosed as of the grant date of such equity awards. The final rules permit, but do not require, that the new disclosure be provided in a company’s Compensation Discussion and Analysis section of the proxy statement.

Additional Disclosure – Graphic, Narrative or Combined

A company is also required to provide a clear description – graphically, narratively, or a combination of the two – of the relationship between:

-

Executive compensation actually paid by the company to the PEO and the average of the executive compensation actually paid by the company to the named executive officers other than the PEO, and each of the following measures (across the applicable period):

-

Cumulative TSR of the company;

-

Company Net Income; and

-

the Company-Selected Measure; and

-

-

Cumulative TSR of the company and cumulative TSR of the company’s peer group over the same period.

Tabular List

Finally, a company is also required to provide a tabular unranked list of at least three, and up to seven, financial performance measures, which in the company’s assessment represent the most important financial performance measures used by the company to link compensation actually paid to the company’s named executive officers, for the most recently completed fiscal year, to company performance. The tabular list may be provided in three different ways:

-

As one comprehensive list;

-

As two separate lists (presenting the PEO and other named executive officers separately); or

-

As separate lists for the PEO and each other named executive officer.

If the company used less than three financial performance measures, the list must include all measures used, if any. A company may include non-financial performance measures if it determines that they are among the most important performance measures (and the company has otherwise disclosed the most important financial performance measures).

Companies are also permitted to voluntarily provide supplemental measures of compensation or financial performance (in the table or in other disclosure) or other supplemental disclosures, as long as any such measure or disclosure is clearly identified as supplemental, not misleading and not presented with greater prominence than the required information.

Next Steps

Most companies will have to include the pay for performance disclosure, using Inline XBRL, in their proxy statements to be filed in 2023, as compliance is required for proxy and information statements with executive compensation disclosure for fiscal years ending on or after December 16, 2022. Of note, companies other than smaller reporting companies will only be required to provide information for three years (instead of five years) in the first proxy or information statement in which they provide the pay for performance disclosure; these companies will be required to add another year of disclosure in each of the next two annual proxy statements for which this disclosure is required. Smaller reporting companies will only be required to provide information for two years in their first proxy or information statement; these companies will be required to add another year of disclosure in the next annual proxy statement. Given the complexities of the calculations and disclosures, companies should begin assembling the information to populate the new pay for performance table and begin the process of identifying the Company-Selected Measure and other measures to be presented in the tabular list, along with the explanatory graphic, narrative or combined disclosure.

FOOTNOTES

1 See Pay Versus Performance, available at https://www.sec.gov/rules/final/2022/34-95607.pdf (August 25, 2022).