/>i

/>iOn 19 May 2021, the financial industry taskforce of Singapore (known as the Green Finance Industry Taskforce (GFIT)) released guidelines on climate-related disclosures and a white paper on green finance solutions.1 Convened by the Monetary Authority of Singapore (MAS), GFIT’s overarching objective is to accelerate green finance in Singapore through four key initiatives:

-

develop a taxonomy,

-

enhance environmental risk management practices of financial institutions,

-

improve disclosures, and

-

foster green finance solutions. The white paper contains a proposed framework on green trade facilities and working capital, catering for banks, asset managers, and insurers in Singapore (Financial Institutions).

This article explores the impact of the suite of green documentation on Financial Institutions, corporates, non-governmental organizations, and financial industry associations, and explains how the new measures may affect green finance risks and opportunities in Singapore and ASEAN. The latest developments build on the country’s efforts to improve the long-term resilience of its financial markets to the impact of environmental risks and, at the same time, foster environmentally sustainable growth.

The Green Finance Opportunity

According to the Climate Bonds Initiative, global green bond and green loan issuance reached over US$258 billion in 2019, expanding over 50 percent compared to 2018.2

Financial Institutions may unlock green finance opportunities in renewables, water resources, green buildings, waste, the circular economy, and transportation (including aviation, shipping, and e-mobility). One example is Deutsche Bank’s green financing of Avation’s aircraft to Braathens Regional Airlines in 2020, replacing older jets with modern alternatives emitting 40 percent less CO2. According to the International Finance Corporation, there is a US$23 trillion climate investment opportunity in emerging markets between now and 2030.3

The contours of green finance solutions continue to evolve, potentially involving preferred shares, bonds, loans, insurance solutions, carbon services, and asset management. Regardless of the structure, the underlying transaction must have a positive impact on environmental issues, such as climate change, biodiversity, pollution, or changes in land use. Sustainable financing, in contrast, has a broader remit and takes into account environmental, social, and governance (ESG) factors.

Challenges such as greenwashing—a green illusion brought about by the promulgation of green financing—have led regulators to seek to impose stricter standards in an attempt to strengthen the green finance market and remove barriers. The draft Singapore taxonomy, referenced below, should play an important role in improving definitions, emulating previous efforts in the European Union.4

The flow of capital to fossil fuel projects has been seriously limited, with over 20 global financial institutions announcing new coal finance restrictions in the first few months of 2021 (out of a total of 145).5

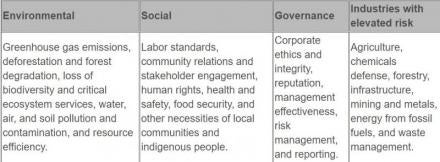

Scope of Responsible Financing6

Accelerating Green Finance in Singapore

Issuers raised US$3.5 billion of green bonds in Singapore in 2020, carrying the label of ‘ASEAN Green Bond’ or otherwise aligned with the Association of Southeast Asian Nations (ASEAN) Green Bond Standards. The Singapore government will boost this number going forward, announcing approximately US$14 billion of green bonds (in equivalent Singapore dollars) in the Singapore Budget 2021.

As Financial Institutions adjust the pricing of loans and investments to reflect increasing environmental risks, MAS expects that this will unlock new green financing opportunities, in turn helping to increase the flow of capital into green/transition projects.

MAS has asked Financial Institutions to implement the MAS Guidelines on Environmental Risk Management of December 2020 (the ENRM Guidelines)7 by June 2022. The ENRM Guidelines encourage Financial Institutions to improve resilience against the impact of environmental risks, providing a pathway for Financial Institutions to integrate such risks into their business and risk management strategies.8 Further to the ENRM Guidelines, GFIT issued the “Handbook on Implementing Environmental Risk Management for Financial Institutions” on 28 January 2021.

The Singapore Green Plan 2030 recognizes the important role that banks and nonbank financial institutions play in a low-carbon future, further to Singapore’s Paris Agreement commitments, ratified on 21 September 2016.9 Beyond the domestic market, Singapore has an opportunity to be an anchorage for green financing, using regional connections and its status as a global financial hub to reach a broad range of markets in ASEAN and globally.

Government initiatives and support will be critical to support the growth of green finance in Singapore. On 24 November 2020, for example, MAS launched the Green and Sustainability-Linked Loan Grant Scheme to defray expenses incurred by corporates to engage independent sustainability assessment and advisory services providers.

Key Features of White Paper on Fostering Green Solutions

GFIT’s white paper of 19 May 2021 describes the challenges and opportunities for Financial Institutions in the emerging area of green finance and proposes solutions and pilot projects to accelerate progress in Singapore. The white paper states that sustainable trade financing along the value chain is a potential US$26 billion opportunity over the next 10 years and includes an industry framework for green and sustainable finance and working capital solutions to define eligibility and reporting. GFIT has identified the establishment of a robust framework for Financial Institutions as an immediate priority in order to address a gap in short-term ESG finance solutions.

The white paper supports the legitimacy of transition finance, particularly in the emerging markets of Asia given the region’s role as the world’s manufacturing and production hub. Transition finance involves financing incremental improvements (towards decarbonization) by very high-polluting and fossil fuel-reliant corporates, and GFIT sees this as a compliment to green, social, or sustainable development goal labels. Government-led support, such as commercial risk cover, is a key to developing transition finance together with subsidies to defray the cost incurred by borrowers for undertaking ESG ratings and surveillance.

Recognizing the nuances of industry sectors at different stages of the energy transition, GFIT adopts a sector-based analysis, identifying oil and gas, shipping, real estate, infrastructure, and fund management as initial ‘priority’ sectors, each with their own areas for development, incentives, and financial solutions.10

Many of GFIT’s sector sub-groups advocate a systematic, principals-based approach by Financial Institutions, anchored to a commonly accepted taxonomy and ideally backed up with a harmonized set of green principles applicable across ASEAN. The taxonomy is important to improve credibility and investor confidence and mitigate the risks of green washing, which will otherwise continue to undermine efforts to accelerate growth. GFIT issued a consultation paper on the draft Singapore taxonomy on 28 January 2021.

Financial solutions may include transition loans, transition bonds, equity, and venture capital, as well as securitization for financing sustainable infrastructure.12 For real estate and infrastructure, seed capital and technology-enabled green platforms and marketplaces may help developers of ESG opportunities connect with lenders and allow projects to be aggregated and monitored, perhaps using artificial intelligence and machine learning, in order to achieve better scale.

The degree of complexity required to implement the steps to achieve target outcomes for each sector is likely to be substantial, requiring a large amount of coordination between stakeholders. Although there is an opportunity to secure favorable loan terms for accretive green projects, corporates have suggested that the difference in the cost of borrowing may not be attractive enough, and in some cases, there is a lack of motivation. Evidence that Asia is lagging behind other regions is clearest in the fund management sector, where total Q4 2020 global sustainable fund flows for Asia ex-Japan was US$5 billion, compared to US$120.8 billion for Europe. However, in some areas, such as infrastructure securitization, there is a potential opportunity for Asia to become a leader.

Next Steps

From Q2 2021, the MAS will engage with Financial Institutions on the implementation of the ENRM Guidelines. The process of implementation will continue to evolve, as global collective action and engagement is refined and harmonized. Early progress, led by the private sector, may avoid disruptive mitigation measures in the future.

Aligning with the Taskforce on Climate-related Financial Disclosures, the ENRM Guidelines provide recommendations for Financial Institutions to identify risks from climate change and to improve the standard of climate-related financial disclosures. Singapore Exchange Limited requires all listed companies to report on sustainability, on a “comply or explain” basis, to support more transparent ESG disclosures.

Financial Institutions and other stakeholders may participate in the consultation for the draft Singapore taxonomy, described in the white paper as a guiding document that will support many aspects of green finance in Singapore. The taxonomy attempts a broader classification on what is sustainable and the criteria to use in ascertaining the differences between green finance, sustainable finance, and other jargon from a Singapore perspective—a yardstick for Financial Institutions to measure up against and ensure that their financial solutions are truly as green and sustainable as they claim to be and adhere to reporting requirements.

Together with the ASEAN Green Bond standards, the Singapore taxonomy and new guidelines and disclosure requirements are likely to improve the certification of green financial instruments and enhance credibility. Financial Institutions may adopt the proposed framework for green trade finance and short-term facilities, prepared by GFIT and set out in its white paper of 19 May 2021. GFIT will also undertake capacity-building activities to improve implementation outcomes and encourage leadership and collaboration.

Conclusion

The new measures provide welcome guidance as the financial and investment markets pivot towards a more sustainable approach, supported by new reporting and transparency requirements for Financial Institutions and other investors. The Singapore taxonomy, once finalized, will be an important step towards mitigating the risks of green washing and hopefully will set a level of harmonization across ASEAN, taking into account the requirements of financiers, borrowers, and investors alike.

Footnotes

1 https://abs.org.sg/industry-guidelines/responsible-financing.

2 https://www.climatebonds.net/resources/reports/2019-green-bond-market-summary.

4 A taxonomy regulation was published in the Official Journal of the European Union on 22 June 2020 and entered into force on 12 July 2020. It establishes the framework for the EU taxonomy by setting out four overarching conditions that an economic activity has to meet in order to qualify as environmentally sustainable. See: https://ec.europa.eu/info/law/sustainable-finance-taxonomy-regulation-eu-2020-852_en.

5 https://ieefa.org/finance-leaving-thermal-coal/.

6 Source: ABS Guidelines on Responsible Financing Release Version 1.1.

7 https://www.mas.gov.sg/regulation/guidelines/guidelines-on-environmental-risk-management.

8See Related Content.

9 Singapore submitted its enhanced climate pledge, or Nationally Determined Contribution, and Long-Term Low-Emissions Development Strategy to the United Nations Framework Convention on Climate Change on 31 March 2020.

10 The five sectors were prioritized by GFIT following consultation with industry players.

11 The white paper mentions the example of the Bayfront pilot securitization of 37 project and infrastructure loans domiciled in the Asia Pacific and Middle East regions. Securitized notes were issued by a special purpose vehicle named Bayfront Infrastructure Capital.