/>i

/>iWe previously wrote about Charitable Remainder Trusts (CRTs) (1), focusing on the beneficial impact of higher IRS 7520 rates. These are coming down, but they are still attractive. In July, the 7520 rate was

5.61 %, and the current (October 2024) rate is 4.45% (2).

Here, after a brief review of CRTs in general, we will focus on the four main flavors of Charitable Remainder Unitrusts (CRUTs). While we are lacking fresh data, the IRS reported in 2012 that Charitable

Remainder Unitrusts continued to be the most common split-interest trusts, accounting for

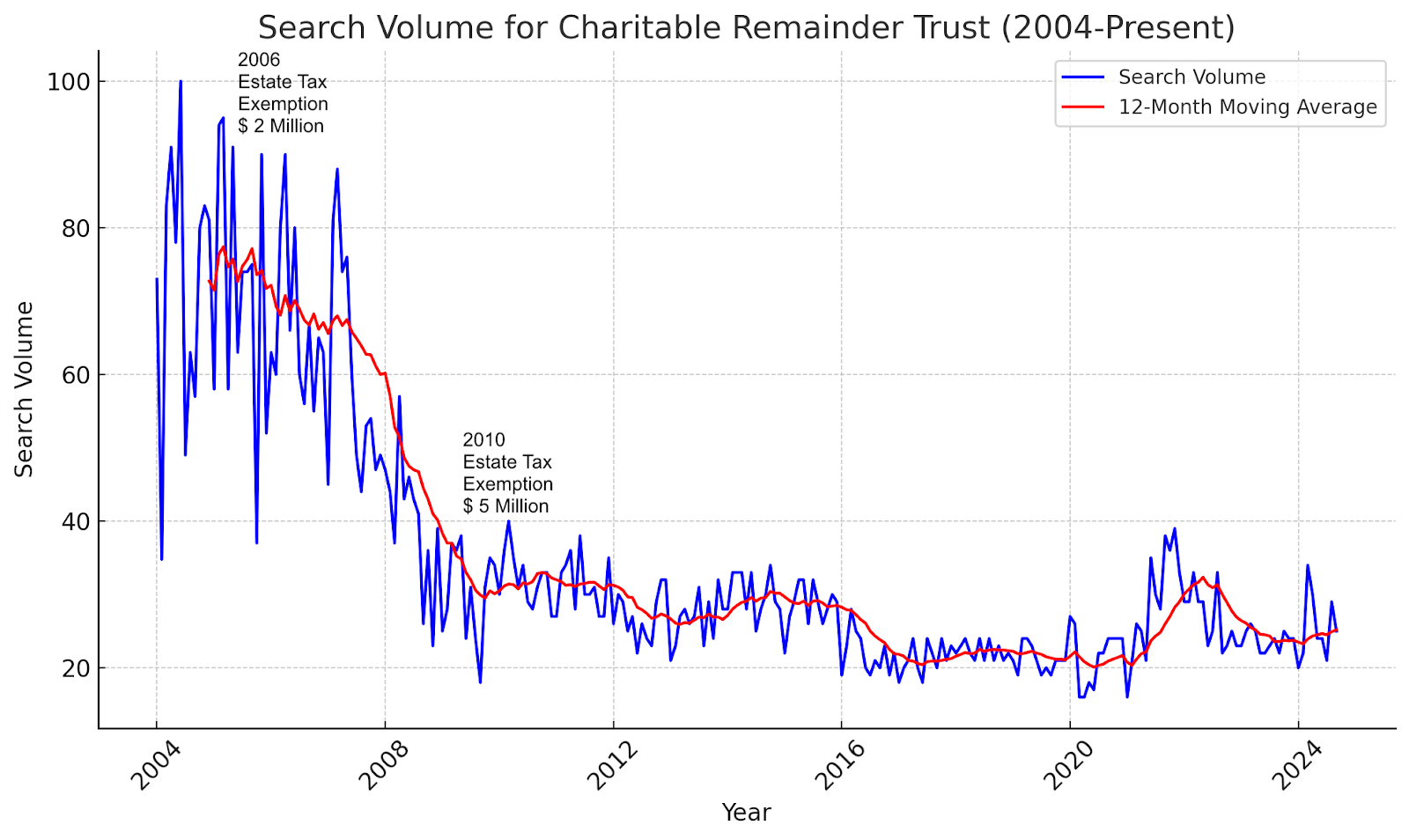

more than three-quarters (80.3 percent) of 113,688 such returns filed in 2012 (3). This was at a time of very low (and therefore unattractive) 7520 rates. The range in 2012 was between 1.0 and 1.6% (4). Given the recent high interest rates and generally increasing net worth, the number of CRUTs should have increased, but we don’t have new IRS data. A look at the Google search volumes for the term Charitable Remainder Trusts does not show a recent convincing uptick in interest in CRTs. Instead, interest in CRTs seems to have decreased with increasing estate tax exemption rates and appears flat since 2010 (Figure 1). Therefore, given the potential benefits of income tax savings (as opposed to avoiding estate taxes), CRUTs seem to be underutilized.

Figure 1: Google searches for Charitable Remainder Trusts have been flat since 2010 (5)

Why Charitable Remainder Trusts?

Establishing a Charitable Remainder Trust (CRT) offers an immediate income tax deduction, the size of which is influenced by the IRS Section 7520 rate. All other things being equal, a higher 7520 rate results in a larger deduction.

The extraordinary performance of stocks like NVIDIA and Tesla over the past five years has led to significant wealth accumulation, often resulting in concentrated stock positions. While diversifying these holdings would typically trigger substantial capital gains taxes, a CRT allows for tax-free diversification. The CRT can sell highly appreciated assets without incurring capital gains tax, enabling growth from a larger principal.

Key Advantages of a Charitable Remainder Trust:

- Tax Efficiency on Asset Sales: CRTs provide an avenue for selling and diversifying highly appreciated assets without triggering capital gains taxes, preserving more wealth within the trust for future growth.

- Income Provision: The trust offers lifetime or term-certain income to the donor, providing either financial security or supplemental income during retirement.

- Immediate Tax Deduction: Upon establishing the CRT, the donor receives an immediate charitable deduction for the present value of the remainder interest designated for charity.

- Charitable Contribution: After the donor’s death or the end of the trust term, the remaining trust assets are distributed to one or more charitable organizations, aligning with the donor’s philanthropic objectives.

- Estate Tax Benefits: Since the remainder interest is irrevocably designated for charity and the donor cannot control or access it, these assets are excluded from the donor's estate, potentially reducing estate tax liability.

This combination of tax efficiency, income generation, and charitable giving makes CRTs a compelling tool for high-net-worth individuals seeking to diversify concentrated asset positions while supporting charitable causes. Let us now examine the different subtypes of CRTs in detail.

1. Standard Charitable Remainder Unitrust (SCRUT)

When to Use:

- Steady Growth Assets: Ideal for assets like a balanced stock portfolio or blue-chip stocks, where the donor anticipates steady appreciation. These assets regularly increase the trust's value, which in turn increases the payments to the beneficiary over time.

- Desire for Increasing Payments: Beneficiaries who expect their income needs to grow later in life (such as for retirement or increasing healthcare costs) will benefit from the way a SCRUT ties payments to asset value.

- Inflation Protection: The potential for annual payouts to increase makes a SCRUT a good choice for those concerned about inflation eroding their purchasing power.

Example Use Case:

An individual contributes $1,000,000 in growth stocks to a SCRUT with a 5% annual payout. As the portfolio grows to $1,200,000 over a few years, the beneficiary’s payout increases from $50,000 to $60,000 per year, providing inflation adjustment and increasing income.

Integration with Financial Planning:

A SCRUT offers flexibility by allowing the beneficiary to benefit from asset appreciation, aligning well with strategies focused on wealth accumulation and distribution planning. It's particularly useful when coordinating with a donor's broader retirement or legacy planning, offering a balance between current income and preserving wealth for charitable purposes.

2. Net Income Charitable Remainder Unitrust (NICRUT)

When to Use:

- Income-Only from Earnings: A NICRUT is preferable when the donor wants the beneficiary to only receive distributions from trust income (like interest, dividends, or rents) rather than the principal. This makes it suitable for assets like income-generating real estate or dividend-paying stocks.

- Illiquid or Non-Income Producing Assets: When the trust is funded with assets like vacant land or closely-held businesses that don't produce regular income, a NICRUT prevents the trust from being forced to make distributions when there is no income.

- Income Flexibility: Beneficiaries who don't require regular, predictable income can benefit from the income-only distribution model of the NICRUT, as distributions fluctuate with trust income.

Example Use Case:

A donor places rental real estate into a NICRUT. In years when rental income is high, the beneficiary receives more significant payouts; in years with vacancies, the payouts may be reduced, allowing the trust to avoid selling assets to make payments.

Integration with Financial Planning:

This option aligns with asset protection and tax deferral strategies. NICRUTs allow donors to avoid liquidation of illiquid assets while still securing charitable tax deductions. It is useful when planning for beneficiaries who might have varying income needs over time, such as in periods of transition (e.g., during retirement, career changes).

3. Net Income with Makeup Charitable Remainder Unitrust (NIMCRUT)

When to Use:

- Uncertain Income with Deferral Possibility: A NIMCRUT is suitable when the donor expects variable income or delayed returns from the trust's assets, such as in the case of early-stage companies or real estate investments. The "makeup" provision allows for larger payouts in future years to account for earlier shortfalls.

- Timing Income for Later Needs: Beneficiaries who don’t need immediate income but expect to require more significant payouts in the future—perhaps in retirement—can benefit from a NIMCRUT’s ability to defer distributions and then make up the shortfall in years when income exceeds the payout requirement.

- Delay or Defer Payouts: Younger donors or beneficiaries planning for future financial needs may find the NIMCRUT especially appealing, as they can defer distributions while allowing assets to grow and compound.

Example Use Case:

A donor contributes shares in a startup to a NIMCRUT. In the early years, the company does not pay dividends, and little income is generated, so payouts are minimal. When the startup starts producing revenue or is sold, the NIMCRUT compensates for prior low payouts, providing a larger income in later years.

Integration with Financial Planning:

NIMCRUTs are particularly beneficial for clients who seek to maximize income during retirement or other periods of high need. By allowing beneficiaries to accumulate payouts for future use, it integrates well with estate planning strategies that aim to delay income until tax rates are lower or until higher income is needed, such as during retirement.

4. Flip Charitable Remainder Unitrust (FLIP-CRUT)

When to Use:

- Transition from Illiquid to Liquid Assets: The Flip-CRUT is ideal when donors wish to contribute illiquid assets like real estate, art, or a privately held business that may not generate immediate income. The trust can "flip" to a standard CRUT when these assets are sold, allowing the beneficiary to receive a more consistent payout after the triggering event.

- Flexibility for Illiquid Assets: This is particularly useful when a donor's portfolio consists of illiquid assets. The trust avoids forcing the sale of such assets to make distributions, allowing the trust to flip only after liquidity is achieved.

- Tax Deferral: By deferring the "flip" until the sale of illiquid assets, donors can time their income recognition more favorably from a tax perspective, particularly in cases where income can be recognized in a lower tax bracket year or when capital gains can be minimized.

Example Use Case:

A donor contributes a valuable piece of real estate to a Flip-CRUT. Initially, the trust operates as a NICRUT, paying out net income, which is minimal while the real estate is unsold. Once the property is sold, the trust flips to a standard CRUT, and the beneficiary begins receiving a fixed percentage of the now-liquidated trust assets.

Integration with Financial Planning:

A Flip-CRUT is especially useful for donors with concentrated positions in real estate or other illiquid assets. It aligns well with a strategy that focuses on wealth diversification, allowing the donor to contribute illiquid assets and still provide for a future income stream once liquidity is achieved. The timing flexibility also integrates with broader tax and estate planning strategies, offering tax efficiency while transitioning from illiquid to liquid wealth.

Each CRUT variation serves a unique purpose, depending on the donor’s goals, asset types, and income needs. By choosing the right type, donors can effectively plan for their financial future while contributing to charitable causes, optimizing their tax benefits, and providing for beneficiaries in a flexible manner.

Key Considerations for Choosing the Right CRUT

- Income Needs: If steady income is required, SCRUT might be better. If the donor is comfortable with fluctuating income or can defer, a NICRUT, NIMCRUT, or Flip-CRUT could be more appropriate.

- Asset Type: Illiquid or non-income-producing assets, such as real estate, favor NICRUT, NIMCRUT, or Flip-CRUT structures, as they allow for more flexibility in payout timing.

- Tax Efficiency: NIMCRUTs and Flip-CRUTs allow deferral of income, which can result in favorable tax timing, especially when tied to the sale of appreciated assets.

- Growth vs. Income: If the trust assets are expected to appreciate significantly, a SCRUT might allow the beneficiary to benefit from rising payments over time.

Here’s a detailed table summarizing the different types of Charitable Remainder Unitrusts (CRUTs) and when they may be preferable:

| Type of CRUT | Description | When to Use | Example Use Case |

|---|---|---|---|

| Standard Charitable Remainder Unitrust (SCRUT) | Pays a fixed percentage of the trust's revalued assets annually. |

- Steady Growth Assets: Assets are expected to grow steadily. - Desire for Increasing Payments: Beneficiaries want income that can rise with the value of trust assets. - Inflation Hedge: Payments increase if assets appreciate. |

A trust funded with a portfolio of steadily growing stocks, where the beneficiary receives 5% of the annual value, increasing as the trust’s assets grow. |

| Net Income Charitable Remainder Unitrust (NICRUT) | Pays the lesser of a fixed percentage or the actual net income generated by the trust. |

- Income Only from Earnings: Beneficiaries prefer receiving only what the trust earns, avoiding principal. - Illiquid Assets: The trust holds assets like real estate or businesses that may not produce consistent income. - Variable Income Flexibility: Income varies with asset performance. |

A trust funded with rental properties or other income-generating assets, where the beneficiary receives payouts based on the rental income generated by the properties. |

| Net Income with Makeup Charitable Remainder Unitrust (NIMCRUT) | Pays the lesser of the fixed percentage or actual income but allows for "makeup" of unpaid amounts in future years if income increases. |

- Uncertain Income with Deferral: The beneficiary prefers to defer income and potentially receive larger payments later. - Delayed or Deferred Payouts: Assets may not produce income initially but could generate more later. - Makeup Provision: Shortfall in payments can be made up later. |

A trust funded with shares in a startup, where income is low initially, but as the startup grows and generates dividends, the trust can "make up" for previous lower payouts. |

| Flip Charitable Remainder Unitrust (Flip-CRUT) | Starts as a NICRUT or NIMCRUT and "flips" to a standard CRUT after a triggering event (e.g., sale of an illiquid asset). |

- Transition from Illiquid to Liquid Assets: The trust holds illiquid assets initially, like real estate or closely held businesses. - Tax Deferral: Deferring larger payouts until a triggering event helps manage tax liabilities. - Flexibility for Asset Sales: The flip occurs after an event. |

A trust funded with appreciated real estate that pays based on income from rents until the property is sold, after which it flips to a standard CRUT, paying a fixed percentage of the trust’s value. |

Table 2: Types of CRUTs compared.

Conclusion

Charitable Remainder Unitrusts (CRUTs) offer a highly customizable and tax-efficient solution for donors looking to balance philanthropic goals with financial planning. By tailoring the choice of CRUT to the donor's specific asset types, income needs, and long-term objectives, advisors can provide bespoke solutions that maximize both charitable impact and financial benefits. Whether the goal is to generate steady income, defer taxes, or strategically manage illiquid assets, CRUTs offer flexibility and significant tax advantages, making them an underutilized yet powerful tool for high-net-worth individuals. Depending on the outcome of the national election and subsequent tax legislation, CRTs may also be of interest again for clients primarily interested in estate tax savings.

Podcast

References

- Klaus Gottlieb, Charitable Remainder Trusts: Get Them While They Are Hot This Summer, Nat’l L. Rev. (July 5, 2024), https://natlawreview.com/article/charitable-remainder-trusts-get-them-while-they-are-hot-summer

- Internal Revenue Service, Section 7520 Interest Rates, https://www.irs.gov/businesses/small-businesses-self-employed/section-7520-interest-rates (last visited Sept. 26, 2024).

- Internal Revenue Service, SOI Tax Stats - Split-Interest Trust Statistics, https://www.irs.gov/statistics/soi-tax-stats-split-interest-trust-statistics (last visited Sept. 26, 2024).

- Internal Revenue Service, Section 7520 Interest Rates for Prior Years, https://www.irs.gov/businesses/small-businesses-self-employed/section-7520-interest-rates-for-prior-years (last visited Sept. 26, 2024).

- Google Trends, Explore: Charitable Remainder Trust, https://trends.google.com/trends/explore?date=all&geo=US&q=Charitable%20Remainder%20Trust&hl=en (last visited Sept. 26, 2024).