/>i

/>iEducation represents one of the most powerful investments families can make, with benefits extending far beyond the individual student. When our estate planning clients think about funding education, they often have tunnel vision and only consider grandchildren and their basic post-secondary education. Various publications feed into this narrow perspective, even comparing the lifetime income benefit of various majors (STEM comes out on top, liberal arts are last).

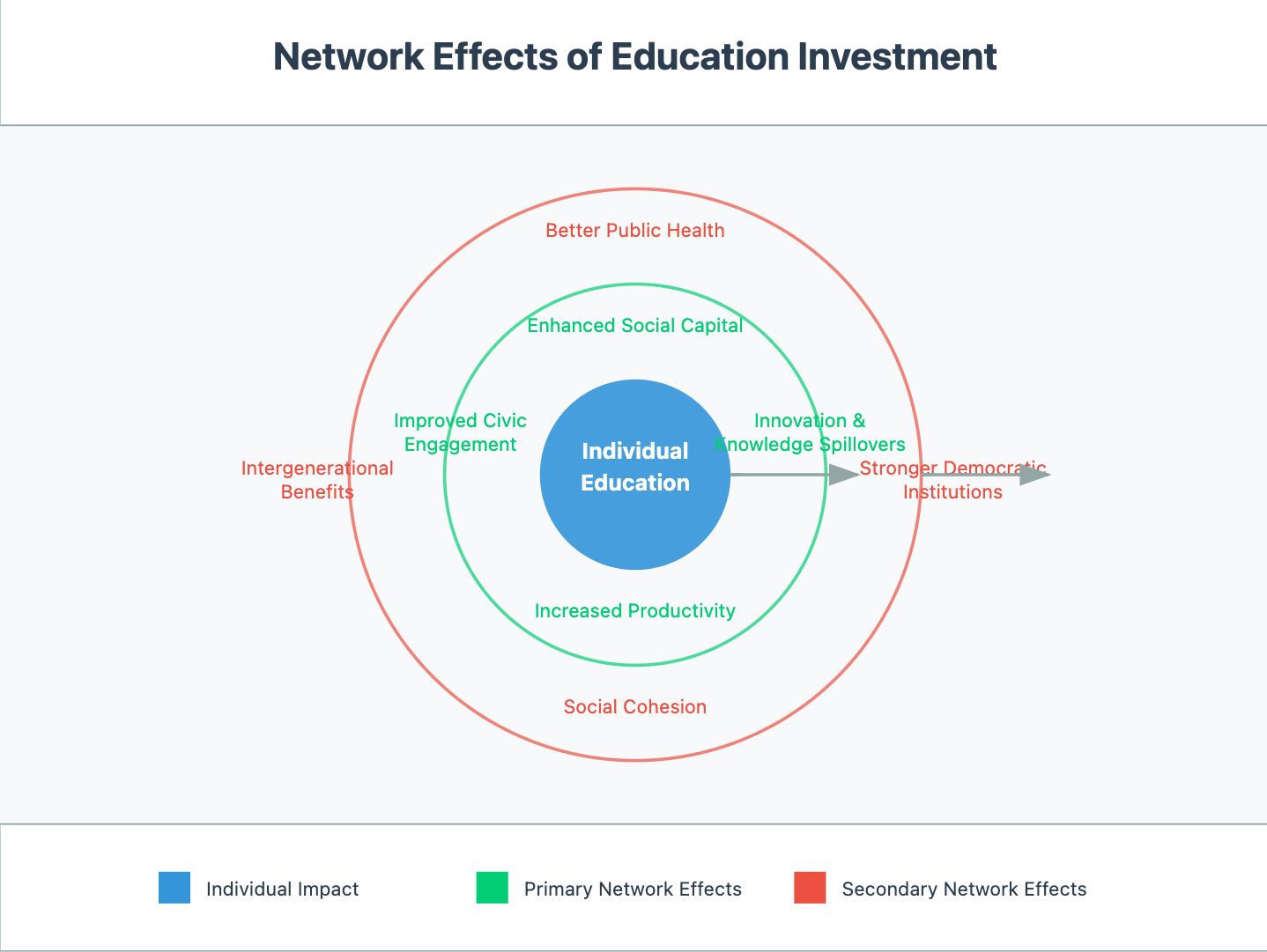

Network Effects of Education

While more difficult to quantify, sending parents and even grandparents back to school may have ripple or network effects. Social network theory, combined with Coleman's work on intergenerational resource conversion and Bourdieu's cultural capital framework (1), suggests that educational investments create multiplicative effects across social networks and generations. When family members pursue education, they build both human and cultural capital that can be transmitted through social ties while simultaneously strengthening those network connections. This theoretical foundation helps explain why educational investments often yield benefits far beyond the direct recipient, as enhanced cultural capital and more robust social networks facilitate resource sharing, knowledge transfer, and the development of educational aspirations across the extended family system.

I always ask my clients who have altruistic motives but don’t see any suitable education candidates to look a bit further, even consider themselves. For example, your client can create a 529 plan for his or her benefit and later change the beneficiary designation to someone else. This is a common and flexible strategy used by many 529 plan account owners.

Even if your client decides to use the plan for their own education, perhaps pursuing a long-held dream of finally getting a Master's in Art History, there are benefits beyond the gratification of a personal hobby. The personal example exerts a long-lasting influence on the perceptions and aspirations of the younger family members.

Figure 1: Education of the individual has intergenerational benefits.

Direct Tuition Payments: A Powerful Tax-Free Transfer Strategy

One of the most straightforward and effective strategies is making direct tuition payments to educational institutions. Under IRC § 2503(e), these payments are exempt from gift tax and don't count against the donor's lifetime gift tax exemption or annual gift tax exclusion.

This option is particularly valuable for clients with potentially taxable estates. The gift must be paid directly to the educational institution, for tuition only (not books, supplies, or room and board) and for someone other than the donor/payer, but it is otherwise unlimited. There is no impact on other gifting strategies, and direct tuition payments are available for any level of education (K-12, college, graduate school).

529 Plans: Flexible Education Funding with Estate Planning Benefits

The modern 529 plan traces its origins to the Michigan Education Trust (MET) in 1986, the first prepaid tuition program. The broader 529 plan system as we know it today was formally established by federal law in 1996 by adding section 529 to the tax code.

The Economic Growth and Tax Relief Reconciliation Act (EGTRRA) of 2001 exempted the earnings of a Section 529 plan from federal income tax instead of deferring the tax on the undistributed earnings. The Tax Cut and Jobs Act of 2017 (TCJA) allows distributions from 529 plans to be used to pay up to a total of $10,000 of tuition per beneficiary each year at an elementary or secondary (k12) public, private or religious school of the beneficiary’s choosing (2).

In addition, contributors can make a lump-sum contribution to a 529 plan and elect to spread it over five years for gift tax purposes. In 2024, an individual can contribute up to $90,000 ($180,000 for married couples filing jointly) in a single year to a beneficiary's 529. This strategy allows contributors to make larger gifts without triggering federal gift taxes or reducing their lifetime gift tax exemption.

Recent changes, including the SECURE Act 2.0 provisions, allow for tax-free rollovers of unused funds from a 529 plan to the beneficiaries' Roth IRAs. Certain restrictions apply.

Despite the numerous benefits, surveys indicate that many potential users remain unaware of how 529 plans function and their expanded uses. For instance, around 50% of adults surveyed were unfamiliar with what a 529 plan is, highlighting ongoing educational needs in this area (3).

Prepaid Inflation-Protected 529 Plans

The Private College 529 Plan offers an alternative to traditional college savings methods by allowing families to lock in current tuition rates at participating private colleges for future use. This program, launched in 2003, involves nearly 300 private institutions, including Georgetown, Princeton, and Stanford.

While traditional 529 plans invest in mutual funds that become more conservative as college approaches, the Private College 529 Plan works differently. Parents can contribute throughout the plan year (July 1 to June 30) and receive tuition certificates tied to that year's rates. These certificates become redeemable 36 months after the first deposit and remain valid for 30 years. The financial impact can be significant. For example:

A $10,000 investment for an 8-year-old could save $4,803

Prepaying a full year ($40,000) saves $19,210

Prepaying four years ($160,000) saves $91,434

(Based on $40,000 annual tuition at inception with 4% yearly increases)

The program remains relatively small, with $334 million in assets compared to $408 billion in traditional 529 plans as of early 2023. The average account size is $45,000. Partial prepayment is possible, though the remaining tuition will be charged at future rates. Tax benefits apply at both federal and state levels. The savings are tax-free when used for education, and some states, including Arizona and Pennsylvania, offer additional tax breaks for contributions. Other states limit tax advantages to in-state plan contributions.

A handful of states operate their own prepaid tuition programs, but these typically require state residency and apply only to public in-state schools. In contrast, the Private College 529 Plan requires no residency requirements but is limited to participating private institutions (4).

Coverdell Education Savings Accounts

A Coverdell Education Savings Account (ESA) is a tax-advantaged investment account for education expenses that, while offering tax-free growth and withdrawals for qualified expenses (including K-12 costs), comes with significant limitations compared to 529 plans. The most notable restrictions are its low annual contribution limit of just $2,000 per beneficiary, income limits for contributors, the requirement that funds must be used by the beneficiary's 30th birthday, and the rule that contributions must stop when the beneficiary turns 18 (unless they have special needs). Given these constraints, many families opt for 529 plans instead, which offer higher contribution limits, no age restrictions, no income limits for contributors, and similar tax advantages, making them generally more flexible for long-term education savings.

Trusts for Education

When a 529 plan proves too restrictive, various trust structures offer enhanced flexibility to address a beneficiary's broader needs beyond education. However, it's important to note that these alternatives generally don't match the tax-free growth advantage of 529 plans for qualified education expenses.

Among these alternatives, Irrevocable Education Trusts can be especially effective for families desiring an education-focused trust that still allows funds to cover related living expenses or health needs. Contributions to such trusts may qualify for the annual gift tax exclusion, with income generated either taxed at the trust level or passed through to the beneficiary, depending on distribution patterns.

A Revocable Living Trust offers another flexible alternative for clients who wish to retain control over the assets and the option to modify terms over time. As a revocable structure, this trust allows the grantor to adjust the trust's provisions or even dissolve it as family circumstances evolve, offering more responsive asset management than a 529 plan's rigid framework.

For clients who prefer greater specificity with tax advantages, there are two distinct options: a Crummey Trust or a Minor's Trust (2503(c) Trust). A Crummey Trust includes withdrawal powers, allowing beneficiaries limited annual withdrawal rights and qualifying contributions for the annual gift tax exclusion while offering distributions for broader purposes beyond education. Separately, a Minor's Trust requires all assets to be distributed to the beneficiary by age 21 but offers more straightforward gift tax treatment without requiring Crummey withdrawal notices.

Discretionary Trusts also provide flexibility, enabling a trustee to determine the timing and scope of distributions based on the beneficiary's needs. A trustee's discretion allows distributions for education, healthcare, or maintenance, making these trusts particularly adaptable across varying circumstances. Alternatively, a HEMS (Health, Education, Maintenance, and Support) Trust aligns distributions with these categories while maintaining sufficient breadth to meet a beneficiary's diverse life needs.

For clients seeking to tailor support beyond education, each of these structures can accommodate evolving needs while offering strategic estate and tax planning benefits. The optimal choice often involves balancing the tax advantages of 529 plans with the flexibility offered by trust structures.

Conclusion

Estate planning for education requires looking beyond traditional college savings approaches. The available tools each serve distinct purposes: 529 plans offer superior tax advantages and new flexibility through Roth IRA rollovers, prepaid tuition programs provide inflation protection, direct tuition payments allow unlimited tax-free transfers, and various trust structures accommodate broader life needs beyond education.

More importantly, education investments create multiplicative effects across family networks and generations. Whether funding young students' college education or supporting adult family members' educational pursuits, these investments build both human and cultural capital that benefit the entire family system.

The most effective strategies combine multiple approaches, balancing tax efficiency with flexibility while considering the broader impact of educational investments across generations. Success lies in matching the right combination of tools to each family's unique circumstances and aspirations.

Podcast:

References:

- Raymond Sin-Kwok Wong, Multidimensional Influences of Family Environment in Education: The Case of Socialist Czechoslovakia, 71 Sociology of Education 1, 1–22 (1998), available at https://www.jstor.org/stable/2673219.

- I.R.S. Pub. 5834, Qualified Tuition Programs – IRC Section 529 (Feb. 2024), available at https://www.irs.gov/pub/irs-pdf/p5834.pdf.

- Remy Samuels, 529 Plans Continue to Grow in Popularity, But More Education is Needed, PLANSPONSOR (May 31, 2024), https://www.plansponsor.com/529-plans-continue-to-grow-in-popularity-but-more-education-is-nee.

- Ashlea Ebeling, The Little-Known Way Parents Are Beating College Tuition Hikes, Wall St. J. (June 23, 2023), https://webreprints.djreprints.com/2407085.html.