/>i

/>iIntroduction

-

Intervener in AAR application cannot seek ruling through another application on same transaction in the absence of specific leave from AAR.

-

AAR’s power to reject application not restricted to grounds mentioned in proviso to section 245R (2); can reject where material facts not disclosed.

-

AAR will look at entire series of events and not restrict itself to events in year in which relevant transaction took place when determining issue of prima facie tax avoidance or exemption under tax treaty.

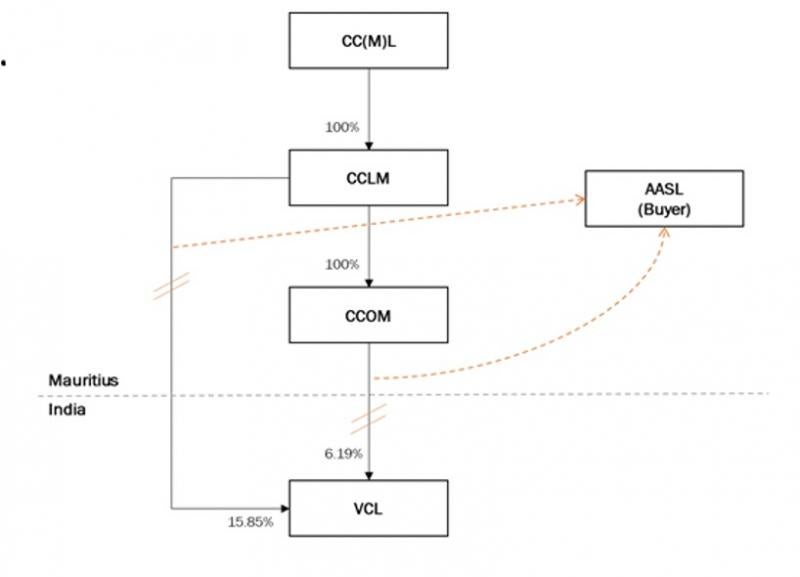

The Mumbai bench of the Authority for Advance Rulings (“AAR”), in a ruling passed in October 2019, rejected the applications1 (“Applications”) made by two Mauritian entities (“Applicants”), i.e. Capex Com Limited (“CCOM”) and Capex Communications Ltd. (“CCLM”). The Applications sought to ascertain taxability in India of capital gains arising to the Applicants from sale of shares of an Indian company, Vortex Capex Ltd. (“VCL”), under the Income Tax Act, 1961 (“ITA”) read with the India – Mauritius Double Taxation Avoidance Agreement (“India – Mauritius DTAA”). The AAR held the applications to be non-maintainable on the basis that (a) certain material facts had not been disclosed, (b) an order allowing withdrawal of the previous AAR applications in which the Applicants were interveners, and that did not give specific leave to the Applicants to file fresh AAR applications, was binding on the Applicants and did not leave room for the Applicants to file fresh applications, and (c) the transaction was prima facie a scheme for tax avoidance.

Background

The Applicants are part of the Capex group which participated in the telecom business in India along with the Marsh group of Hong Kong. In 2004, the Capex group underwent internal restructuring post which CCOM acquired 6.19% shareholding of VCL using funds from third party lenders and from its holding company. Capex Telecom Investments Limited (“CTIL”), another group company in India, held 15.85% stake in VCL. In 2006, CCLM infused funds in CTIL obtained from its holding company (which funds were in turn obtained from a third party lender), and became its 100% shareholder. CTIL thereafter went into voluntary liquidation pursuant to a condition in the lending agreement between CCLM’s holding company and the third-party lenders, making CCLM the direct owner of 15.85% VCL shares.

In 2010, Aura Atlantic Sec. Ltd. (“AASL”), an entity resident in Mauritius, had filed an application before the AAR seeking a ruling on its withholding liability under the ITA read with the India-Mauritius DTAA on a proposed purchase of the shares of VCL held by CCOM and CCLM (“Previous Application”). AASL had been nominated to acquire VCL’s shares. In May 2011, CCOM and CCLM had applied as interveners in the Previous Application, which request was allowed by the AAR.

In June and July 2011, the Applicants sold their shares in VCL to AASL. AASL paid sale consideration to the Applicants after deducting tax at source, which it deposited with Government of India under protest. AASL thereafter filed an application for withdrawal and accordingly the Previous Application was ‘dismissed as withdrawn’ by the AAR. Significantly, this withdrawal order was “without prejudice to the right of the applicant, the Revenue and the Interveners to put forward whatever contentions they have at appropriate stage in other proceedings, in accordance with law”.

Subsequently in September 2012, the Applicants filed the present Applications before the AAR seeking a ruling as to whether the transaction of sale of shares of VCL was taxable in India in light of the India - Mauritius DTAA, and whether the Revenue should refund the tax at source deducted by AASL. The AAR admitted the Applications keeping the objections of the Revenue open for consideration during the final hearing.

Arguments by Revenue

The Revenue argued that:

-

The Applicants had not disclosed their participation as interveners in the Previous Application, hence the Application should be dismissed on the sole ground of suppression of material facts.

-

The Applicants’ admission as interveners in the Previous Application put them in the same position as an ‘applicant’ in the Previous Application. Hence, per section 245S, the withdrawal order was binding on applicants (which would include the interveners). Since the ruling dismissed the Previous Application as withdrawn, this was binding on the interveners as well and they could not agitate another application before the AAR but only “other” proceedings.

-

Even otherwise it was argued that the term ‘respondent’ includes ‘intervener’2, and the withdrawal order was binding on the respondent as well under section 245S of the ITA.

-

Notices under section 133(6) of the ITA had been issued to the Applicants during the proceedings pertaining to AASL which tantamount to ‘pending proceedings’ for the Applicants hit by clause (i) of the proviso to section 245R(2) of the ITA.

-

Although the Applicants held Tax Residency Certificates (“TRCs”) for Mauritius, they had no involvement in the decisions that were in fact taken by the Capex group personnel in India implying their control and management was wholly in India. The present transaction fell within the carve out in Vodafone3 for cases where a subsidiary does not have sufficient autonomy, and in support the Revenue subjected the transaction in question to the various tests laid down in Vodafone. On basis of this, the Revenue contended that the Applicants were used as colourable devices to avoid taxes in India, which was hit by clause (iii) of the proviso to section 245R(2) of the ITA.

Arguments by Applicants

-

The Applicants argued that the Applications involved a simple case of exemption claim under the India-Mauritius DTAA that the Applicants were entitled to on account of their TRCs read with Circular No. 789 of 2000, and the fact that the Applicants were control and managed from outside of India.

-

While the Applicants admitted their failure to disclose their role in the Previous Application, they stated it was an inadvertent omission rather than suppression and no prejudice was caused to the revenue as the facts were known to them.

-

The Applicants argued that the decision to withdraw the Previous Application was of AASL only and not of the Applicants and as interveners they had no right to prevent withdrawal of the application. Further, it was also contended that the purpose of intervention was limited to address arguments in support of AASL.

-

The withdrawal order is not a ‘ruling’ per section 245R(4) of the ITA as it did not involve determination of the questions posed before the AAR. Further, the rights available to an applicant are not available to an intervener, hence the intervener cannot be considered to be on the same pedestal as the Applicant. The Applicants also argued that questions raised in both the applications were different as the present one did not make any reference to withholding taxes.

-

In any case, the meaning of ‘other proceedings’ in the withdrawal order, would have meant other proceedings before the AAR itself as the AAR was not required to grant permission with respect to proceedings before other forums. Therefore, specific permission to file before the AAR had been granted by the withdrawal order.

-

The AAR can reject an application only for grounds provided under proviso to section 245R(2)4 of the ITA.

-

The Applicants argued that for the purpose of clause (iii) to the proviso of section 245R(2) of the ITA, there should be prima facie tax avoidance, which revenue failed to establish. Even otherwise, placing reliance on Vodafone, it was argued that there exist a conceptual difference between “series of preordained transactions” created for tax avoidance purposes, on one hand, and a transaction which evidences investment to participate in India, and the current transaction satisfies all the parameters of investment to participate. Further, it was also argued that since capital gains arose in the financial year 2011-12, hence the details provided by revenue should be ignored as they relate to years 2001 to 2007 and the bench should restrict to activities related to relevant assessment year.

Ruling

The AAR held that the Applicants had omitted the fact of their intervention in the Previous Application in Form 34C of the present Applications that required disclosure of all relevant facts, for fear that if all facts were disclosed the Applications may be rejected at the initial stage itself. The facts pertaining to the Previous Application were held to be relevant to the current Application, and hence their non-disclosure rendered the Applicants’ verification in Form 34C incorrect. On this basis itself, the AAR held that the Applications were liable to be rejected.

The AAR also held that the question raised in the Application was squarely covered in the Previous Application and the withdrawal order passed therein was binding on the Applicants under section 245S of the ITA. The AAR placed reliance on Nuclear Power Corporation of India Ltd., In re5 where it was held that an advance ruling is a determination in relation to a transaction, and a transaction always involves a payer and a payee, thereby rejecting the argument of the Applicants that each party had its individual remedy before the AAR. Notably, the AAR noted that Applicants had not sought specific permission to file a fresh application, and the withdrawal order did not give the Applicants such liberty. The AAR further opined that the phrase ‘other proceedings’ in the withdrawal order could not possibly mean a fresh application before the AAR, as that would imply that even AASL was permitted to file such a fresh application.

The AAR also agreed with the ruling in Microsoft Operations Pte. Ltd., In re6 cited by the Revenue that its power to reject an application is not restricted to three specified situations under the proviso to section 245R(2) of the ITA. It rejected the Applications for (a) suppression of material facts, and (b) the question raised related to the same transaction as in the Previous Application and there was no liberty to file a new application in the withdrawal order.

The AAR further observed that the withdrawal of the Previous Application was pursuant to a commercial arrangement between AASL and the Applicants, and the Applicants could not now claim that the withdrawal was a unilateral act of AASL.

On the question of the bar under clause (i) of proviso to section 245R(2), the AAR rejected the section 133(6) argument raised by the Revenue as the notices contained no question on the taxability of capital gains on the shares of VCL, hence no ‘question’ remained pending.

Lastly, with respect to the transaction being prima facie designed for tax avoidance, the AAR concurred with the Revenue’s arguments on the basis that the acquisition of shares of VCL were not done using the Applicants’ own funds, but the Applicants were bound by restrictive covenants of loan agreements, post-sale consideration was immediately transferred, and the voluntary liquidation of CTIL was done with the sole purpose to move situs of shares to Mauritius. Further, the AAR observed that the scheme of tax avoidance presupposes a series of events which might have been planned for a few years and thereafter the desired event occurs leading to the intended tax benefit, thereby rejecting the Applicants’ argument to limit the inquiry to the activities of the financial year in which transaction took place.

Analysis

The ruling has touched upon some interesting aspects of procedural law in the advance ruling mechanism. The withdrawal order passed by the AAR was considered an advance ruling for the purpose of section 245S of the ITA, and not a withdrawal under section 245Q(3) . Section 245S renders binding an ‘advance ruling pronounced’ by the AAR under section 245R. A reference to the text of section 245R makes clear that an ‘advance ruling’ is only a ruling passed under section 245R(4) that opines on the ‘question specified in the application’, and would not extend to any other order passed by the AAR. Within this statutory framework, the AAR’s position in equating an order of withdrawal of an application with an advance ruling under section 245R(4) seems questionable, as the withdrawal order is not an advance ruling on the question specified in the application. This interpretation also renders otiose section 245Q(3). Furthermore, since the amendment of section 245S vide the Finance Act, 2021, even advance rulings passed under section 245R would no longer be binding on the applicants or the revenue. Thus, the AAR’s finding regarding the withdrawal order would no longer be a valid interpretation under the amended section 245S.

With respect to withholding tax obligations, the AAR ruled that a ruling/order passed in the matter of a payee or a payor will subsequently bind the other party as well, as the binding authority of a ruling is not only qua a party but qua the transaction. This raises certain issues as often, particularly in a transaction involving unrelated parties, one party has no control over the decision of the other party to approach the AAR. While there is an argument to be appreciated (as made in Nuclear Power Corporation) that since the underlying facts involved are the same, the pendency of the question in the case of one party should act as a bar to an AAR application by the other party, as otherwise there is a potential of having different rulings by different authorities on the same set of facts. However, the application of this rationale to a situation where the proceeding in the case of the other party has been withdrawn, and hence there is no live proceedings pondering the same question, is not founded on the same logic. In fact, this amounts to a denial of a process otherwise available under the ITA to a taxpayer/withholder, without any sound rationale.

As mentioned, the Finance Act, 2021 seeks to replace the Authority of Advance Rulings with the Board for Advance Rulings, and a notification on the rules of procedure for the Board is awaited. It remains to be seen whether these aspects will be addressed in such rules.

Apart from the procedural grounds, the AAR also sought to reject the Applications under clause (iii) of the proviso to section 245R(2). The AAR held that the transaction entered into by the Applicants was prima facie designed for tax avoidance. In arriving at this, the AAR makes certain troubling statements to the effect that the shares in VCL were acquired by CCLM on account of voluntary liquidation of CTIL, and the sole purpose of this was to transfer the situs of ownership of shares of VCL to Mauritius to avoid Indian capital gains tax. This statement ignores the fact that (a) any transfer of ownership of shares of an Indian entity would necessarily involve capital gains tax implications, and (b) such capital gains tax may be exempt under a tax treaty, such as the India-Mauritius DTAA in the present case, which cannot then be a basis to conclude on tax avoidance. It appears to be a circular argument to say that a claim of treaty benefit is not permissible because of tax avoidance, while that very claim of a treaty benefit is regarded as a basis to conclude on the existence of tax avoidance. Not to mention, that taken to its logical conclusion, this would imply that every claim of a tax treaty benefit would then amount to an attempt at avoiding tax. It is interesting to note that the AAR has also ruled on similar lines in Tiger Global International II Holdings, In re7 which also involved taxability of capital gains under India Mauritius DTAA, however, that ruling has been challenged and is currently pending adjudication before the Delhi High Court.

1 A.A.R. No. 1373 & 1374 of 2012

2 Supreme Court of India Rules, Notification GSR 367(E) & GSR 368(E) dated 27.05.2014

3 Vodafone International. Holding B.V. v UOI (2012) 341 ITR 1 (SC)

4 The three reasons for rejection of an AAR application specified under the proviso to Section 245R are (i) the question raised is already pending before any income-tax authority or appellate tribunal or court, (ii) the question involves determination of fair market value, or (iii) the question relates to a transaction or issue which is designed prima facie for the avoidance of income tax.

5 [2012] 343 ITR 220 (AAR – New Delhi)

6 [2009] 310 ITR 408 (AAR)

7 [2020] 429 ITR 288 (AAR - New Delhi)