/>i

/>i

I. Introduction

On July 26, 2019, the IRS announced that it was in the process of sending letters to over 10,000 taxpayers with a history of cryptocurrency transactions by the end of August, noting that the letters were sent to taxpayers who, “potentially failed to report income and pay the resulting tax from virtual currency transactions or did not report their transactions properly.” The announcement also notes that the IRS is heightening its scrutiny of cryptocurrency activity, including increased use of data analytics. However, guidance remains lacking on many key issues affecting the taxation of cryptocurrency transactions.

These letters are the latest development in IRS’ ongoing efforts to enforce the taxation of cryptocurrency transactions. Accordingly, this article provides context for the issuance of these letters, covering some of the background developments concerning IRS’ efforts to collect tax on cryptocurrency transactions. We then discuss the content of these letters and the potential implications of such letters. Finally, we touch on the need for IRS to issue additional guidance.

II. Background

In 2014, the IRS published Notice 2014-21, the only guidance it has issued to date on the taxation of cryptocurrency transactions.[1] While this question and answer format guidance is not extensive, it did answer certain base questions concerning the federal taxation of cryptocurrency. Namely, that the IRS treats cryptocurrency as property and not as currency. As such an exchange of one cryptocurrency for another (e.g. Bitcoin for Ethereum) is considered a taxable transaction, as is an exchange of cryptocurrency for fiat currency or goods or services. A recipient of cryptocurrency is obligated to include the fair market value of the cryptocurrency received in income as of the date such cryptocurrency was received.

The “tax basis” that a taxpayer has in cryptocurrency it receives is the fair market value of the cryptocurrency in U.S. dollars (USD). If the cryptocurrency received is listed on an exchange, its fair market value is generally determined by the applicable exchange rate on the date of receipt.[2] Upon a subsequent disposition of cryptocurrency, the gain or loss for federal income tax purposes is recognized based upon the difference between the value in USD of the item received in exchange and the taxpayer’s basis in the cryptocurrency. The character of the gain or loss on cryptocurrency will generally depend on whether the cryptocurrency is considered a capital asset or an ordinary income asset, such as inventory or property held for sale to customers in the ordinary course. Thus, cryptocurrency would generally be a capital asset in the hands of an investor, but may be an ordinary income asset in the hands of a dealer.

In the case of a taxpayer that mines cryptocurrency as a trade or business (a miner), IRS stated that the fair market value of the cryptocurrency as of the date of receipt is includible in gross income. Additionally, the net earnings would be subject to the self-employment tax. Although the IRS did not address the recovery of expenses, related expenses should offset gross income from crypto mining activities, subject to general income tax conventions and limitations such as the requirement to capitalize certain expenses.

Finally, the IRS provided that a person paying cryptocurrency to an independent contractor for the performance of services is required to report such payment equal to the IRS and to the payee on Form 1099-MISC. In addition, the IRS provided that third party settlement organizations (TPSOs) are required to report payments made to merchants on Form 1099-K if, during the relevant calendar year, both (1) the number of transactions settled for the merchant exceeded 200 and (2) the gross amount of payments made to the merchant exceeded $20,000.00. A TPSO is a third party intermediary that contracts with a substantial number of unrelated merchants to settle payments between the merchants and their customers. This could include, for example, crypto exchanges and some crypto wallet providers.[3]

Despite the issuance of this guidance, the IRS believes that rampant underreporting of cryptocurrency transactions has continued. Accordingly, in 2016, the IRS served the digital currency exchange Coinbase with a “John Doe” summons seeking extensive information with respect to U.S. taxpayers who conducted transactions in a convertible virtual currency, as defined in IRS Notice 2014-21, during the calendar years 2013-2015. When Coinbase refused to comply, the IRS brought a petition to enforce its request.

In the court battle that ensued, evidence was introduced to the effect that Coinbase had at least 5.9 million customers served and 6 billion transactions.[4] However, while 83-84% of relevant returns were filed electronically, the IRS was able to locate only 800 to 900 taxpayers a year that filed electronic returns with a property description related to Bitcoin during the summons period. In response to the IRS’ amended summons request covering only transactions with U.S. customers over $20,000.00, Coinbase acknowledged that this would still cover 8.9 million Coinbase transactions and 14,355 Coinbase account holders. Based on this evidence, the court agreed that it was reasonable to infer that more Coinbase users were trading Bitcoin than were reporting gains on their tax returns. Therefore, the court granted a partial victory to the IRS, requiring Coinbase to identify U.S. taxpayers with transactions of a value of at least $20,000.00 during the request period and to provide information on their account activity.

Thereafter, Coinbase and certain other crypto exchanges, wallets and credit card issuers began issuing Form 1099-K’s to account holders who met the threshold requirements for filing such forms.[5]

In 2018, the IRS published a notice reminding taxpayers that income from cryptocurrency transactions is reportable on their tax returns. The IRS threatened that non-compliance can be addressed through the audit process, which could result in penalties and interest or, in more extreme situations, criminal charges.[6] In addition, the IRS’s Large Business and International Division announced a virtual currency compliance campaign intended to address tax noncompliance related to the use of crypto currencies.[7] The IRS indicated that it would address this noncompliance, “through multiple treatment streams including outreach and examinations.”

The recently announced IRS letters appear to be an outgrowth of the Coinbase audit and the IRS’s virtual currency campaign. These letters provide educational content and, in some cases request compliance under the threat of examination. Below, we compare and discuss the content of the three letter variations.

III. Content of Letters

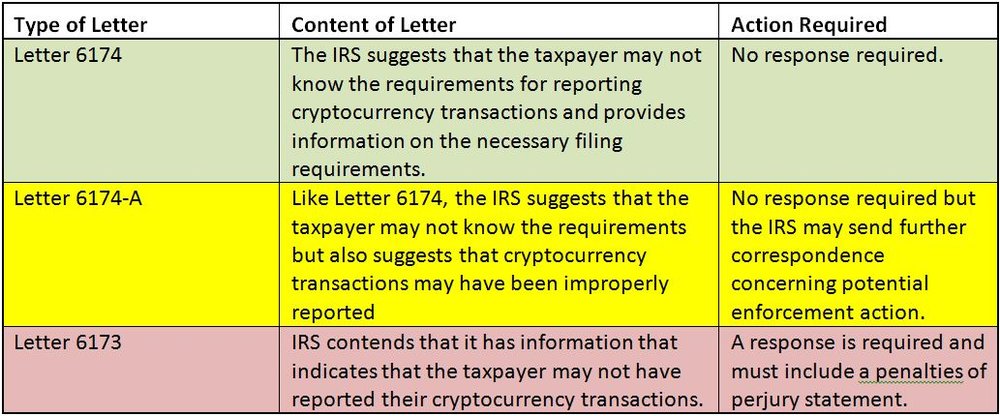

In its July 26, 2019 announcement, the IRS indicated that it was sending out three variations of its crypto letter: Letter 6173, Letter 6174 and Letter 6174-A. According to the IRS, “all three versions strive to help taxpayers understand their tax and filing obligations and how to correct past errors.”

Letter 6173 states that the IRS has information indicating that the taxpayer holds or has held one or more virtual currency accounts and, “may not have met its U.S. tax filing and reporting requirements for transactions involving virtual currency.” These letters state that, “[f]or one or more of tax years 2013 through 2017, we haven't received either a federal income tax return or an applicable form or schedule reporting your virtual currency transactions.” After providing some information on Notice 2014-21, the letter then states that the taxpayer should file the delinquent returns and report the virtual currency transactions, file an amended return, or send a statement of facts explaining the taxpayer’s position, including a complete history of previously reported income from its virtual currency transactions. Such statements must be signed and include a penalties or perjury statement. Finally, the letter indicates that if the IRS does not receive a response by the date stated in the letter, that the account will be referred for examination.

A taxpayer in receipt of Letter 6173 should contact their tax adviser immediately to determine how to respond. Since a response is required and must be accompanied by a “penalties of perjury statement”, careful consideration should be given to the content of such response.

Letter 6174, on the other hand, does not require a response. It states that IRS has information that the taxpayer had one or more accounts containing virtual currency but “may not know the requirements” for reporting transactions involving virtual currency. It then goes on to provide certain information on the taxation of virtual currency transactions, in line with the guidance provided in Notice 2014-21.

Letter 6174-A is much like Letter 6174 but states in its introduction that the taxpayer, “may not have properly reported” its transactions involving virtual currency. Like Letter 6174, Letter 6174-A does not require a response but adds the proviso that, “we may send other correspondence about potential enforcement activity in the future.”

Juxtaposing Letter 6174 with Letter 6174-A, it appears that the former is merely informational and perhaps sent to all taxpayers on whom the IRS has information indicating that they hold cryptocurrency accounts. Recipients of Letter 6174 may have reported all of their cryptocurrency transactions correctly and received the letter merely because they hold one or more cryptocurrency accounts. However, such taxpayers should review the reporting of their cryptocurrency transactions and the limited guidance provided in Notice 2014-21. On the other hand, the introduction to Letter 6174-A suggests that the IRS may disagree with the way a cryptocurrency transaction was reported on a taxpayer’s return. A taxpayer in receipt of a Form 6174-A Letter should consult with their tax adviser to determine whether such transactions were properly reported.

(Click to enlarge chart)

(Click to enlarge chart)

IV. Lack of Guidance

It is unfortunate that the IRS is taking action without first providing the guidance on some of the key outstanding tax issues, particularly for those taxpayers who reported their cryptocurrency transactions but may have taken a position at odds with the IRS’s unstated interpretation. As noted in our blog post on June 7, 2019[8], IRS Commissioner Charles Rettig indicated in a response letter to the Congressional Block Chain Caucus that the IRS would prioritize guidance on certain outstanding tax issues, including: (1) acceptable methods for calculating cost basis; (2) acceptable methods of cost basis assignment; and (3) the tax treatment of forks.[9] To date, however, no such guidance has been released.

There are many other areas where guidance from the IRS would be welcomed on the application of federal income tax rules to cryptocurrency transactions. Such areas include whether an exchange of one cryptocurrency for another can be treated as a like-kind exchange prior to the 2018 tax year,[10] the characterization of cryptocurrency as a commodity or a security for purposes of the mark-to-market and wash sales rules, in what circumstances does Section 1032 apply to the issuance of tokenized securities[11] and the proper application of international tax reporting requirements to holders of cryptocurrency and institutions which provide cryptocurrency accounts (e.g., wallet providers and exchanges).

V. Conclusion

As discussed above, taxpayers should carefully consider the content of the correspondence they receive from the IRS concerning cryptocurrency transactions and consult with a tax professional. Until the IRS issues guidance concerning open tax issues, taxpayers should deliberately consider how they report their cryptocurrency transactions. The lack of guidance in some areas presents both opportunities and risks.

[1] https://www.irs.gov/pub/irs-drop/n-14-21.pdf

[2] While not directly addressed in Notice 2014-21, general federal income tax principles indicate that when cryptocurrency received is not traded on an exchange, its fair market value should be measured by the value of the item the taxpayer paid or exchanged for the cryptocurrency (irrespective of whether that was fiat, another cryptocurrency or goods or services). See e.g., U.S. v. Davis, 370 U.S. 65 (1962).

[3] Interestingly, the IRS did not address whether and in what circumstances taxpayers such as crypto exchanges should file a Form 1099-B, which applies to (among other things) barter exchanges. Since the IRS considers cryptocurrency to be property, an exchange one cryptocurrency for another would seem on its face to constitute a barter exchange.

[4] These numbers appear to include all customers and all transactions, not just those of U.S. customers.

[5] https://news.bitcoin.com/coinbase-sends-american-clients-irs-tax-form-1099-k/

[6] https://www.irs.gov/newsroom/irs-reminds-taxpayers-to-report-virtual-currency-transactions

[7] https://www.irs.gov/businesses/irs-compliance-campaigns

[9] A hard fork is a change to the blockchain protocol that makes previously invalid blocks/transactions valid (or vice-versa). This results in a permanent divergence from the previous version of the blockchain, resulting in the existing cryptocurrency becoming two separate crypto currencies. See e.g., https://www.investopedia.com/terms/h/hard-fork.asp; https://cointelegraph.com/bitcoin-cash-for-beginners/what-is-hard-fork.

[10] H.R. 1, known as The Tax Cuts and Jobs Act of 2017, limited the application of the like-kind exchange rules to real estate transactions effective for exchanges completed after December 31, 2017.

[11] Section 1032 of the Internal Revenue Code of 1986, as amended, states that “[n]o gain or loss shall be recognized to a corporation on the receipt of money or other property in exchange for stock (including treasury stock) of such corporation.”