/>i

/>iWhile some may see the discovery and use of tax loopholes as a triumph of human ingenuity, others see their exploitation as an abuse of the tax code. The concepts developed here are complex but worth understanding if you want to use them for your clients or participate in the public discourse about related tax law reforms.

When anticipating significant appreciation of an asset, affluent taxpayers typically have two options: 1. transfer the property now (as a gift) to avoid estate taxes on future appreciation, or 2. transfer the property upon death to avoid income taxes on the appreciation. For each of these options, there is good news and bad news:

If the taxpayer gifts the property today, its value is fixed for transfer tax purposes as of the gift date per IRC Sec. 2512. This avoids transfer taxes on any future appreciation. However, the donee inherits the donor’s basis, often low, under IRC Sec. 1015 and will pay income tax on the appreciation when selling the property.

If the property is transferred at death, its value is determined at the date of death under Sec. 2031, capturing all appreciation for transfer tax purposes. The donee receives a stepped-up basis under IRC Sec. 1014, eliminating income tax on the appreciation that occurred before the donor’s death. However, the property is subject to the estate tax at its current fair market value.

In addition to the above, we need to mention an intermediate situation, the incomplete gift. An incomplete gift occurs when the donor retains certain powers or interests over the transferred property, which prevents the gift from being considered complete for tax purposes. This can have various implications, including the deferral of gift tax liability and the potential inclusion of the property in the donor's estate.

Tax Planning Conundrum: Wouldn’t it be nice if a taxpayer who has an estate large enough to be subject to estate taxes could do both: avoid capital gains taxes and avoid additions to the taxable estate due to appreciation? In other words, could one obtain a stepped-up basis for income tax purposes while also “freezing” the value of the wealth for transfer tax purposes?

Let’s hold that thought and review the Grantor Trust Rules. They determine when a trust is a grantor trust and when it is not, which in turn determines who pays income taxes. This will be important to solving the tax planning conundrum posed above.

Grantor Trust Rules

The distinction between a grantor trust and a non-grantor trust depends on whether the settlor (grantor) retains any incidents of ownership over the trust. If they do, it is a grantor trust; if they don’t, it's a non-grantor trust. Incidents of ownership can be any number of things by which control over the trust is exerted, for example, the right to change beneficiaries (Table 1).

As stated, in a grantor trust, the grantor maintains a certain degree of control over the trust’s assets or income. In contrast, non-grantor trusts include irrevocable trusts in which the grantor has relinquished control over the trust assets and does not retain any powers that would cause the trust to be treated as a grantor trust.

| Provision | Description |

| Power to Revoke (§ 676) | If the grantor has the power to revoke the trust and reclaim the trust assets, the trust is considered a grantor trust. |

| Power to Control Beneficial Enjoyment (§ 674) | If the grantor retains certain powers to control the beneficial enjoyment of the trust’s income or principal, the trust may be treated as a grantor trust. |

| Administrative Powers (§ 675) | If the grantor retains administrative powers that can affect the beneficial enjoyment of the trust, the trust may be considered a grantor trust. |

| Reversionary Interests (§ 673) | If the grantor retains a reversionary interest in the trust that exceeds 5% of the trust’s value, the trust is considered a grantor trust. |

| Income for the Benefit of the Grantor (§ 677) |

If the trust income is or may be used to pay premiums on insurance policies on the life of the grantor or the grantor’s spouse, the trust is treated as a grantor trust. If the trust income can be distributed to the grantor or the grantor’s spouse or held for future distribution to them, the trust is considered a grantor trust. |

Table 1: The most important grantor trust rules

The distinction between grantor and non-grantor trusts was made to determine who has to pay income taxes on the trust's income. In a grantor trust, it’s the grantor; in a non-grantor trust, it’s the trust.

The transfer tax and income tax regimes are closely aligned. When a grantor retains control over transferred property in a trust, they have a grantor trust. This property is generally considered owned by the grantor at death for estate tax purposes. For instance, if a grantor has the power to revoke a trust, Section 676 treats the grantor as owning the property for income tax purposes, and Section 2038 treats it as owned by the grantor at death for estate tax purposes. However, there is a loophole.

The Loophole - The Intentionally Defective Grantor Trust

An Intentionally Defective Grantor Trust (IDGT) is a type of trust designed to be treated as owned by the grantor for income tax purposes but not for estate tax purposes. This means that the income generated by the trust is taxable to the grantor, but the trust's assets are not included in the grantor's estate for estate tax purposes. To draft an IDGT, certain provisions must be included to ensure that the trust is considered defective for income tax purposes. These provisions typically involve intentionally violating one of the above grantor rules so that the trust is taxed on the trust's income.

A more descriptive name for an Intentionally Defective Grantor Trust (IDGT) could be "Swap Power Grantor Trust". The swap power is a common feature in the drafting of an Intentionally Defective Grantor Trust (IDGT). It allows the grantor to reacquire trust property by substituting other property of equivalent value. This power is crucial because it helps ensure that the trust is considered a grantor trust for income tax purposes while not causing the trust property to be included in the grantor's estate for estate tax purposes.

The "Swap Power" in Action:

- Income Tax Implications:

- Section 675: The swap power causes the grantor to be treated as owning the property for income tax purposes.

- No Corresponding Estate Tax Rule: There is no rule that includes this property in the grantor's estate for transfer tax purposes. Thus, the value of the property for transfer tax purposes is fixed at the time of the gift (Section 2512).

Transferring Property to the Trust:

- Initial Transfer:

- When the grantor transfers property to a trust with a swap power, the property is valued for gift and estate tax purposes as of the date of the gift, which freezes its value.

- Appreciation:

- Inside the trust, after the transfer, the property may enjoy unlimited appreciation; however, its value for estate tax purposes remains "frozen" at the time of the gift.

Income Tax Treatment of Transactions with the Trust:

- Disregarded Transactions:

- Under Section 675, transactions between the grantor and the trust (due to the swap power) are disregarded for income tax purposes.

- Exercise of Swap Power:

- When the grantor exercises the swap power (exchanging property within the trust), it is seen as moving assets between the grantor’s own "pockets," so there are no income tax consequences.

Basis and Tax Implications:

- Carryover Basis Rule (Section 1015):

- Normally, the basis of the gifted property carries over to the donee, meaning any appreciation is subject to income tax when the property is sold.

- Stepped-Up Basis (Section 1014):

- By using the swap power, the grantor can transfer appreciated low-basis property out of the trust and high-basis property of the same value into the trust.

- The appreciated property is back in the grantor's hands. When the grantor dies, it gets a stepped-up basis to its fair market value at death.

- This eliminates the capital gains tax on the appreciation of the property that occurred before the grantor’s death.

- In addition, estate taxes are at a lower level because the valuation for estate tax purposes was frozen before appreciation in the trust.

This is all very well, but let’s see how this works out in practice.

Simplified Example

- Grantor: John

- Trust Beneficiary: Emily

- Property: Real estate

- Initial Value: $2 million

- Appreciated Value: $6 million

Steps:

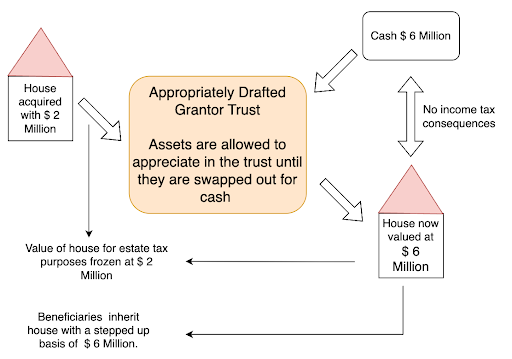

See Figure 1.

- Initial Transfer:

- John transfers real estate valued at $2 million to a trust with a swap power. This value is fixed for gift and estate tax purposes.

- Appreciation:

- The property appreciates to $6 million over several years, but its value for estate tax purposes remains "frozen" at $2 million.

- Using the Swap Power:

- John uses the swap power to exchange the $6 million property in the trust for $6 million in cash or other assets.

- This transaction has no income tax consequences because it is disregarded under Section 675.

- Basis Adjustment:

- Normally, the property in the trust would retain John's original basis, making any appreciation subject to income tax when sold.

- By swapping the property out of the trust for $6 Million, John reclaims the house. Upon his death and transfer to beneficiaries, the property gets a stepped-up basis to its fair market value of $6 million.

- This eliminates capital gains tax on the appreciation that occurred before John's death.

Figure 1: How to avoid capital gains and estate taxes with a swap power in a grantor trust (Intentionally Defective Grantor Trust)

John effectively avoids income tax on the property's appreciation during his lifetime and ensures the property gets a stepped-up basis at his death, providing significant tax advantages for Emily. Our tax planning conundrum from above has been solved.

A number of other techniques have a similar effect, but their discussion goes beyond the scope of this article.

Biden’s Reform Plans

Historical Background

Until 1986, taxpayers aimed to avoid having their trusts classified as grantor trusts to escape the burden of personally paying income taxes on trust earnings. This was crucial in an era with a highly progressive income tax system, exemplified by 1954’s 24 tax brackets ranging from 20% to 91%. In 1954 Congress, codifying judicial decisions and wanting to prevent income shifting from higher to lower tax brackets, enacted the grantor trust rules. However, the 1986 Tax Reform Act and subsequent reforms compressed income tax rates, making grantor trusts more favorable. Today, classifying a trust as a grantor trust often results in better tax outcomes. Moreover, as explained above, careful drafting of grantor trusts can limit both estate and income taxes to an extent otherwise not possible (1).

The current situation subverts Congress's original intent and is also perceived as societally unfair, as it benefits only the already very wealthy. Reforms are periodically suggested, most recently by the Biden administration in the Greenbook, the Tax Proposal for 2025 (2).

Several reform efforts are aimed at Grantor Retained Annuity Trusts, which we will discuss in a follow-up article but list here for context.

1. Grantor Retained Annuity Trusts (GRATs)

- Minimum Value for Gift Tax: The remainder interest in a GRAT must have a minimum value for gift tax purposes equal to the greater of 25% of the value of the assets transferred or $500,000.

- Annuity Payments: The annuity payments cannot decrease during the term of the GRAT.

- Minimum and Maximum Terms: The GRAT must have a minimum term of ten years and a maximum term equal to the annuitant's life expectancy plus ten years.

- Prohibition on Tax-Free Exchanges: The grantor cannot exchange assets held in the trust without recognizing gain or loss for income tax purposes.

- Impact: These changes aim to reduce the use of short-term and “zeroed-out” GRATs, which are often used for tax avoidance purposes.

2. Sales and Transfers Between Grantor Trusts and Deemed Owners

- Taxable Events: Sales of appreciated assets between a grantor and a grantor trust will be recognized as taxable events, requiring the seller to pay capital gains tax on the appreciation.

- Basis Adjustment: The buyer’s basis in the transferred asset will be the amount paid to the seller.

- Purpose: This proposal aims to prevent tax-free transfers of appreciated assets and ensure that such transactions are treated similarly to sales between unrelated parties.

3. Income Tax Payments as Gifts

- Gift Treatment: The grantor's payment of income tax on the trust’s income will be treated as a taxable gift to the trust. This gift will occur on December 31 of the year the tax is paid unless the trust reimburses the grantor.

- Impact: This change ensures that the grantor’s payment of the trust’s income tax liabilities is recognized as a transfer of value subject to gift tax.

4. Realization of Capital Gains

- Realization Events: Unrealized capital gains on appreciated property will be taxed at the time of transfer by gift or upon death. This includes transfers to or from most types of trusts and distributions from revocable grantor trusts to persons other than the trust’s owner or their spouse.

- Impact: This would treat transfers of appreciated assets as taxable events, departing from the current practice of realizing such gains only upon sale. It aims to ensure that high-income taxpayers do not benefit from deferred capital gains taxes indefinitely.

5. Intrafamily Asset Transfers

- Valuation Discounts: Discounts for lack of marketability and control will be reduced or eliminated for intrafamily transfers of partial interests in assets if the family collectively owns at least 25% of the property.

- Collective Valuation: The transferred interest’s value will be calculated as a pro-rata share of the total fair market value of the property held by the transferor and their family members, as if a single individual owned all interests.

- Purpose: This proposal aims to curb the use of valuation discounts to reduce the taxable value of intrafamily transfers.

What if the Republicans Gain Control of Congress?

The Republican proposals regarding grantor trusts largely focus on maintaining the status quo established by the 2017 Tax Cuts and Jobs Act (TCJA). This includes making the increased estate, gift, and generation-skipping transfer (GST) tax exemptions permanent, thus avoiding the reduction scheduled for 2026. Additionally, Republicans are likely to oppose the Biden administration’s suggested reforms, such as treating sales between a grantor and a grantor trust as taxable events and recognizing the payment of income tax on trust income as a taxable gift.

Conclusion

As we anticipate potential changes to the grantor trust rules in 2025, it’s clear that the landscape of estate planning may undergo significant transformations. The Biden administration’s proposals, likely to be adopted in a similar form by Vice President Harris, aim to close loopholes that currently allow for substantial tax advantages through mechanisms like the swap power and GRATs. These reforms would impose stricter requirements and tax consequences, curbing the ability to avoid capital gains and transfer taxes. Conversely, Republican proposals focus on maintaining the current tax benefits established by the 2017 Tax Cuts and Jobs Act. Understanding these proposals and their potential impacts is crucial for tax professionals and affluent taxpayers. Staying informed and proactive will ensure the optimal structuring of trusts and asset transfers, aligning with the evolving tax regulations and maximizing the benefits within the legal framework.

References:

1 Jesse Huber. The grantor trust rules: An exploited mismatch. The Tax Adviser. November 1, 2021

2 Department of the Treasury March 11, 2024. General Explanations of the Administration’s Fiscal Year 2025 Revenue Proposals. Green Book p.127

A podcast that summarized the points of this article is available here: