/>i

/>iIf you made your fundraising forecast in November, it could be due for an update. The Wall Street Journal's December 29 write-up Private Equity Faces Gloomy Fundraising Forecast for 2024 makes my point: The main statistic, Preqin Q1-Q3 global PE fundraising down 46% lower from a year earlier at 620 closings for $509 billion, drives the article’s discussion on the outlook for a prolonged downturn.

The narrative here is old terrain for FFF readers. Capital circulation in private markets slowed dramatically in the first half of 2023 as the fastest Fed hiking cycle on record translated to higher acquisition costs, reduced access to cheap financing, poor exit conditions, and a slump in distributions, all taking a toll on fundraising and portending fundamental changes in the industry.

More current data, however, also from Preqin, show full-year 2023 PE fundraising of 851 funds for $669.2 billion, finishing ahead of the $666.9 billion raised in 2022. That’s a pretty significant delta from the Q1-Q3 read to the full-year data.

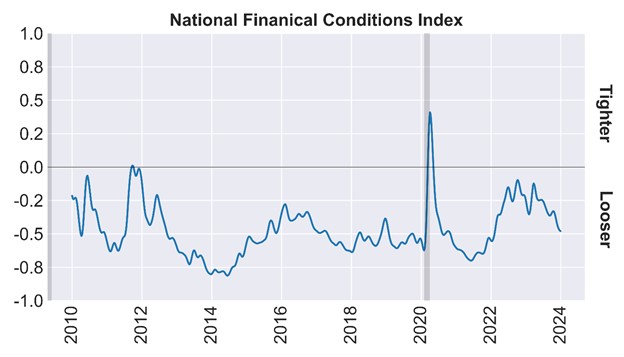

The recent easing in financial conditions probably go a long way to explain the gap. The Chicago Fed’s National Financial Conditions Index (NFCI) is back to the least restrictive levels seen since February 2022, and trending looser. (The NFCI bakes together 105 financial condition indicators such as credit spreads, interest rate volatility, and leverage levels into a composite index). Credit spreads and equity prices tell the same story.

Source: Federal Reserve Bank of Chicago and Cadwalader, Wickersham & Taft LLP.

Financial conditions have to be factored into the outlook for M&A volume, deal exits, and distributions. Global M&A declined by about 20% YoY in 2023 based on Refinitiv data, but key variables have changed in recent weeks. Most obviously, the forward interest-rate trajectory is now perceived to be less restrictive and less uncertain (84% market implied probability of a 50-75 bps funds rate cut by June). Public equities are expected to post a second consecutive quarter of YoY EPS growth in Q4. And the disconnect between strategic buyer and seller expectations is being filled, in part, through higher overall valuations. Distributions may well accelerate if financing costs continue lower and valuations remain high.

If distributions, do in fact, accelerate from here, the question then becomes: What do LPs do with that cash? On this point, LP survey data could shed some light. Two recent reports suggested sustained interest in maintaining or increasing private fund allocations:

- 64% of institutional investors are bullish on private equity, and 60% on private credit, according to results from the 2024 Natixis Institutional Investor Survey among 500 investors. A significant majority of investors indicate plans to increase or maintain private fund allocations.

- 82% of LPs plan to invest the same amount or more in PE funds over the next 12 months, according to the most recent PEI investor survey This total is up modestly after weakening somewhat in 2023. The number of investors reporting an overallocation to PE dropped to the lowest since 2021.

How do the pieces all fit together? Well, first, as David Rosenberg is fond of saying, “Fall in love with your partner, not your forecast.” When the variables driving the fundraising outlook change, so should the outlook.

Second, upside risk to the base case from a shift back to accommodative monetary policy and financial conditions can’t be ignored and should be expected to rejuvenate capital circulation in the private markets while these conditions hold.

Third, even if fundraising improves further, industry changes are inevitable, but are more attributable to the concentration of funds raised rather than absolute fundraising levels. Preqin reports 851 PE funds closed in 2023, down from 1,464 in 2022. Expect sponsors to continue to evaluate non-core strategy exits, consolidation, permanent capital vehicles, and greater retail participation.

Finally, downside risks are not insignificant. These are mostly macro and geopolitical. So, we’re left with taking a page from the Fed’s book: The 2024 fundraising outlook is going to be data dependent.

Chris van Heerden, Director | Fund Finance, authored this article.