/>i

/>i-

INTRODUCTION

Recent trends in merger enforcement demonstrate the importance of understanding the economic issues involved in platform mergers. The number of significant platform transactions reviewed by agencies has increased. For example, in 2014, both the US Federal Trade Commission (FTC) and the European Commission (EC) investigated Facebook’s acquisition of WhatsApp and cleared the merger.1 In 2018, the US Department of Justice (DoJ) unsuccessfully sued to block AT&T’s acquisition of Time Warner.2 More recently, in 2020, after a phase II investigation, the EC conditionally cleared Google’s acquisition of Fitbit.3

In this paper, using three recent platform mergers as examples, we discuss several economic issues that often arise in platform cases. The first case is CoStar/RentPath, which was challenged by the FTC and subsequently abandoned by the merging parties.4 We use this case to discuss market definition; specifically, how non-platform competitors should be treated and how indirect network effects can affect the analysis. The second, Sabre/Farelogix, was investigated in the UK and the US and was ultimately abandoned. In the UK, the merger was blocked by the UK’s Competition and Markets Authority (CMA). In the US, the DoJ challenged the merger, but was unsuccessful in district court.5 We use this case to discuss how to frame the theory of harm in the context of different approaches to horizontal and vertical mergers. Our third case, which we use to discuss recent academic research concerning the types of efficiencies that can arise in platform markets, is Ritchie Bros Auctioneers (RBA)/IronPlanet (IP), where the parties received a second request from the DoJ, but the transaction was not ultimately challenged.6

-

MARKET DEFINITION

Platforms typically bring together different group of users. For example, PlayStation and Xbox attract both video game players and game developers; Uber brings together consumers searching for rides and drivers; Mastercard and Visa bring together consumers using payment systems, such as debit or credit cards, and merchants.7 Platforms differ, however, in the business models that they use and the range of services they provide. For example, Google offers a wide range of services and relies primarily on advertising revenues, while payment card platforms offer a narrow set of functionalities and charge fees to both types of users.8 Platforms are typically characterised by network externalities, also often called network effects. These can be either direct (e.g., all else equal, users’ value of a social media platform will increase with the number of users on the platform) or indirect, where users care about scale on the other side of the platform (e.g., all else equal, rideshare users will value platforms more when they have more drivers).9 In some settings, both direct and indirect network externalities may exist.

When two platforms propose to merge, it is often necessary to consider whether the platforms would be constrained by competition from non-platforms that, while having different business models, may offer similar services to at least one side of the market. Recently, the US Supreme Court’s Amex decision has raised questions about when, as a matter of US law, it is appropriate to consider a non-platform business as part of the same market as platforms.10 However, from an economics perspective, it often makes sense to allow for this possibility and directly address this issue within market definition. The definition of the market was one of the key issues raised by CoStar’s proposed acquisition of RentPath in February 2020 for $587.5 million. In November 2020, the FTC challenged the merger, alleging that the merging parties had been each other’s closest rivals for years.11

CoStar and RentPath are real estate data and analytics providers that offer internet listing services (ILSs) — online sites where large apartment buildings post ads and detailed information (e.g., floor plans, videos, unit availability) and potential renters gather information on buildings that they are interested in.12 Currently, ILSs primarily generate revenues by selling subscriptions to apartment buildings that want their information displayed, with leases typically being agreed to between renters and buildings outside the ILS.13

An important choice during the merger review would have been whether to define a market that, in addition to the CoStar and RentPath ILSs, would have included only other ILSs (i.e., an ILS-only market), or a market that would have included other types of advertising that apartment buildings can and do use, such as their own websites, paid search on Google, and more traditional means like newspaper advertisements and flyers. As CoStar and RentPath operate the largest US ILS platforms, the merger would likely be presumptively anti-competitive based on standard measures of concentration, such as the HHI, in an ILS-only market. On the other hand, concentration measures might have been significantly lower if alternative types of advertising were included.14 In a broader market containing these alternative forms of advertising, the market shares of CoStar and RentPath would be significantly lower.

The conceptual market definition question can be framed as usual: would a hypothetical monopolist of a particular set of services find a small, significant, non-transitionary increase in price (e.g., 5 per cent) profitable?15 This framing allows for the possibility that both two-sided platforms and one-sided businesses can be in the same market. Naturally, the extent of the data available determines whether this question can be answered quantitatively, or only using qualitative evidence.

The fact that many apartment buildings currently use multiple types of advertising does not necessarily imply that they would shift substantial advertising volume away from ILSs in response to an increase in ILS subscription prices. For example, if ILSs allow buildings to reach particular types of renters (e.g., ones who are moving from out-of-town and so may not see local newspapers) or allow for more accurate targeting of advertising, then substitution away from ILSs would be limited and an ILS monopolist might find a price increase to be profitable.16

One factor that should be considered when defining markets that include platforms is how indirect network externalities may impact the profitability of a hypothetical price increase. It is possible that, when indirect network externalities are important, a price increase on one side of the market would trigger a feedback loop that reduces demand. Consider a price increase that would only cause a small decrease in demand from one side of the market holding demand from the other side fixed. This price increase may cause a significantly larger reduction in demand if a loss of users on one side leads to a reduction in usage on the other side, which, in turn, reduces usage on the first side even further. If the fall in demand after the feedback loop has played itself out is large enough, then the price increase will not be profitable.17

-

THEORIES OF HARM

In mergers where a platform and non-platform business propose to merge, it may be useful to focus less on market definition, especially in the way that this is often done in the context of horizontal mergers, and instead, focus on the theory of harm. Doing so can help to clarify the economic issues at hand. We illustrate this point in the setting of Sabre’s proposed acquisition of Farelogix.

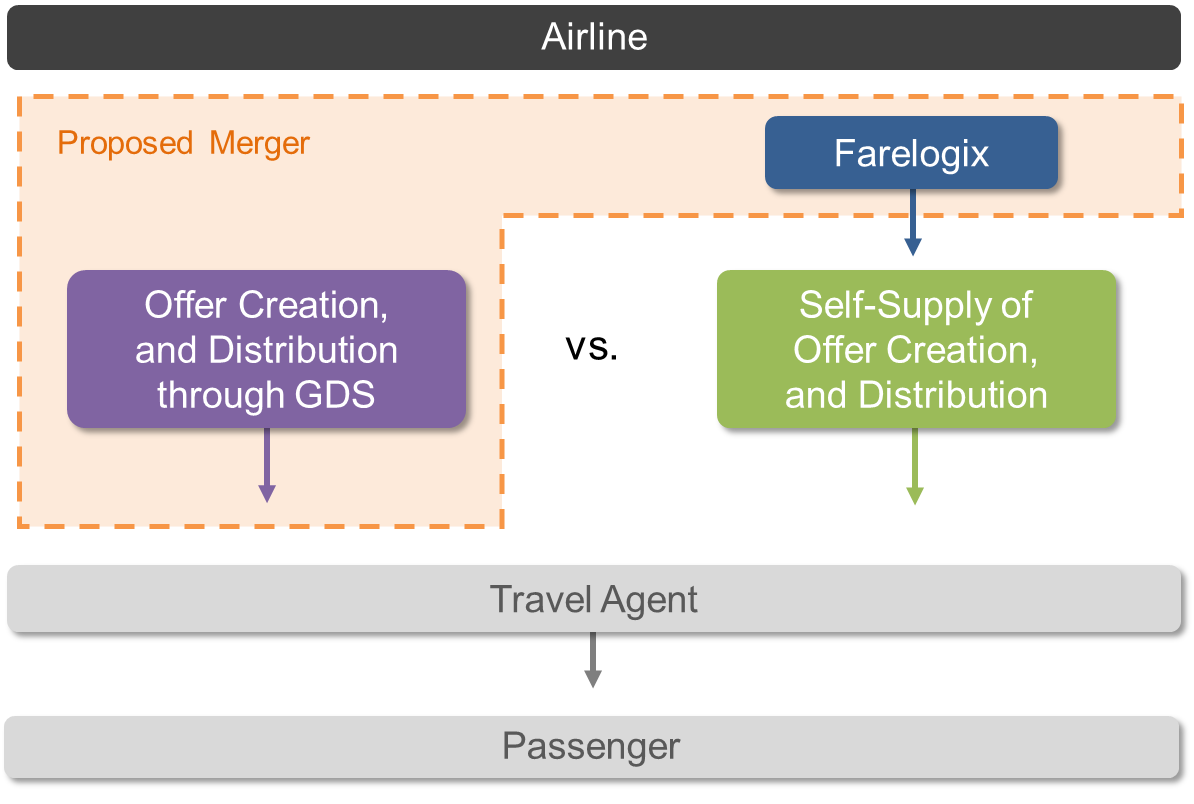

Sabre and Farelogix are technology and software providers to the airline and other travel industries. In November 2018, Sabre proposed to acquire Farelogix. As noted above, the merger was blocked by the CMA and was ultimately abandoned. Sabre serves as a Global Distribution System (GDS) — a platform that aggregates the content (e.g., fares, seat availability, and schedules) from various airlines and other travel providers. GDS providers, which also include Amadeus and Travelport, sell services to both airlines and travel agents, who use GDS services to create travel packages for their clients. However, rather than using a GDS platform, airlines may connect and provide offers to travel agents directly through different types of software, including the types of software sold by Farelogix.18

One approach to thinking about the transaction, which is consistent with the approaches used by both the CMA and the DoJ, is to view it as a horizontal merger between firms competing in the same product market.19 While this framing is consistent with how Sabre appeared to recognise the growth of Farelogix as a competitive constraint,20 it appears inconsistent with the extent to which the parties’ activities actually overlap — for example, GDS providers actively operate as two-sided platforms contracting with both airlines and travel agents to facilitate transactions, whereas providers like Farelogix provide customised software to airlines and do not directly deal with travel agents.

An alternative framing, which avoids this problem, is to consider the proposed transaction as a vertical merger, where Farelogix is an input provider for self-supply of GDS services (i.e., offer creation and distribution) by airlines. It is the self-supply channel which competitively constrains the GDS platforms, and so should be included in the same market as GDS. This is illustrated in the following figure.

Figure 1 – Global Distribution System, Farelogix, and Self-Supply

It is common to think of a vertical merger as being a merger of two firms that are in the same supply chain (i.e., one party supplies the other party with some type of good or service). When a merger takes place within a supply chain, it will often have both pro-competitive and anti-competitive effects: pro-competitive effects arising from the possible elimination of double marginalisation or other types of supply chain coordination, which may ultimately benefit consumers; and anti-competitive effects arising if the merged entity offers less favourable terms post-merger to downstream rivals that the upstream party supplies in order to create an advantage to the downstream merging partner. This theory of anticompetitive effects is often called “raising rivals' costs”.21

However, the set of possible vertical mergers also includes what have sometimes been labelled “diagonal mergers” where, for example, a downstream firm acquires an upstream supplier from which it does not source any inputs, but which does supply one or more of its downstream rivals.22 In this case, the “raising rivals costs” incentive may still exist, but there may not be countervailing pro-competitive benefits associated with supply chain coordination. Therefore, even though classifying a merger as vertical may mean that agencies are unable to appeal to legal presumptions that exist for horizontal mergers, as a matter of economics, some types of vertical transactions, such as diagonals, can be viewed as having the potential to be anti-competitive.

In Sabre/Farelogix, even though the district court disagreed with the DoJ’s characterisation of Sabre and Farelogix as competitors in the same market, it was “persuaded” that Farelogix provided a “real alternative to the GDS,” and Sabre considered the “acquisition of Farelogix as [a] way to neutralize this perceived threat.” Furthermore, according to the court, the merger may have reduced “one source of airlines’ leverage in negotiating with GDSs,” and would have incentivised Sabre to increase the prices or reduce the availability of Farelogix products.23 These descriptions of possible anti-competitive effects are consistent with a vertical/diagonal framing.24 A vertical framing would also have provided a natural framework for assessing Sabre’s claims that the transaction could generate pro-competitive benefits, if, contrary to the supply relationships existing before the merger, Farelogix’s software would be used to provide improved versions of Sabre’s own products.25

-

EFFICIENCIES

In assessing any horizontal or vertical merger, agencies have to consider potential pro-competitive effects that could incentivise the parties to provide lower prices or better products.26 If evidence suggests that both anti- and pro-competitive effects may be present, it will be important to quantify their magnitude and assess the net impact of the merger.

In the case of a horizontal platform merger, network externalities (typically not an issue in non-platform mergers), can lead to significant efficiencies that are of first-order importance. This is because users on both sides of a platform may benefit when usage on one side increases.

For example, consider two differentiated platforms where sellers of a particular type of product try to connect with buyers, and, because of the way the platforms in question work, only buyers can multihome (i.e., sellers are restricted to list on at most one platform). Buyers who search both platforms (i.e., multihomers) will get a more complete view of the selection of goods available, and so tend to be better matched. But, individual buyers may find it costly to multihome, and independent platforms may not choose to facilitate multihoming if it increases substitution and price competition between the platforms (e.g., on commissions).

Now suppose that the companies operating the two platforms merge. One possibility is that the merged firm creates a single, thicker platform where all buyers can browse the full selection of products. However, another possibility is that the merged firm continues to operate both platforms but, as a result of the merger, has more incentive to facilitate multihoming. As a matter of economic theory, it is quite possible that these effects will leave both buyers and sellers better off, even if prices increase somewhat.

Recently, Yao (2021) studied these issues in an in-depth retrospective evaluation of the 2017 merger of two North American auction platforms (RBA and IP) that facilitate buying and selling of used heavy equipment. Yao (2021) finds that a small increase in commissions was outweighed by procompetitive effects.27 RBA was the largest primarily offline (or onsite) auction platform, while IP was a primarily online platform that had emerged as a significant challenger in the used heavy-truck auction market. Online auctions occur more frequently than offline auctions, which require large amounts of equipment to be moved to a single place. However, since many buyers prefer to inspect equipment in person, RBA still accounted for a significantly larger share of transactions at the time of the merger.28 As noted above, the parties received a second request from the DoJ but the transaction was not ultimately challenged.

Yao (2021) shows that after the merger was consummated, some transaction commissions increased. Therefore, looking only at direct price effects, one might conclude that the deal was anti-competitive. However, the merged entity also made improvements on the platform — including integrating customer service and making it much easier for interested buyers to get information on equipment being sold in both online and offline auctions. Yao (2021) estimated a model of search and matching, and competition within auctions for particular pieces of equipment, and showed that the benefits of better matching after the merger were substantial. Better matching was a direct benefit for buyers, but because better-matched buyers were also willing to pay/bid more, the majority of sellers benefited as well, and the overall benefit to buyers and sellers dominated the negative effects of commission increases.29

-

CONCLUSION

With the number of significant platform transactions reviewed by agencies on the rise, economists and economic analysis are taking a greater role in the assessment of these mergers. Economic analysis can offer valuable insights in defining markets — particularly in assessing the extent to which platforms might be constrained by competition from non-platforms or the magnitude of network effects and how they impact the profitability of price increases; in framing the theory of harm in the context of different approaches to horizontal and vertical mergers; and in demonstrating the efficiencies associated with network effects, which can be of first-order importance.

The views expressed herein are those of the authors and do not necessarily reflect the views of Cornerstone Research or its clients. This article was first published by Competition Law Insights.

Endnotes

1 FTC, Press release, “FTC Notifies Facebook, WhatsApp of Privacy Obligations in Light of Proposed Acquisition”, 14 April 2014; European Commission, Case No COMP/M.7217 - FACEBOOK/ WHATSAPP, Regulation (EC) No 139/2004 Merger Procedure, 3 October 2014, p. 35.

2 Redacted Proposed Conclusions of Law of the United States, United States of America v. AT&T INC., DIRECTV GROUP HOLDINGS, LLC, and TIME WARNER INC., 8 May 2018, ¶ 1; Financial Times, “US Court Backs AT&T’s Acquisition of Time Warner”, 26 February 2019.

3 European Commission, Press release, “Mergers: Commission Clears Acquisition of Fitbit by Google, Subject to Conditions”, 17 December 2020. Google closed the transaction despite the investigation being ongoing in certain jurisdictions, including the US. See Burnside, A, De Backer, M and Strohl, D, “Google/Fitbit: Merger Control Unfit for Purpose”, Competition Law Insight, Vol. 20, No. 2, p. 1.

4 FTC, Press release, “Statement of Daniel Francis, Deputy Director of the FTC’s Bureau of Competition, Regarding the Announcement That the Parties Have Abandoned CoStar Group Inc.’s Acquisition of RentPath Holdings, Inc.”, 31 December 2020.

5 CMA, “CMA Blocks Airline Booking Merger”, 9 April 2020; Opinion, US v. Sabre Corp., et al., 1:19-cv-01548-LPS, United States District Court for the District of Delaware, 8 April 2020 (“Sabre/Farelogix Opinion”).

6 PR Newswire, “Ritchie Bros. and IronPlanet Receive Requests for Additional Information and Documentary Material under HSR Act”, 15 December 2016, ; PR Newswire, “Ritchie Bros. Completes Its Acquisition of IronPlanet, Growing Digital Presence and Offering Unprecedented Choice to Customers”, 31 May 2017, .

7 Weyl, G E and White, A, “Let the Right ‘One’ Win: Policy Lessons from the New Economics of Platforms”, Competition Policy International, Vol. 10, No. 2 (2014), pp. 29–51, at p. 29.

8 Visa, “Interchange Fees”; Mastercard, “Understanding Interchange”; European Commission, Case No AT. 39740 – Google Search (Shopping), 27 June 2017, ¶¶ 7–37.

9 de Reuver, M, Sorensen, C and Basole, R, “The Digital Platform: A Research Agenda”, Journal of Information Technology, Vol. 33, No. 2 (2018), pp. 124–135, Table 1.

10 Ohio et al. v. American Express et al., 138 S. Ct. 2274 (2018), p. 19.

11 FTC, Press release, “FTC Sues to Block CoStar Group, Inc.’s Proposed Acquisition of Chief Competitor RentPath Holdings, Inc.”, 30 November 2020; Redacted Administrative Complaint, In CoStar Group Inc. and RentPath Holdings Inc. Docket No. 9398, (“CoStar/RentPath Complaint”), ¶ 18.

12 FTC, Press release, “FTC Sues to Block CoStar Group, Inc.’s Proposed Acquisition of Chief Competitor RentPath Holdings, Inc.” 30 November 2020; CoStar/RentPath Complaint, ¶¶ 20–30.

13 CoStar Group, Inc., SEC Form 10-K for the fiscal year ended 31 December 2020, filed on 19 February 2021, pp. 6–7.

14 CoStar/RentPath Complaint, ¶¶ 20–30.

15 DoJ and FTC, “Horizontal Merger Guidelines”, 19 August 2010, (“Horizontal Merger Guidelines”), Section 4.1.1. Alternatively, the merging firm may find it profitable to worsen non-price aspects. For example, in Sainsbury/Asda, in addition to price effects, the CMA assessed whether the merged entity would reduce quality, or choice, such as product ranges or services offered to consumers. See CMA, “Final Report: Anticipated Merger between J Sainsbury PLC and Asda Group Ltd”, 25 April 2019, ¶¶ 10, 21.

16 CoStar/RentPath Complaint, ¶¶ 20–30.

17 Evans, D and Schmalensee, R, “The Industrial Organization of Markets with Two-Sided Platforms”, Competition Policy International, Vol. 3, No. 1 (2007), pp. 151–179, at pp. 173–174.

18 CMA, “Final Report: Anticipated Acquisition by Sabre Corporation of Farelogix Inc.”, 9 April 2020, (“Sabre Farelogix Final Report”), pp. 8–9, 15, 50, Section 3. As discussed above, in the US, the DoJ challenged the merger but was unsuccessful in the district court. The court’s opinion is highly disputed for many reasons, including how the court interpreted the Amex decision, and subsequently concluded that “as a matter of law” Sabre and Farelogix cannot be competitors because Farelogix is not a platform. As discussed in Section 2, from an economic perspective non-platform channels can exert competitive pressure on platforms, and the determination of the degree of this pressure should be assessed empirically. See Sabre/Farelogix Opinion, pp. 69–72; Hatzitaskos, K, Howells, B and Nevo, A, “A Tale of Two Sides: Sabre/Farelogix in the United States and the UK”, Journal of European Competition Law and Practice (2021), p. 6.

19 Sabre Farelogix Final Report, ¶¶ 11.95–11.102; Complaint and Demand for Jury Trial, USA v. Sabre Corporation et al., Case 1:99-mc-09999, United States District Court For the District of Delaware, 20 August 2019 (“Sabre Farelogix Complaint”), Section VI.

20 Sabre/Farelogix Opinion, p. 87.

21 DoJ and FTC, “Vertical Merger Guidelines”, 30 June 2020, (“Vertical Merger Guidelines”), Sections 4.a, 6.

22 Higgins, R, “Diagonal Merger”, Review of Industrial Organization, Vol. 12, No. 4 (1997), pp. 609–623, at pp. 610–611. Also, Moresi and Salop recently argued that under certain conditions vertical mergers may lead to the loss of “an indirect competitor.” Moresi, S and Salop, C, “When Vertical Is Horizontal: How Vertical Mergers Lead to Increases in ‘Effective Concentration’”, Review of Industrial Organization, Vol. 59, No. 2 (2020), pp. 177–204, at pp. 177–178.

23 Sabre/Farelogix Opinion, pp. 62, 87–90.

24 Similarly, Moresi and Salop also note that the DoJ “could have framed the proposed acquisition as a vertical merger, but explained to the court that the merger had indirect horizontal effects because Farelogix supported competition between Sabre and the airlines in the market for booking services to travel agencies.” Moresi, S and Salop, C, “When Vertical Is Horizontal: How Vertical Mergers Lead to Increases in ‘Effective Concentration’”, Review of Industrial Organization, Vol. 59, No. 2 (2020), pp. 177–204, at p. 178.

25 Sabre, Press release, “Sabre Enters Agreement to Acquire Farelogix, Expanding Its Airline Technology Portfolio and Accelerating Its Strategy to Deliver Next-Generation Retailing, Distribution and Fulfillment Capabilities”, 14 November 2018; Sabre/Farelogix Opinion, p. 57; Vertical Merger Guidelines, Section 6.

26 For example, the Horizontal Merger Guidelines emphasise that efficiencies involved in a horizontal merger, among others, include cost reductions and subsequent effects on price — either in the form of unilateral effects, i.e., cost reductions reduce the merged entity’s incentive to increase the price or multilateral effects, i.e., cost reductions reduce the likelihood of coordination. On the other hand, the Vertical Merger Guidelines recognise the complementary nature of the products produced by the vertically related parties and emphasise that the merged entity may streamline production, improve distribution and inventory management, and reduce double marginalisation (price may be lower if the merged entity maximises profits as a single entity, in comparison to the counterfactual, where the merging parties maximise the profits as two distinct entities). See Horizontal Merger Guidelines, Sections 6, 7; Vertical Merger Guidelines, Section 6.

27 Yao, X, “Platform Mergers in Search Markets: An Application in the U.S. Used Heavy Truck Market”, Job Market Paper, University of Maryland (2021), (“Yao (2021)”). Academic economists are beginning to explore the pro- and anti-competitive effects of platform mergers using a combination of data on what has happened after consummated mergers, as well as models that capture the incentives of platforms and platform customers. In addition to Yao (2021), see also Farronato, C, Fong, J and Fradkin, A, “Dog Eat Dog: Measuring Network Effects Using a Digital Platform Merger”, NBER Working Paper No. 28047, November 2020; Jeziorski, P, “Effects of Mergers in Two-Sided Markets: The US Radio Industry”, American Economic Journal: Microeconomics, Vol. 6, No. 4 (2014), pp. 35–73; Ivaldi, M and Zhang, J, “Platform Mergers: Lessons from a Case in the Digital TV Market”, Centre for Economic Policy Research Discussion Paper, No. DP14895, March 2021.

28 Yao (2021), pp. 2–13.

29 Yao (2021), pp. 2–5, 54–55.