/>i

/>iA comprehensive guide to reviewing Commercial & Industrial or Distributed Generation Solar project documents for Partnership/Flip and Sale/Leaseback Transactions

1. Forward

In an industry that boasts over 60 different forms of PPA, some much better than others, knowing how to make your project documents financeable is of paramount importance. We know that all companies face challenges with internal legal and compliance training and decided that sharing a Manual that can be used as an ongoing reference tool would be far more useful to our clients than a one-hour seminar. We are therefore sharing this Manual with you to help your legal and business teams ensure that you do not have to make costly and frustrating amendments when it comes time to finance your projects.

This Manual highlights what financing parties look for when they undertake due diligence, explains what provisions to include in project documentation and why such provisions are important. It contains guidelines to keep in mind while reviewing or negotiating a set of C&I solar project documents, followed in each section by a “checklist” of items to confirm you have evaluated the key aspects of the applicable document. We have included a sample “Due Diligence Summary” that we provide to financing party clients for each C&I solar project – it’s a handy reference tool that contains the most basic document terms and a section on highlighted issues (Financing Party Notes). If developers provided something like this to financing parties upfront, together with a well-organized dataroom, then diligence costs would most definitely go down.

Most of us who work in the solar market landed here not just because we enjoy projects, but also because we believe that solar is the future. The better the project documents, the smoother the financing, and the more projects get done – and then suddenly, the future is brighter.

A. Tax Equity Due Diligence Summary

Summary as of DATE: __________ Prepared by: ____________

Project Company:

System Location (Address):

System Size (kW/MW): _____AC; _____DC

Structure: [_] Ground Mount [_] Roof Mount [_] Parking Canopy [_] Landfill

Financing: [_] Sale Leaseback [_] Partnership Flip

Regulatory Approvals: [_] QF Self-Cert (≥1 MWAC) [_] EWG (>30 MWAC) [_] MBR Authority (>20 MWAC) [_] None

1. Revenue Contract(s): [_] PPA [_] Net Metering Credit Purchase Agreement [_] Other

-

Host/Type (Private Company/Utility/Municipality):

-

Term/Renewal Terms:

-

Pricing:

-

Purchase Options:

-

Guaranteed Milestones:

-

Termination Value:

-

Termination Rights:

-

Force Majeure:

-

Credit Support Requirements:

-

Performance Guaranty:

-

Third Party Items Required: [_] Third Party Consent [_] Estoppel [_] Legal Opinion

2. Site Document: [_] License contained in PPA [_] Site License [_] Facility Use Agreement [_] Site Lease [_] Easement [_] Other

-

Site Provider (Fee Owner/ Site Lessee):

-

Term/Renewal Terms: (flag if term/renewal terms do not extend until at least 35 years)

-

Rent:

-

Guaranteed Milestones:

-

Credit Support Requirements:

-

Third Party Items Required: [_] Third Party Consent [_] Estoppel [_] Owner Consent/NDA

-

Additional Items Required: [_] Mortgage [_] Memorandum of Site Lease/License [_] Title Insurance

3. Interconnection Agreement:

-

Utility:

-

Maintained by: [_] Host [_] Project Company

-

Term/Renewal Terms:

-

Guaranteed Milestones:

-

Credit Support Requirements or Other Costs:

-

Net Metering Permitted: □Yes □No

-

Third Party Items Required: [_] Third Party Consent [_] Estoppel

4. EPC Contract

-

Contractor:

-

Contractor Credit Support:

-

Contract Price:

-

Warranties (note equipment brand):

-

Modules:

-

Inverters:

-

Trackers/Other:

-

-

Performance Guaranty:

-

Guaranteed Milestones:

-

Amount Due as of Anticipated Financing Date:

-

Liability Cap:

-

Third Party Items Required: [_] Third Party Consent [_] Estoppel

5. O&M Agreement

- O&M Provider:

-

O&M Provider Credit Support:

-

Service Fee:

-

Warranty:

-

Performance Guaranty:

-

Liability Cap:

-

Third Party Items Required: [_] Third Party Consent [_] Estoppel

6. REC or Incentive Agreement

-

Purchaser:

-

Term:

-

Quantity/Type:

-

Annual Requirement:

-

Price:

-

Third Party Items Required: [_] Third Party Consent [_] Estoppel

7. Financing Party Notes:

2. FINANCING STRUCTURES OVERVIEW

I. Financing Structures

Here is a very basic overview of tax equity financing structures to be shared with and used as a reference tool by your employees at all levels. The two main tax equity structures are sale/leasebacks and partnership/flips. These both allow a tax equity investor to take advantage of the tax benefits available to a solar transaction. Currently, this means tax depreciation of the asset, as well as the Investment Tax Credit (ITC) in the following amounts:

|

Starting Construction |

ITC Amount |

|

Through 2019 |

30% |

|

2020 |

26% |

|

2021 |

22% |

|

2022 (and beyond) |

10% |

The ITC is a one-time credit against income tax that is based on the amount invested in a facility. The ITC is subject to recapture if, within five years after a facility is “placed in service,” the taxpayer sells or otherwise disposes of the project or stops using it in a manner that qualifies for the credit – like taking it out of service or permitting the PPA offtaker to operate and maintain the project.

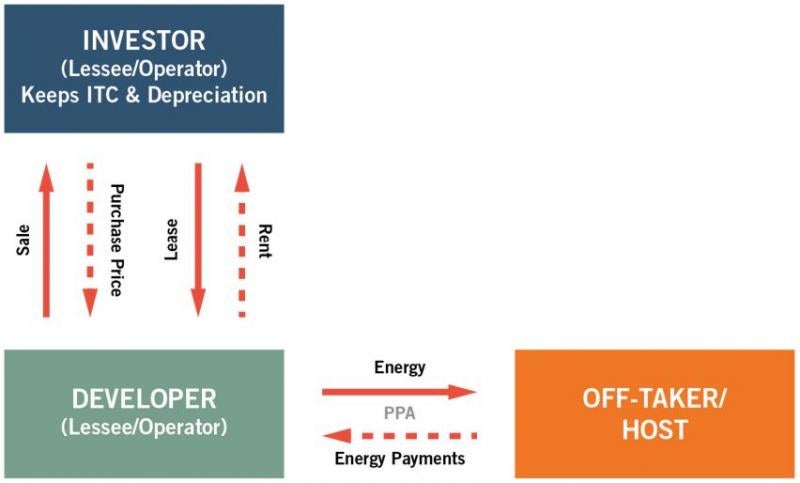

II. Sale/Leaseback

A sale/leaseback is a sale to a tax investor of solar equipment and an instant lease back to the developer of the same equipment so the developer can use it (typically to sell the generated power to a third party host). It is attractive to developers because it offers 100% upfront financing and a “step-up” in ITC basis upon the sale for fair market value, although the IRS rules require there to be a 20% residual value at the end of the lease term, making the end-of-term purchase price higher than that seen in a partnership/flip. Documentation usually involves a Purchase Agreement and Bill of Sale (for the sale part) and a Lease Agreement and Rental Schedule (for the lease part). Investors (Lessors) will generally take assignment of the deal collateral (mainly project documents) under a security agreement (or, for real property, a mortgage or deed of trust). Third party consents are generally required for each project document, even when the document is expressly assignable, as the consents provide the investor with estoppel language and additional rights and remedies.

Sale/leasebacks have three end-of-term options: a purchase option for fair market value, a renewal option (not to go beyond 80% of the equipment’s useful life), and a return option. The return option must be a viable option and the sale/leaseback documentation cannot be read to compel the Lessee to exercise the purchase option. It is therefore imperative that the PPA and Site Document counterpart(ies) agree that the investor (or Lessor) may take direct assignment of such project documents at the end of the sale/leaseback term in order to preserve the option for the developer (or Lessee) to return the solar equipment in place – this agreement is typically contained in the third party consents, but is even better placed in the project documents from day one.

The sale/leaseback closing typically takes place after Substantial Completion of the project (due to a 90- day window permitted by the IRS to enter into a sale/leaseback transaction after the placed in service date and still be eligible to take the ITC) and the EPC Contract will accordingly be mostly performed – consequently, review of an EPC Contract for these transactions focuses only on warranties, indemnities, performance guarantees, and any other provision that would survive full performance or give rise to a claim (such as a guaranteed substantial completion date and subsequent LDs). As the investor is the project owner and the developer is the project company owner, it is important to note who is the beneficiary of the warranties and whether they are assignable. Further, since there is a sale of equipment taking place, it’s important for the client to note whether a sales tax exemption is available in the relevant state under a “sale for resale” or other exemption for the initial sale, and what taxes are imposed on the ongoing rent payments. In sale/leaseback transactions, the developer usually takes risks relating to: timing of placement in service, ITC amount, and ITC timing, and the investor usually takes risks relating to structure/true lease risk, rent accrual patterns, and residual risk (change in law risk is negotiable).

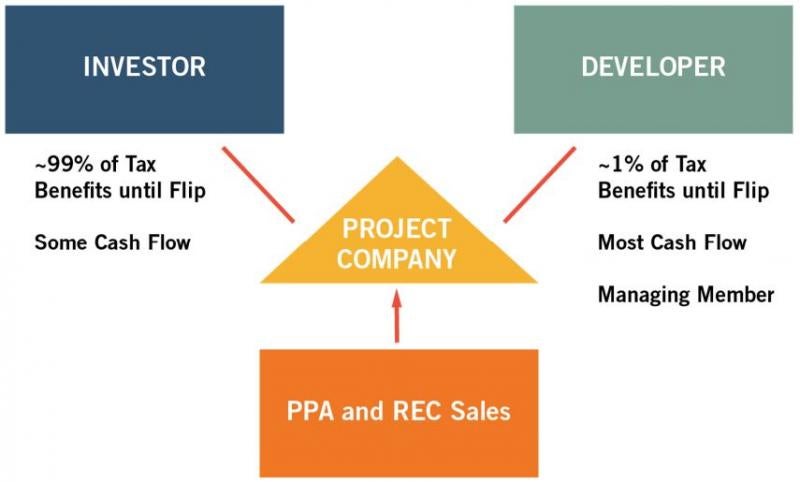

III. Partnership/Flip

A partnership/flip is a simple concept - a developer brings in a tax investor as a partner to own a solar project together. In a yield- based flip, the partnership allocates taxable income and loss ~99% to the investor until the investor reaches a target yield, after which its share of income and loss distributions flips to a lower percentage and the developer has an option to buy the investor’s interest. Cash is distributed in specified ratios before the flip based on expected energy production and timing of the flip date. In addition to the yield-based flip, there is also a fixed-flip structure that is used principally by US Bank and leaves as much cash as possible to the developer – in these, there is usually a cash flip at the 5th year and a tax flip at the 6-7th year, with a 2% preference to the investor and some sharing on additional distributions if production is good. Flip deals are different than sale/leasebacks in terms of the amount of capital raised, risk allocation and the timing of when the investor must invest. A sale/leaseback provides the developer with the full fair market value of the project (in theory). In a partnership/flip, the investor contribution is usually 40% to 85% of the fair market value and the developer must provide the rest.

In order for the investor to be eligible for the ITC, it must be a partner in the partnership prior to the assets being placed in service – for this reason, investors typically contribute 20% of their investment related to a project after mechanical completion of such project, but before it is placed in service. The remaining 80% is typically contributed after substantial completion for the project is achieved. For this reason, financing parties review an EPC Contract for a partnership/flip transaction with more emphasis on the requirements for mechanical completion, as well as the remaining obligations of the EPC contractor after mechanical completion is achieved. Unlike in a sale/leaseback, the investor is taking some construction risk – for the period between mechanical and substantial completion – and will care about contractor obligations and remedies from and after the mechanical completion date. Also unlike a sale/leaseback transaction, the investor is an owner in the project company and will not be taking a security interest in the project documents – therefore only an estoppel certificate will be required from the third parties (and no third party consents to assignment).

3. REVIEWING POWER PURCHASE AGREEMENTS (PPAs) AND NET METERING

CREDIT PURCHASE AGREEMENTS

A C&I PPA should be a simple contract whereby a host agrees to purchase power from a system owned by a project company – this should include project company obligations that naturally relate to providing such a service, like installing the system and a meter and maintaining insurance. A Net Metering Credit Purchase Agreement should look exactly like a PPA, except that instead of purchasing power, the host purchases net metering credits – and the system will not be co-located with the host (so no access rights, installation requirements, or any other provision relating to the site will be included).

The two main concerns when reviewing a PPA are whether the PPA is a true service contract and, if so, whether it is otherwise financeable. Any provisions that would cause the host to play an ownership role in the equipment or that would put pressure on the host to exercise a purchase option will be problematic – it is for this reason that we like to see “service contract” (Code Section 7701(e)) language showing the intent to be a service contract, and why permitting the host to operate or maintain the system or have more than a few purchase options or an end-of-term bargain purchase option would be a fatal flaw. Further, any right the host might have to get out of paying for electricity – whether through shutting down the system for any reason without paying for estimated lost power or through being permitted to terminate the contract for any reason other than project company default or force majeure – will be problematic from a financing perspective. Also, any obligation the project company might have outside of installing, operating and maintaining a solar system and typical related service obligations should be noted as a potential problem (roof repair obligations, for example). Any provisions that could impact economics, like site upgrades, credit support requirements, onerous site restoration obligations or any mechanics that could cause pricing to go down will be red flags that a Financing Party will need to evaluate.

I. Gating Items:

-

State Permitted.

-

Are PPAs permitted in the state where the system is located? Some states, like Florida and Texas, have legal roadblocks in place to prevent solar PPAs from being used there. Further, a net metering credit purchase agreement depends on a utility accepting net metering credits to offset a customer’s bill – this structure must be permitted in the state and/or by the specific utility.

-

Does the PPA require state PUC approval? This is typically noted somewhere on the cover page or in the boilerplate and will typically only apply to a utility host (not a corporate host).

-

-

Parties. Who are the parties to the PPA?

-

Is the host the same entity whose credit your Financing Party is reviewing? If not, what comfort do you have that the host shares the same creditworthiness?

-

Is the power provider the project company? If not, it should be assigned to the project company.

-

If the host is a municipal entity, it is likely that additional rules and laws apply – note what those are (if referenced in the PPA) and look them up (usually available online) – see if there are any that would override the PPA terms. Also, some tax equity providers require a legal opinion from every host that is a municipal entity, so ask your counterparty if delivery of a legal opinion will be an option and who the contact person will be for that request.

-

-

Project. Does the description, capacity, and location of the project match the other project documents and the financing documents? If not, this should be noted and will need to be fixed.

-

Milestones. Look at the milestone dates in the PPA. Have they been met? Is there a guaranteed date for commencement of construction or commercial operation? If so, what is the penalty for missing the guaranteed date? Aim to delete this milestone if possible – it is very rarely met.

-

Credit Support. What type of credit support will be required from the project company – your Financing Party may require you to reserve this amount in cash or provide a letter of credit outside of your financing, which may be costly.

II. Term:

-

Length. How long is the term? It is preferred that the term not extend beyond 80% of the expected life and value of the equipment. This is a particular concern where the host is the landowner. The risk is that, if the host is taking the benefit of the system for its entire useful life and essentially paying for the system in full over time, then the PPA could be characterized as a loan and the host seen as the true owner of the system.

-

Renewal. What are the renewal terms, if any?

-

Automatic renewal terms are counted as part of the base term unless either party has the right to terminate within a certain amount of time prior to the automatic renewal.

-

Renewal terms at fixed prices are counted as part of the base term for purposes of the 80% test, so the renewal term price should be re-set to market value.

-

Note that a typical PPA term is 20 years with an option for a 5 year renewal term – sometimes there are two renewal terms. As noted, renewal terms should be at the option of the host, but preventable by notice from the project company, and the pricing should be at the then-FMV. If a PPA term goes beyond 25 years without these mitigating factors, or if it goes beyond 30 years even with these mitigating factors, a Financing Party may require you to amend it.

-

III. Power Purchase and Payment.

-

Quantity. Host should agree to purchase no less than 100% of the power generated by the system that is received by the host. Any cap on the amount of power the host is to receive will be reviewed carefully by your Financing Party and could impact your economics. Host should not be required to pay for power it does not receive (meaning that project company cannot require host to pay a fixed amount regardless of whether or not it receives power), unless host is not receiving power due to its own actions or inactions (for example, due to a host default or host-requested outage).

-

Interconnection. Is net metering available? If not, the interconnection agreement should still provide that the power may flow onto the grid. Otherwise the system’s production will be curtailed if it is capable of producing more power than the host is able to use. If there is any indication that power cannot be put onto the grid, it is viewed as a potential fatal flaw. If the host is party to the Interconnection Agreement (and not the project company), then the host should be responsible for maintaining an interconnection and an interconnection agreement (this is always preferred and the Financing Party will want to know if it is not the host’s obligation to maintain).

-

Pricing. How is the pricing structured? Typically, there is an initial price per kWh with an annual escalator, or at least gradually increasing pricing over time. If the PPA calls for a prepayment, fixed periodic fee, uneven pricing or adjustments to pricing in certain events, then tax lawyers will be called in to review. Tax lawyers will also need to know if the host is required to pay property taxes.

-

Outages. How many outages is the host permitted per year? Typically, we see 24-48 hours of permitted outages without penalty, and anything above that will trigger project company’s right to reimbursement for downtime, estimated based on historical production. Financing Parties will bristle at permitted outages longer than a few days. If outages beyond 48 hours per year are not compensated by the host, then this is a potential fatal flaw.

-

Environmental Attributes. Unless negotiated otherwise, environmental attributes will only be included in the sale of power if the host is the only entity that can use them. The PPA should specifically state that such environmental attributes do not include any tax incentives or credits (and grants in lieu of these), which will always remain with the project company. Determine what the business deal is with respect to state and local or utility rebates/incentives and make sure the PPA reflects the business deal. If the definition of environmental attributes is so broad as to include tax benefits, then make sure the environmental attributes accrue to the project company. If the tax benefits can be read as accruing to the host, then this is a potential fatal flaw.

-

Metering. Project company should agree to install and maintain a utility grade kWh meter to measure the electricity output for billing purposes.

-

Host should grant the right to remotely monitor the meter and install any communication devices necessary for the monitoring. Host should be required to maintain a consistent internet connection at the site for this purpose.

-

Project company should be granted right to remotely monitor the meter and install any communication devices necessary for such monitoring.

-

Mechanics are typically included in the PPA to provide for meter auditing, and if the meter reading is inaccurate by more than a certain percentage, the parties will agree on the proper price adjustment. The main meter on the site stays in the name of the host, and host generally agrees to arrange with the utility to have project company named as an agent of host so that it may receive copies of invoices for monitoring purposes.

-

The meter is typically the PPA delivery point – the point where the transfer of title to the electricity produced by the system takes place (sometimes it’s a substation – but this is more common in larger utility deals). If the project company is party to the interconnection agreement, this should match the delivery point specified in the interconnection agreement – if the points do not match, this is a potential fatal flaw. If the host is party to the interconnection agreement, then there may be two meters – one to measure the project output to the host, and one to measure power going to and from the grid, and therefore the PPA delivery point and the IA deliver point may not match.

-

-

Reg-Out Clause. Is there a reg-out clause? This will permit project company (not the host) to modify the contract price or terminate the PPA if a change in law or regulation imposes a requirement on project company that materially affects its ability to perform. As long as the changes are within the control of the project company, then these provisions are fine – if they are within the control of the host (i.e., the host has the option to change pricing or terminate the PPA), then they could indicate a potential fatal flaw.

IV. System Transfer and Purchase Options.

There should not be a reasonable likelihood that the host will end up with the system at the end of the PPA term.

-

Number of Purchase Options. How many purchase options are offered to the host? More purchase options make it more likely that the host will own the system. Most investors get concerned when the number of host purchase options exceeds 1-3 throughout the term. Continuous purchase options are common, but hard to sell to investors and could require an amendment down the line since multiple purchase options put additional tax pressure on the transaction.

-

No Transfer in Recapture Period. To preserve the tax benefits, there should be no purchase option available to the host prior to the sixth anniversary of the commercial operation date of the system. Any transfer in the first five years of operation will likely cause an ITC recapture.

-

Purchase Option Price. What is the purchase option price? The price should be at least fair market value. We often see a floor price (e.g., to ensure any debt can be paid off) in addition to the FMV option, in which case it should be the greater of the floor price and fair market value (although it should be noted that anything but a straight FMV purchase price will add tax pressure to the transaction). The host should not get credit against the purchase price for amounts it has paid for power under the PPA, unless it has not yet received the power for which it paid. Confirm that there is no circumstance that suggests the host is reasonably expected to exercise its purchase option, such as a regulatory or legal requirement for the host to buy the system.

-

System Removal. The project company should be required to remove the system at the end of the PPA term, and such removal should be an economical option.

-

Purchase Reasonably Expected. The PPA should not contain any provisions that could force the host to exercise the purchase option, such as a requirement that the host be responsible or removing, packing and shipping the system at the end of the PPA term.

-

No Transfer upon Default. If the host defaults under the PPA and project company terminates and requires payment of Termination Value, the system should not be transferred to the host. The Termination Value payment should be a penalty and not a back-door purchase option for a fixed fee.

-

Move & Pay. If a move & pay provision is included, the new location should be satisfactory to the project company and the host should be required to pay for all dismantling, moving and reassembly costs, plus any damages and loss of revenues during the moving period.

V. Early Termination Rights.

-

Generally. Does the host have any right to terminate the PPA other than due to a project company default or a force majeure? If so, any such right will be frowned upon and carefully evaluated by your Financing Party – if you must accept such terms, try to negotiate a mitigating factor, such as having the termination right coupled with the obligation to pay Termination Value.

-

Upon Customer Default. If the PPA is terminated due to a host default or any other right of Customer to terminate the PPA in the absence of a project company default, then project company should have the right to terminate the PPA and require the host to pay a scheduled Termination Value, which should be calculated to provide the project company with its expected yield, and include the value of any lost tax benefits as well as the cost of dismantling and removal of the system.

-

Note that there should be a finite limit on host’s right to cure defaults (i.e., in no event longer than 90 days), so that a line can be drawn to start exercising remedies. A “reasonable time” to cure a default without an outside date is often not acceptable. (This is commonly seen in SunEdison-originated forms – and it should be fixed in an amendment or in a third party consent.)

-

As noted above, payment of Termination Value should not entitle host to take title to the system. This should be a penalty, not a veiled purchase option.

-

-

Prior to Commercial Operation Date. Project company may have the unilateral right to terminate the PPA before construction and without liability if (I) it is unable to obtain all interconnection approvals or any other government approvals or permits, (ii) it is unable to get zoning approval for the system, if applicable, or otherwise is unable to install the system at the site, (iii) net metering is not available, if applicable, (iv) it is unable to receive expected rebates or grants, (v) it is unable to procure financing, or (vi) upgrades are required to Customer’s existing electrical infrastructure and Customer will not pay for such upgrades. Any project company rights to terminate the contract are likely not problematic as these are within the project company’s (or financing party’s) control.

VI. Necessary Provisions. The PPA should contain the following provisions:

-

Maintenance of Access Covenant. If the PPA host is the same entity to give the site document or when the access rights are contained in the PPA, the PPA host must provide a covenant that it will always maintain the project company’s access rights to the property and, if it does not, it will be a breach of the PPA that would permit the project company to terminate and collect Termination Value. In lieu of an express covenant, a cross default to the site document or an express default for loss of use of the site is acceptable.

-

System Owner. Project company will be the owner and operator of the system and Host will not take any position that it is the owner of the system or beneficiary of any tax incentives. The PPA host cannot have any opportunity to operate the system during the PPA term – if there is any provision that would permit the host to operate or maintain the system, then it is a potential fatal flaw.

-

Personal Property. The parties agree that the system is personal property and should not be deemed to be a fixture.

-

Service Contract. The parties intend for the PPA to be treated as a “service contract” within the meaning of section 7701(e) of the Internal Revenue Code. (This is especially important to include when the host is a tax-exempt or governmental entity.)

-

Liens. Host agrees to not incur or suffer to exist any liens on the system created through it.

-

Interconnection Maintenance. If host is the party to the interconnection agreement, it should agree to always maintain an interconnection agreement and an interconnection to the local grid.

-

Swimming Pool. Host agrees not to use the system for purposes of heating a swimming pool within the meaning Section 48(a)(3)(A)(i) of the Internal Revenue Code of 1986, as amended. (Although this is seen as a particularly silly rule, the tax code does not permit a system to be used to heat a swimming pool, with the consequence being loss of the system owner’s ability to take the ITC and accelerated depreciation.) I do note, however, that this provision is typically overlooked unless the site is likely to have a swimming pool.

-

Security. For ground-mount systems in particular, the PPA should provide for installation and maintenance of a fencing system for security purposes.

-

Hazardous Substances. The PPA should provide a host indemnity for any liability of the project company relating to hazardous substances not brought onto the site by project company or its contractors. If there is a separate land use agreement, then the environmental indemnity is typically in that document.

-

Force Majeure. The parties will be excused from performance for force majeure events, and may have the right to terminate the PPA without penalty if the force majeure extends beyond a specified time (typically 6 months – 1 year). The definition of force majeure should only include events outside of the control of the party claiming force majeure that could not have been avoided using commercially reasonable measures. There should be no other reason for a host’s excused performance.

VII. Provisions to Watch Out For.

-

Improvements. Project company should not be required to make improvements to the property or roof unless contracted and paid for outside of the pricing of the PPA.

-

Performance Guaranty. Any performance or availability guaranty should be backstopped by the O&M provider to the system under the O&M Agreement.

-

Standby Service Tariff. Some utilities will place a host with on-side generation on what is called a “standby service” tariff. These commonly consist of a fixed monthly contract demand charge and a volumetric charge that is applied to the amount of energy consumed. If this will apply, the host should be responsible for paying it, and these charges should be factored into the net economic benefits to the host associated with the system.

-

Additional Costs. Are there any provisions that require the project company to incur costs beyond the installation and maintenance of the system, like having to provide performance security or pay for restoration insurance? These terms will have to be included in your financial model and should be highlighted for your Financing Party.

-

References to Specific Rules and Regulations. Look for provisions that incorporate other rules, regulations, contractual provisions, etc., into the PPA by reference. These can change or even nullify project company’s rights otherwise set forth in the agreement, and add significant requirements to the PPA, and should therefore be carefully reviewed.

-

Non-Appropriation. If the host is a municipal entity, an appropriation clause will typically be included, stating that the host is only required to pay under the PPA if the funds are appropriated for such purpose in its annual budget. It is helpful if language is included in the PPA that requires the host to use commercially reasonable efforts to appropriate the funds. This is a term that should be highlighted for your Financing Party.

VIII. Assignment and Cooperation with Financing.

-

Assignment. The host should not be permitted to assign the PPA without the prior written consent of project company (or its assignee). Project company should have the express ability to collaterally assign the PPA to a financing party (including any tax-equity vehicle or investor) without consent. (Note that any permission to collaterally assign to a financing party cannot be conditioned on the financing party assuming the PPA obligations – sometimes this language sneaks in and it doesn’t work – a financing party will not assume any obligations until an express assumption of the agreement, which usually only takes place after foreclosure.

-

Cooperation with Financing. It is always helpful to have the host agree to cooperate in all respects with project company’s financing parties in connection with any financing obtained by project company with respect to the system, which will avoid difficult negotiations at the time of financing.

-

In this case, it is typical for Host to agree to provide all documentation required by the financing parties, including a consent to assignment, an estoppel certificate, an opinion of counsel as to corporate and enforceability matters, and if host is a private entity, financial statements either individually or on a consolidated basis with its affiliates, in each case, upon request of any financing party.

-

A. Review Checklist - Power Purchase Agreement/Net Metering Credit Purchase Agreement (for reference purposes only):

|

□Final |

□ Draft |

|

|

Parties: Project Company and (“Host”) |

||

|

Date: [List on Summary] |

||

|

Amendments: [List on Summary] |

||

|

Term of PPA: [List on Summary] Renewal Term(s): [List on Summary] □Yes □ No – Renewal can be prevented by Project Company |

||

|

PPA Pricing: □ Fixed Price $ _______/(month/quarter) □ Variable [Describe on Summary] □Yes □No - Renewal Terms reset to FMV |

||

|

□Yes |

Fully Executed |

If no, list signatures needed on Summary |

|

□Yes |

Address and Project Description |

List on Summary |

|

□Yes |

Assigned from third party to Project Company |

If yes, describe assignment document and consent to assignment in Summary |

|

□Yes |

Purchase Option(s) |

List number of purchase options, dates and whether for fixed price or FMV on Summary (flag as potential fatal flaw if a purchase option occurs prior to 6th anniversary of PPA) |

|

□Yes |

Environmental Attributes accrue to Owner |

If not, ensure that tax benefits are excluded |

|

□Yes |

Site License contained in PPA |

Aim for expiration of the Site License to be 3-6 months after the term. |

|

□Yes |

Cross-defaulted to site document (if separate site document) |

|

|

□Yes |

Municipal Entity |

Note on Summary if non-appropriation clause applies and if there are any mitigating factors |

|

□Yes |

Guaranteed Construction Start Date |

List on Summary |

|

□Yes |

Guaranteed COD |

List on Summary |

|

□Yes |

Letter of Credit or other credit support required |

List on Summary and include any end-of-term restoration security |

|

□Yes |

Host required to purchase 100% of energy produced by system |

|

|

□Yes |

Tax Benefits adequately described and accrue to Owner or its designee |

|

|

□Yes |

Collaterally assignable without Host consent |

|

|

□Yes |

Assignable by Host |

|

|

□Yes |

Performance Guaranty included |

Describe on Summary and note whether it is backed by an EPC/O&M Performance Guaranty |

|

□Yes |

Any provisions for the Host to receive LDs |

Describe on Summary |

|

□Yes |

Host is party to Interconnection Agreement |

|

|

□Yes |

Host required to maintain Interconnection Agreement |

|

|

□Yes |

Service Contract language (Code Section 7701(e)) |

|

|

□Yes |

Agreement that System is Personal Property and not a fixture |

|

|

□Yes |

Host responsible for security/fencing |

|

|

□Yes |

Contains Termination Value schedule |

|

|

□Yes |

Host termination rights outside of Project Company default or Force Majeure |

Describe on Summary |

|

□Yes |

Host is permitted to move equipment |

If yes, confirm that option is not granted prior to the sixth anniversary of COD, the new site must be acceptable to Project Company, all costs of de- installation, moving and re- installation will be paid by Host, and that Host will pay for all estimated lost power based on historical production |

|

□Yes |

Roofing or other construction required |

List on Summary |

|

□Yes |

Host is permitted to cause outages in excess of 48 hours per year |

List on Summary |

|

□Yes |

Force Majeure performance excuse – termination after _____ months |

List on Summary |

|

□Yes |

Force Majeure is solely for major events out of the claiming party’s control and not avoidable by reasonable efforts |

|

4. REVIEWING SITE DOCUMENTS

Every solar project will require some sort of land rights in order to be installed, operated and maintained. There are a handful of ways to get these rights in C&I projects. The easiest way, if your PPA and site document are with the same counterparty, is to include access rights in the PPA. Access rights, like a site license or a facility use agreement, are considered personal property (license) rights and can be secured through a security agreement and perfected by filing a UCC-1 financing statement. Site Leases and Easements are real property rights that can only be secured through recording a mortgage or deed of trust. Regardless of the type of land right the project company has, it should allow for basic access rights for the term of the PPA, plus some reasonable time to de-install or remove the system. Below are the most common provisions to look out for in a site document.

I. Site Document Basics.

-

Site Provider and Owner.

-

Often the host is the same entity that is providing the site document, but occasionally it is not. It is important to understand who owns the property and how the project company has the rights to access the site.

-

Does the host own the property? If not, what documentation do you have showing that the host has the right to occupy the site? The host can only grant whatever rights it has. A title report or other evidence of site ownership should be provided.

-

-

Lessee, Amendments, Execution.

-

Is the lessee the project company? If not, the agreement should be assigned to the project company.

-

Has the Site Document been amended? If so, are the amendments reflected in the description of the Site Document in the financing documents, as well as any third party consent or estoppel?

-

Has the Site Document been fully executed?

-

-

Supplements. Have any landlord consents or NDAs been provided?

-

Project. Does the description, capacity, and location of the project match the other project documents and the financing documents? If not, this should be noted and will need to be fixed.

-

Milestones. Are there any guaranteed milestone dates in the Site Document? Try to avoid these as they are rarely met.

-

Rent. Rent is commonly a nominal amount ($10/year, for example) in a C&I project, but can be substantial, particularly in a Virtual Net Metering or small utility deal and should always be included in your financial model.

-

Term. In order to be considered a true owner of a project for tax purposes, the owner must have the ability to operate the asset for its useful life. The average useful life for a photovoltaic solar project is around 35 years, and this will be confirmed in the appraisal. It’s for this reason that we always make sure that either the term of the site lease is extendable to at least 35 years or that it makes economic sense to remove and relocate the system to be operated elsewhere. One can typically get an appraiser to support the idea that it’s economically viable to relocate a project that is 2.5MW and under, in which case a site agreement that is co-terminous with a PPA is acceptable, but it is always advisable to get appraisal support for this assumption. If you have a site lease with a term (including extension terms) that is less than 35 years, it’s always good to consult a tax colleague and flag for the client in the diligence summary.

-

Termination. The Landlord should have no ability to terminate the Site Document outside of a project company default or a force majeure (after at least six consecutive months). Any other termination right is a potential fatal flaw.

-

Credit Support. Note if any credit support is required to be provided from the project company – the amount, type and duration should be evaluated, as your Financing Party will likely require that you maintain this in cash or through a separately- maintained letter of credit. This includes any credit support required for site restoration obligations.

II. Site.

-

Type.

-

Is it a landfill site or another site with the potential for hosting hazardous waste? Has a Phase I Report been done and reviewed? We like to see a solid environmental indemnity from the host covering all existing hazardous substances at the site and all violations of environmental laws going forward that are not caused by the project company or its contractors. If the project company could have environmental liability at the site, you should consider how to address this and be ready for questions from Financing Parties.

-

Is it a rooftop project? If so, then you do not need a Phase I, but may need building access rights as well as land access rights. If the host owns the building, but not the land, what rights do you have from the landowner?

-

Is the land BLM (Bureau of Land Management) or other government land? If so, this often comes with other requirements and approvals – it’s good to talk to your real estate counsel about this.

-

-

Legal Description. Does the legal description of the site match the location of the project? Sometimes these are terribly mismatched.

-

Title Search. Have you performed a title search to confirm that the host is the owner or lessee of the property and to identify third parties with an interest in the real property? Mineral rights are important to note because in many states they trump surface rights (which are the project company’s rights to build a project on the surface). A Financing Party will require this, so why not ask for it upfront.

III. Site Access and Security.

What land rights are being granted? The project company needs to have rights to access the site where the project will be located. Generally, there are 3 different scenarios to consider.

-

License

-

Often seen as “access rights” in the PPA, or specifically named as a license. This is a contractual right to access the site, which can include an exclusive right to receive sunlight on the site.

-

The access rights should include the right “to enter onto the property to install, maintain, repair, replace and remove the system.” Make sure each of these activities is covered.

-

A license is a contractual right, not a real property right, so it will not survive foreclosure or sale of the property unless the relevant third party agrees to continue to provide the license. This is fine if the PPA and the site document are with the same party and the documents are cross-defaulted. You will want to make sure that if the PPA host fails to provide access to the location of the system (if it stops doing business at the site or loses its lease, for example) and an acceptable substitute site is not agreed to by the project company, then it’s a default under the PPA and the project company can charge the termination value.

-

A memorandum of license can be recorded in the land records if the client desires to do so, but it is not required for validity of the license.

-

-

Site Lease or Easement.

-

A site lease or easement provides another layer of protection to the project company, since it is a real property right that runs with the land. It should survive foreclosure or sale of the property. It’s very important to have this protection in any Virtual Net Metering project and every other situation where the host under the PPA is not the same person providing the site access.

-

A memorandum of site lease or easement can be recorded in the real estate records to let future owners of the property know of the existence of the project company’s real property interest in the site.

-

If the Site Lease or Easement is with the PPA host, rent will typically be nominal. If it is with a separate party, the rent may be substantial and should be noted in the financial model.

-

If the tax equity transaction is a sale/leaseback, then the financing party will likely be taking a security interest in the site document which, if it is a site lease or an easement, can only be done with a mortgage on the leasehold or easement interest. The mortgage document form will vary by state and can come with hefty recording fees. If the site provider and the PPA host are the same person and the documents are cross-defaulted, and if there is a third party consent providing a contractual right to step into the site lease or easement upon a default, then some tax equity providers have taken the position that they have enough contractual protection and decided to forego the expenses of drafting and recording a mortgage. If you’re in this situation, call me and we can talk about who will finance this.

-

If the site document provides rights to a site from a true third party (such as for a Virtual Net Metering or small utility project), then the financing party will likely want title insurance in addition to a recorded mortgage. There is typically no reason to get title insurance for a site lease or easement given by the PPA host (if the PPA and site lease are cross-defaulted). If the project is small and there is a clean title report, then some parties might get comfortable without title insurance if it is expensive – but if there are other interests in the site, like mineral rights, then these can trump surface interests and people will likely want the title insurance.

-

-

Real Estate Rights Term. The real estate rights should be at least co-extensive with the PPA term (including renewals), and it is recommended that the real estate rights extend for 90-180 days beyond that term for purposes of removal of the system from the property. It is worth noting if the project company can stay on the land post PPA and sell to a different offtaker – this is typically only the case with Virtual Net Metering and utility projects, but they occasionally are allowed in other situations.

-

Fixture Filings. Does the Site Document permit you to file a fixture filing on the property? Although the system must constitute personal property and not a fixture, a “protective” or “precautionary” fixture filing may be filed, which puts the world on notice that the system is personal property owned by a third party. This is mostly done when the project company has access rights only and does not record a license or site lease.

-

NDAs and Landlord Consents. If there is any third party with an interest in the real property (such as a landowner, building owner, mortgagee, mineral rights holder, etc.), then you should seek a consent or non- disturbance agreement from all such parties. Such consent or NDA should disclaim any rights to the system, state that the system will be treated as personal property of the system owner, and affirm the project company’s access rights. These consents and NDAs can be put in a form to be recorded in the real estate records, but do not have to be.

IV. Expected Provisions.

-

Liens. Host agrees to not incur or suffer to exist any liens on the system created through it.

-

Property Taxes. The site provider should be required to pay property taxes, but the project company is typically required to pay any increased taxes due to the system being located on the premises.

-

Disclaimer of Interest. Site provider should acknowledge somewhere that the project company (or its assigns) is the owner of the solar facilities and that site provider has no claim to them.

-

Security. For ground-mount systems in particular, if the site document is provided by the PPA host and the system is co-located with the host’s business, the site document (or the PPA) should provide for the site provider’s installation and maintenance of a fencing system for security purposes.

-

Environmental Indemnity - Hazardous Substances. The site document should provide a site provider indemnity for any liability of the project company relating to hazardous substances not brought onto the site by project company.

-

Condemnation. Upon a total taking, it is common for the site document to terminate. Upon a partial taking, the project company should have the option to terminate the site document.

-

Casualty. The site document should not terminate due to a casualty – the project company should have the right to rebuild.

V. Provisions to Watch Out For.

-

Estoppels. Occasionally, you may see a requirement that if an estoppel is requested by the landlord, then it must be provided by the project company within X days or else all defaults are deemed cured. This is not an acceptable provision to most Financing Parties, so try to remove it or at least remove the “deemed cured” part.

-

Improvements. Project company should not be required to make improvements to the property or roof unless contracted and paid for outside of the project pricing.

-

Surface Damage. Any provision for the project company to compensate the site provider for any damage to the surface or crop damages will be reviewed carefully by a Financing Party and the developer will likely be required to absorb these costs.

-

Restoration Obligations. It is expected to see a provision stating that the project company will remove the system at the end of the term and restore the site to its original condition, ordinary wear and tear excepted. A Financing Party may require that any extensive site restoration obligations, such as landscaping or planting requirements and any site restoration security or payments that are required be reserved upfront by the developer – and these can get pretty expensive.

-

Assignment. The site provider should not be permitted to assign the site document without the prior written consent of project company. Project company should have the express ability to collaterally assign the site document to a financing party (including any tax-equity vehicle or investor) without consent. (Note that any permission to collaterally assign to a financing party cannot be conditioned on the financing party assuming the site document obligations – sometimes this language sneaks in and it doesn’t work – a financing party will not assume any obligations until an express assumption of the agreement, which usually only takes place after foreclosure. Also be sure to note if any third party notice is required to be sent upon a collateral assignment to a financing party (this is typical if there is a third party who owns the site).

A. Review Checklist - Site Documents (for reference purposes only)

|

□Final |

□ Draft |

|

|

Parties: Project Company and ____________ (“Landlord”) □Yes □No – Same party as PPA Host |

||

|

Date: [List on Summary] |

||

|

Amendments: [List on Summary] |

||

|

Term: [List on Summary] Renewal Term(s): [List on Summary] □Yes □No Coterminous with PPA (note if not at least 60 days after PPA term) |

||

|

□Site Lease □ Easement (security interest will require a mortgage)] * Consider whether a mortgage or title insurance will be required for the project |

||

|

□ Site License □ Facility Use Agreement (security interest can be created in a security agreement) |

||

|

Rent Amount: [List on Summary] |

||

|

□Yes |

Fully Executed |

If no, list signatures needed on Summary |

|

□Yes |

Address and Project Description |

List on Summary |

|

□Yes |

Assigned from third party to Project Company |

|

|

□Yes |

Property legal description matches address |

|

|

□Yes |

Title/lien search done to confirm ownership of property |

|

|

□Yes |

If rooftop system, land document covers building and land |

|

|

□Yes |

Property owned in fee by Landlord |

If no, then is there an acceptable owner consent from □ building owner and □ land owner |

|

□Yes |

Cross-defaulted to PPA |

|

|

□Yes |

Property is mortgaged or affected by other liens |

If yes, then has an acceptable NDA been received |

|

□Yes |

Site restoration required at end of Term |

|

|

□Yes |

Credit Support requirements |

List on Summary and include any end-of-term restoration security |

|

□Yes |

Environmental Indemnity for all hazardous substances not brought to site by Project Company (or its contractors) |

|

|

□Yes |

Guaranteed Construction Start Date |

List on Summary |

|

□Yes |

Guaranteed COD |

List on Summary |

|

□Yes |

Collaterally assignable without Landlord consent |

|

|

□Yes |

Assignable by Landlord |

|

|

□Yes |

Landlord is permitted to cause outages in excess of 48 hours per year |

Describe on Summary |

|

□Yes |

Any provisions for the Landlord to receive LDs |

Describe on Summary |

|

□Yes |

Agreement that System is Personal Property and not a Fixture |

|

|

□Yes |

Host responsible for security/fencing |

|

|

□Yes |

Host termination rights outside of Project Company default or Force Majeure |

Describe on Summary |

|

□Yes |

Landlord is permitted to move equipment |

If yes, confirm that option is not granted prior to the sixth anniversary of COD, the new site must be acceptable to Project Company, all costs of de- installation, moving and re- installation will be paid by Landlord, and that Landlord will pay for all estimated lost power based on historical production: □ |

|

□Yes |

Roofing or other construction required |

List on Summary |

|

□Yes |

Force Majeure performance excuse – termination _________ after months |

List on Summary |

|

□Yes |

Force Majeure is solely for major events out of the claiming party’s control and not avoidable by reasonable efforts |

|

5. REVIEWING INTERCONNECTION AGREEMENTS

Interconnection agreements for C&I solar projects are generally pretty straightforward and easy to review. There are a few basic things to look for – primarily, who is party to the agreement? If the project is located at the PPA host’s site, then the host is usually party to the interconnection agreement with its local utility. In that case, the project company is not a party and the financing parties will not be taking an interest in the agreement, so review will be limited and you will want to make sure that the PPA requires the host to maintain the agreement. Interconnection agreements typically only become complex documents requiring regulatory review when you are dealing with larger utility projects.

If your interconnection agreement is between the host and the local utility, you will want to make sure (i) the parties, site, project and other details match the PPA, (ii) the interconnection agreement permits net metering or the ability for the project to put power onto the grid (and this ability is not capped), (iii) any interconnection upgrades the document requires are expected to be completed prior to commercial operation of the project and any associated costs are paid prior to financing, (iv) the term of the interconnection agreement is at least as long as your PPA, including renewal terms, (v) the interconnection provider is not permitted to shut down the system or terminate the agreement except for emergencies and for common events of default, and (v) there is no onerous or costly obligation aside from maintaining the project facilities in working order and abiding by applicable laws and regulations. If the interconnection agreement is with the project company (in a Virtual Net Metering or small utility deal), then you will also need to make sure the same type of collateral assignment provisions are included as in the PPA. If the project company is party to the interconnection agreement, then the delivery point should be the meter installed pursuant to the PPA (or, more typically in larger utility projects, a substation) – the PPA and IA delivery points should match. If the host is party to the interconnection agreement, then there may be two meters – one to measure the project output to the host, and one to measure power going to and from the grid, so the PPA and IA delivery points may not match.

The commencement of the term of the interconnection agreement is typically conditioned upon the utility inspecting the system connection and issuing “PTO” or permission to operate. Many utilities will not countersign the interconnection agreement until PTO is issued.

A. Review Checklist – Interconnection Agreement (for reference purposes only)

|

□Final |

□ Draft |

|

|

Parties: Project Company and ________________ (“Transmission Provider”) |

||

|

Date: [List on Summary] |

||

|

Amendments: [List on Summary] |

||

|

Guaranteed Milestone Dates: [List on Summary] |

||

|

Term: [List on Summary] Renewal Term(s): [List on Summary] □Yes □No Coterminous with PPA |

||

|

□Yes |

Fully Executed |

If no, list signatures needed on Summary |

|

□Yes |

Address and Project Description |

List on Summary |

|

□Yes |

Assigned from third party to Project Company |

|

|

□Yes |

Delivery point matches description in PPA (on-site meter or substation) |

|

|

□Yes |

Collaterally assignable without Utility consent (only matters if Project Company is the counterparty) |

|

|

□Yes |

Net Metering is permitted – if yes, list any cap or restriction on net metering in the Summary |

|

|

□Yes |

Improvements required |

If yes, estimated cost: $[List on Summary] – Evidence of payment: |

|

□Yes |

Credit support required |

If yes, list amount, type and duration on Summary |

|

□Yes |

Utility termination rights outside of Project Company/Host default |

Describe on Summary |

|

□Yes |

Curtailment permitted outside of an emergency or failure to abide by applicable laws |

|

6. REGULATION AND PERMITTING REVIEW

Most C&I solar projects will have few regulatory and permitting requirements, as most are QFs (Qualifying Facilities) and not large enough to be an EWG (Exempt Wholesale Generator) or require MBR (Market Based Rate) Authority. The installation permitting is typically covered by the EPC contractor, and the financing documents should require the developer to disclose what operating permits are required. If you are working in a new state, it’s good to ask your regulatory lawyers to give you an overview of the local requirements.

Federal Regulatory Permitting

Since the typical C&I project will not be required to file for EWG status or MBR Authority, we will only focus on QF status for purposes of this manual. However, if the system size is greater than 20MW AC (or the system could ever produce more than 20MW AC at any time), then you will need MBR Authority and should talk to a regulatory specialist.

If the system size is greater than 1MW AC but less than 80MW AC, then you should file for QF status in order to be eligible for PURPA’s special rate and regulatory treatment for Qualifying Facilities. Qualifying Facilities equal to 1MW AC and under do not have to file. Filing consists of a simple online self-certification, and evidence of the filing consists of an email showing the self- certification was made. Note that if there are multiple projects located within 1 mile of one another owned by the same entity or its affiliates, the aggregate capacity of all such projects will be counted to determine if they have to file for QF status. The benefits that are conferred upon QFs by federal law generally fall into three categories: (1) the right to sell energy or capacity to a utility, (2) the right to purchase certain services from utilities, and (3) relief from certain regulatory burdens.

A. Regulatory Checklist

|

□Yes |

||

|

□Yes |

≥1 MW AC – Requires QF Self- Certification |

If multiple systems, then include aggregate amount of capacity within 1 mile |

|

□Yes |

>30 MW AC – EWG |

Get regulatory specialist review |

|

□Yes |

>20 MW AC – MBR Authority required |

Get regulatory specialist review |

|

□Yes |

Section 203 Filing Required |

Ask a regulatory specialist if this filing is required if your transaction involves the purchase or sale of an operating project in excess of $10,000,000 |

|

□Yes |

HSR Act Filing Required |

If the deal is over $78 million, ask your lawyers to see if an HSR filing will be required |

|

□Yes |

State PUC Approval Required |

Typically only for utility deals, but the PPA should indicate whether this is a requirement |

|

□Yes |

Any applicable state filings or approvals required |

If yes, list in Summary |

|

□Yes |

Phase 1 received (not required for rooftop) |

Any Phase 1 identified issues should be listed in the Summary |

|

□Yes |

Approvals listed on datasite |

If yes, list any non- construction permits on Summary |

7. REVIEWING INCENTIVE DOCUMENTS

Incentive documentation will vary from state to state. Some documents, like the Connecticut Z-REC or New York NYSERDA program documents, look much like PPAs. Others, like contracts for the sale of SRECs in New Jersey and Maryland, look more like commodity documents and may not be site-specific. The most important thing to do in reviewing incentive documentation is to follow the money. The gating question is whether or not the incentive payments are being factored into your financing party’s pricing – if not, then their review will be limited. If the incentives are included in pricing, then you will want to note how much money will be paid under the contract, for how long and to whom. Is it a contract for the sale of a specific number of SRECs at a particular price, where there’s a penalty for not meeting the required load? Or does it provide for an incentive for your specific project with pricing that varies based on production?

You should note what exactly is being purchased – for instance, an example contract would be for the sale of 1,500 2017 SRECs, 1,500 2018 SRECs and 1,500 2019 SRECs with a fixed price per SREC. If the project will reach commercial operation in December of 2017, then it won’t be able to fill the 2017 vintage SREC order and this could be a flaw that would change the deal pricing. Note any caps, any penalties and any counterparty termination rights. In most instances, you will want to treat your REC agreement similarly to a PPA, since it is a revenue contract, and you will want third party consents or estoppels, as applicable. Accordingly, the REC counterparty credit is important and you should pay specific attention to the parties to the contract – it should be between the project company and the REC counterparty that has been approved by the financing party. REC contracts typically have some sort of cliff date or will require a separate authorization. It is important to read the contracts carefully to determine what milestone dates need to be met and what additional documentation may be required.

Occasionally, state tax credits are factored into pricing – often in Hawaii and North Carolina deals. Ask your tax specialist if there are state tax credits available in any new state you are working in.

A. Review Checklist – Incentive Documents (for reference purposes only)

|

□Final |

□ Draft |

|

|

State: ____________________ |

||

|

Parties: Project Company and ____________________ (“REC Purchaser”) |

||

|

Date: [List on Summary] |

||

|

Amendments: [List on Summary] |

||

|

Term: [List on Summary] Renewal Term(s): [List on Summary] |

||

|

Pricing: □ Fixed Price $ ______/(REC)□ Variable [Describe on Summary] □Yes □No – Quantity or Vintage Year Requirement [Describe on Summary] *List payment timing on Summary |

||

|

□Yes |

Fully Executed |

If no, list signatures needed on Summary |

|

□Yes |

Address and Project Description |

List on Summary |

|

□Yes |

Assigned from third party to Project Company |

|

|

□Yes |

Project-specific requirements |

|

|

□Yes |

Are incentives capped |

If yes, describe in Summary |

|

□Yes |

State tax credits available |

|

|

□Yes |

Collaterally assignable without REC Purchaser consent |

|

|

□Yes |

Assignable by REC Purchaser |

|

|

□Yes |

Any provisions for REC Purchaser to receive LDs |

Describe on Summary |

|

□Yes |

Contains Termination Value schedule |

|

|

□Yes |

REC Purchaser termination rights outside of Project Company default or Force Majeure |

Describe on Summary |

|

□Yes |

Force Majeure performance excuse – termination after _______ months |

List on Summary |

|

□Yes |

Force Majeure is solely for major events out of the claiming party’s control and not avoidable by reasonable efforts |

|

8. REVIEWING EPC CONTRACTS

A good, financeable EPC Contract in a C&I solar deal is an installation contract that allocates as much engineering, construction and procurement risk to the contractor as possible, since the contractor is typically the best person to manage those risks. The key objectives of the contract are to get the project built in a manner that meets the project company’s specifications and the other project document requirements, and to get it built on time because there will be revenue loss and often revenue contract loss or penalty payments for delays. The third key objective is to get the project built at a fixed price because another key axiom of project finance is that most of these are non- or limited recourse transactions. There is a defined pool of money and a budget – and the higher project company’s capital costs, the lower its return.

I. Diligence Basics

The most typical construction contract in for a C&I solar project is a “turn-key” contract. That means that the contractor is the person with the sole responsibility to get the project built – often called a “full wrap.” So if a subcontractor fails to perform from the project company’s perspective it’s the contractor’s responsibility. If instead of a turn-key EPC contract, you have various construction and engineering contracts, this should be flagged and discussed with clients before continuing review. For C&I solar deals, the installation is not complex enough to warrant various contracts and the finger-pointing risks that come along with such a structure.

Financing Parties will undertake due diligence review of the contract on at least four levels. One is the technical review done by an independent engineer. The independent engineer assesses the contract, looks at the technical specifications, liaises with the contractor, makes a determination as to whether the project is installed and works as intended, and puts its conclusions in the independent engineer’s report, which is delivered to the financing party as a condition to closing. The second piece of that review, of course, is legal review. The Financing Party will review the contract and assess the risks to determine whether it’s a market contract -- whether there are risks that are outside market norms. If the C&I project is large enough to warrant incurring the costs of an independent reviewer, the third reviewer will be an insurance advisor, who will look at the insurance package. Finally, the financing party does a business review, looking at the economics of the contract.

II. Reviewing by Financing Type

If your Financing Party is reviewing an EPC contract for a sale/leaseback transaction, then closing will likely take place after substantial or perhaps final completion and will consequently be largely performed before the financing party makes an investment. Accordingly, it will read through the contract but only focus on obligations and requirements that will survive substantial completion – such as warranties, indemnities and performance guarantees. They will want to note milestone deadlines for substantial and final completion and penalties for not meeting the deadlines, as well as any responsibilities of the project company that could survive substantial completion. Also note how much money is expected to be unpaid as of the substantial completion date – they will want to see a conditional lien waiver from the contractor as a condition to closing saying how much money is left outstanding on the contract and the financing party will likely want to keep that amount in reserve.

If your Financing Party is reviewing an EPC contract for a partnership/flip transaction, then initial closing will take place after mechanical completion and the final closing will take place after substantial completion. In addition to the items you would note for a sale/leaseback review, you should note the timing and difference between mechanical and substantial completion, and any risks that could arise between those two dates.

If your Financing Party is reviewing an EPC contract for a construction loan, then it will want to perform a full review of the document from start to finish.

III. Contractor Responsibilities

The contractor should be responsible for all the engineering and design work, construction and construction management – and for providing that work in accordance with Prudent Industry Practice, applicable law, permits, project documents and applicable incentive programs. Construction management is managing all the subcontractors (if any) and the like and making sure everyone is working together toward a common goal. The contractor is generally responsible for procurement of all equipment and materials and, to the extent that it is not itself an equipment provider, it will subcontract with vendors to provide that equipment. It will provide all construction labor and personnel. The contractor will also be responsible for permitting, although a contractor will only typically be responsible for permits that are customarily obtained in the name of the contractor. There may be permits which, by their nature, have to be obtained by the project company. Usually, there’s some provision for training of the project company’s or operator’s personnel. And there will be reporting requirements -- typically a monthly progress report setting forth progress the contractor has made toward meeting milestones and the like, any problems it has encountered, and any expectations of changes in the scope. The contractor should also be responsible for providing an O&M Manual for the project. The other way in which the contract defines the contractor’s scope is through what is typically Exhibit A or 1 to any construction contract, and that’s the technical scope exhibit. This is a key document and is generally the domain of the engineers.

IV. Project Company Responsibilities

The project company’s principal obligation in an EPC contract is to pay money for performance. The project company will have other obligations that will include providing the site and necessary access rights to the site. It may also include a provision for something called a construction lay down area, where the contractor puts its stuff while it’s building the facility – if this is included and your PPA is with a business, you should make sure the PPA provides for similar requirements. If there are utility upgrade requirements on the project company in the interconnection agreement, you should make sure these requirements are passed through to the contractor in the scope of work or through a change order.

V. Important Milestones

There are three events in the process of construction that are critical. These events are defined in most, if not all, construction contracts using the following terms:

-

Mechanical Completion. Mechanical completion means that the facility is physically complete, except for testing and punch list items – essentially, the is ready to be turned on safely and is ready for performance testing. In a partnership/flip transaction, this definition becomes important because the financing party will have to invest prior to the project’s placed in service date. If the mechanical completion definition includes that all testing is done and power is being sold under the PPA, then that will be a problem.

-

Substantial Completion. Substantial Completion occurs when mechanical completion has occurred, the facility is ready to be put into commercial operation, the performance tests have been completed and the capacity performance guarantees (if any) have been satisfied. This is typically when transfer of title and risk of loss occurs.

-

Final Completion. Final Completion means that substantial completion has occurred, the punch list has been completed and all other work (like delivery of as-built drawings) has been completed.

VI. Performance Guarantees

Performance guarantees can vary from deal to deal – sometimes there is a capacity guaranty (or bonus) measured at substantial completion showing how much capacity was built - this is particularly important to focus on in transactions where the PPA requires a certain minimum (or maximum) output (and note that bonuses are only appropriate when the PPA provides that the project company will be compensated for excess generation and when the PPA host has the energy appetite to use the excess capacity). Sometimes when the EPC contractor and O&M provider are the same, there will be a performance guaranty guaranteeing a certain level of capacity and efficiency over maybe five years, with exceptions for any activities outside of the contractor’s control – but these guarantees are most often contained in the O&M Agreement and subject to a cap of annual O&M fees, which is a small amount. It’s also important to note when there are performance guarantees to have the IE review them – it’s good to have an engineer look at the mechanics to make sure the test is designed to properly measure what it’s intended to measure.

For C&I projects, the overall contractor liability cap is typically 100% of the contract price, with some exceptions for third party liability, gross negligence, fraud and willful misconduct.

VII. Payment Provisions

Typically, installments are paid based on completion of milestones. There will be a milestone schedule that includes milestones like “start of construction” or “issuance of the notice to proceed”, pay $5 million; “completion of engineering”, another $10 million; installation of certain equipment, $10 million. In some contracts, payments are made based on the percentage of the work completed. The payment provisions will also provide for something called retainage. Retainage is an amount that project company holds back from each payment -- typically from 5 to 10% of the amount that’s due to contractor. Retainage is held back as a form of security for contractor’s performance. If, for example, contractor doesn’t complete some portion of the work as and when it’s supposed to, project company may be able to go in using retainage money to pay someone else to do the work. Owner may also set-off retainage amounts against liquidated damages. It’s a way of keeping the contractor interested, of keeping her around, because she knows that she has to get project company to substantial completion to get most of the retainage money and then to final completion to get the rest of the retainage money.

VII. Change Orders