/>i

/>iAnalyses in this report are based on 2,116 securities class actions filed after passage of the Private Securities Litigation Reform Act of 1995 (Reform Act) and settled from 1996 through year-end 2022. See page for a detailed description of the research sample. For purposes of this report and related research, a settlement refers to a negotiated agreement between the parties to a securities class action that is publicly announced to potential class members by means of a settlement notice.

2022 Highlights

In 2022, the number of settled cases reached its highest level in 15 years, increasing 21% relative to 2021. The median settlement amount, median “simplified tiered damages,” and median total assets of the defendant issuer also rose dramatically.1 |

||

|

|

|

Figure 1: Settlement Statistics

(Dollars in millions)

|

|

2017–2021 |

2021 |

2022 |

|

Number of Settlements |

395 |

87 |

105 |

|

Total Amount |

$16,714.3 |

$1,932.4 |

$3,805.5 |

|

Minimum |

$0.3 |

$0.7 |

$0.7 |

|

Median |

$10.2 |

$8.9 |

$13.0 |

|

Average |

$42.3 |

$22.2 1 |

$36.2 |

|

Maximum |

$3,496.8 |

$202.5 |

$809.5 |

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented.

Author Commentary

Findings

The year 2022 was a record year for settlement activity. The number of securities class action settlements in 2022 increased sharply from 2021 and reached levels not observed since 2007. This sharp increase was accompanied by dramatic growth in case settlement amounts, “simplified tiered damages” (our rough proxy for potential shareholder losses), and the size of issuer defendant firms.

The historically high number of settlements in 2022 can be explained by the elevated number of case filings in 2018–2020, when over 70% of these settled cases were filed.

The median settlement amount is the highest since 2018. This was likely driven by the record-high level of “simplified tiered damages,” an estimate of potential shareholder losses that our research finds is the single most important factor in explaining settlement amounts.

The all-time-high median “simplified tiered damages” reflects a number of factors such as larger issuer defendants (measured by the company’s total assets) and larger disclosure dollar losses (a measure of the change in the issuer defendant’s market capitalization following the class-ending alleged corrective disclosure). Institutional investors are more likely to serve as lead plaintiffs in larger cases, i.e., cases with relatively high “simplified tiered damages.” Consistent with this observation, institutional investor involvement as lead plaintiffs for 2022 settled cases was higher than the prior year and the 2017–2021 average. Larger cases also tend to take longer to settle, and accordingly, we observe an increase in the median time to settlement in 2022 relative to prior years.

2022 was an interesting year as settlement activity reached historically high levels across several dimensions, including the number and size of settlements, and a record-high for our proxy for potential shareholder losses.

Dr. Laarni T. Bulan

Principal, Cornerstone Research

In contrast to the historic highs, settlements in relation to our proxy for potential shareholder losses declined sharply. In particular, both the median and average settlement as a percentage of “simplified tiered damages” in 2022 fell to their lowest levels among post–Reform Act years. These low levels are consistent with a low presence in 2022 of factors often associated with higher settlement amounts, such as the presence of an SEC action, criminal charges, or accounting irregularities.4

Securities class action settlements in 2022 involved substantially larger cases with larger issuer defendant firms. Overall, these cases took longer to resolve and reached more advanced litigation stages before settlement than in prior years.

Dr. Laura E. Simmons

Senior Advisor, Cornerstone Research

Looking Ahead

In light of the reduced level in the number of securities class action case filings in 2021–2022, we may begin to see a slowdown or flattening out in settlement activity in the upcoming years,5 absent a decrease in dismissal rates.

Given that SEC enforcement actions have tended to increase subsequent to when a new SEC Chair is sworn in (which last occurred in 2021), we may also begin to see a reversal in the frequency of corresponding SEC actions among settled cases in the near term. For additional details, see Cornerstone Research’s SEC Enforcement Activity: Public Company and Subsidiaries—FY 2022 Update.

As discussed in Cornerstone Research’s Securities Class Action Filings—2022 Year in Review, certain issues have emerged as focus areas in securities class actions. In particular, 26% of all core federal filings in 2020–2022 were related to special purpose acquisition company (SPAC), COVID-19, or cryptocurrency matters. While very few of these types of cases have settled to date, we expect increased settlement activity for these cases in the future.

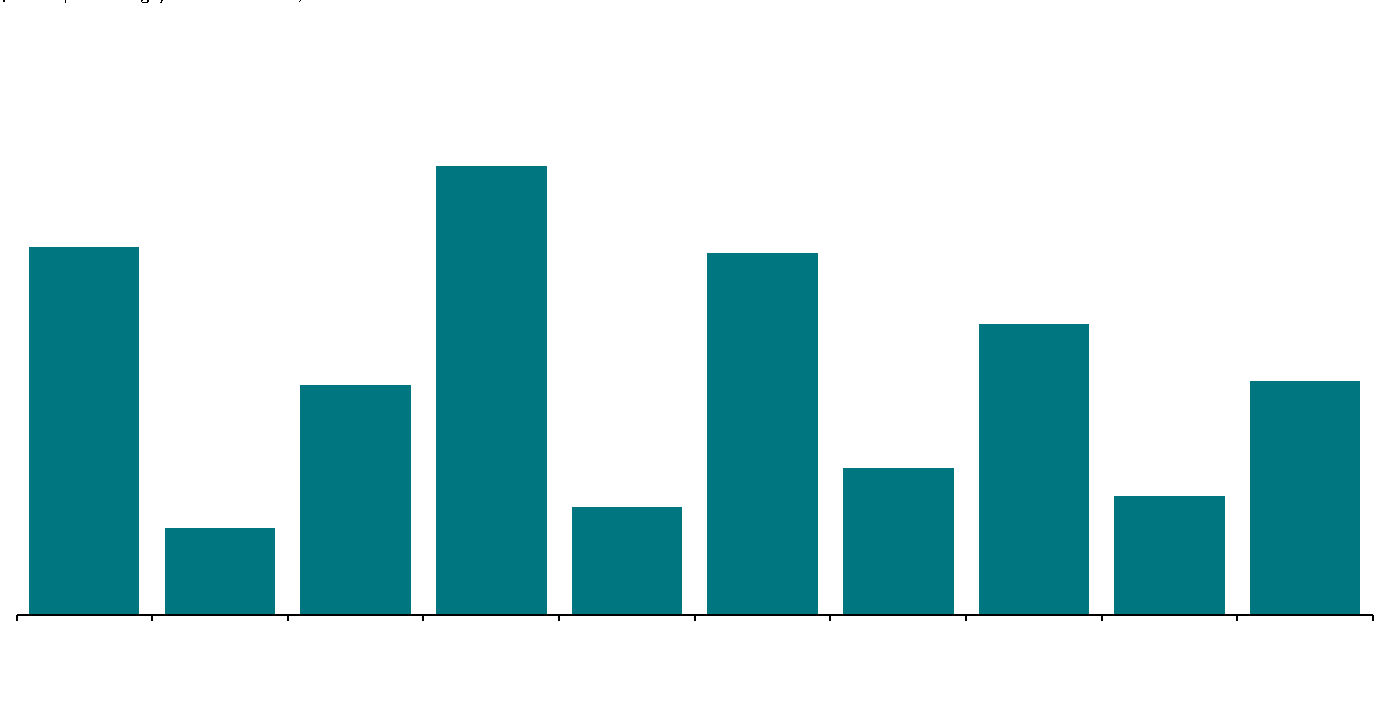

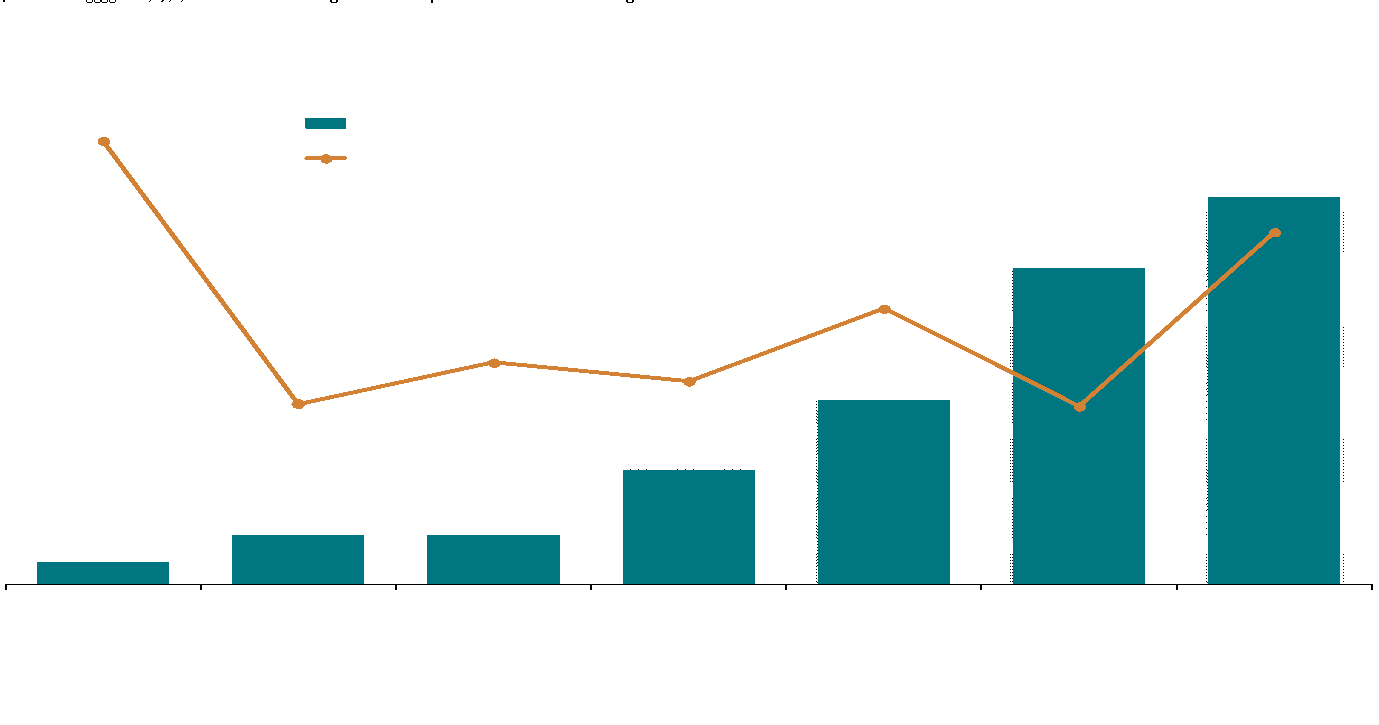

Total Settlement Dollars

As has been observed in prior years, the presence or absence of just a few very large settlements can have a substantial effect on total settlement dollars for a given year.

-

The number of settlements in 2022 (105 cases) continued the upward trend since 2019 and represented a 38% increase from the prior nine- year average (76 cases).

-

An increase in the number of mega settlements (i.e., settlements equal to or greater than $100 million) contributed to total settlement dollars nearly doubling in 2022 compared to the prior year.

-

There were eight mega settlements in 2022, ranging from $100 million to $809.5 million. Eight such settlements is the highest number since 2016.

-

A decline in the proportion of very small settlements further contributed to the growth in total settlement dollars. Only 23% of settlements in 2022 were for less than $5 million, compared to 33% of cases settled in the prior nine years.

The number of settlements in 2022 was the highest number since 2007.

Figure 2: Total Settlement Dollars

2013-2022

(Dollars in Billions)

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented. “N” refers to the number of cases.

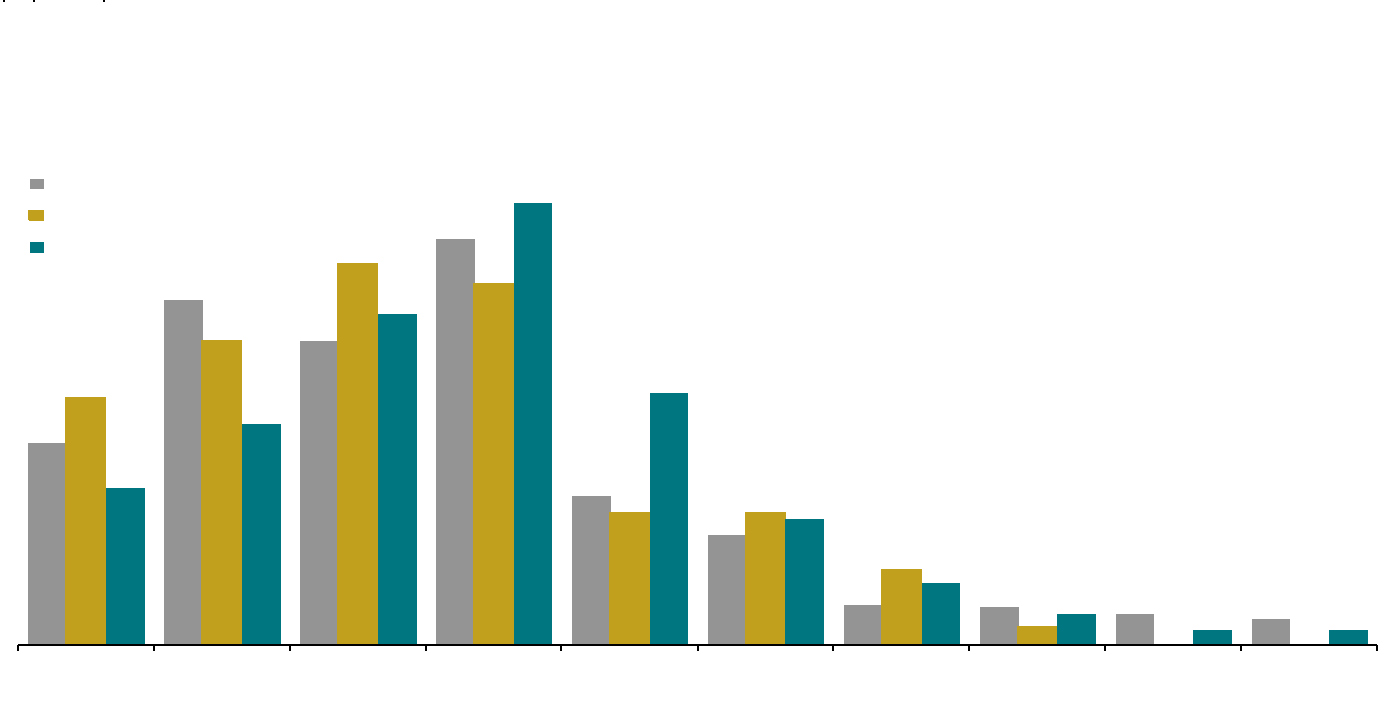

Settlement Size

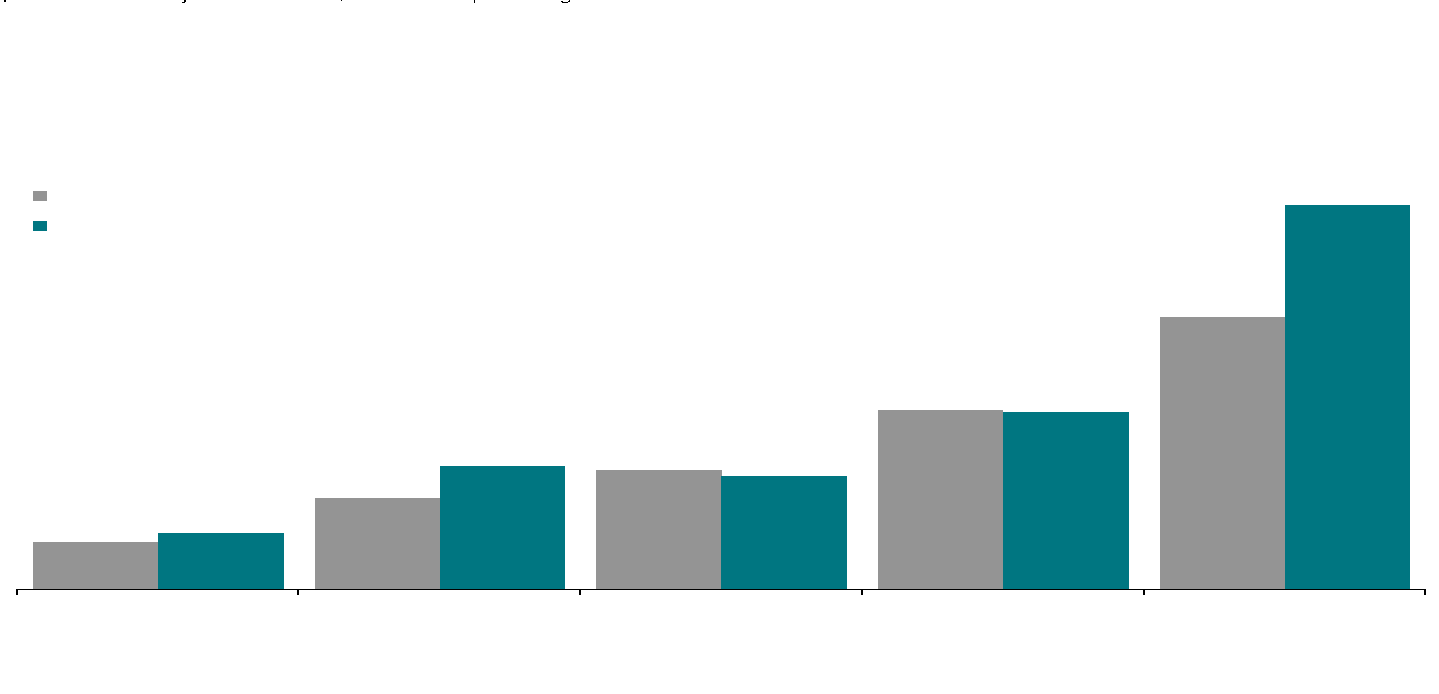

-

The median settlement amount in 2022 was $13.0 million, a 46% increase from 2021 and a 34% increase from the prior nine-year median. Median values provide the midpoint in a series of observations and are less affected than averages by outlier data.

-

The average settlement amount in 2022 was $36.2 million, a 63% increase from 2021. (See Appendix 1 for an analysis of settlements by percentiles.)

-

In 2022, 42% of cases settled for between $10 million and $50 million, compared to only 30% in 2021 and 34% in 2013–2021.

The median settlement amount in 2022 was the highest since 2018.

-

The increase in the proportion of these “midsize” settlement amounts ($10 million to $50 million) was accompanied by a decrease in the proportion of cases that settled for less than $10 million—43% in 2022 compared to 56% in 2021 and 51% in the prior nine years.

Figure 3: Distribution of Settlements

2013–2022

(Dollars in millions)

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented.

Type of Claim

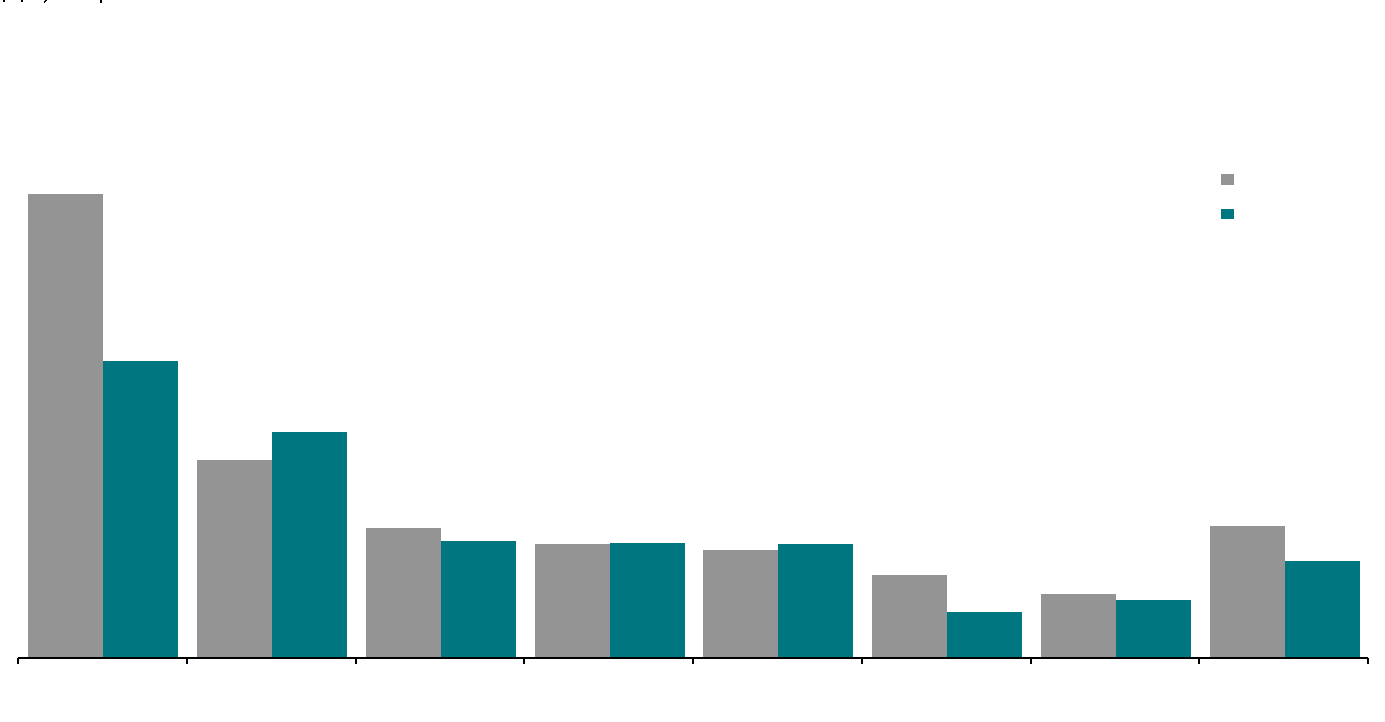

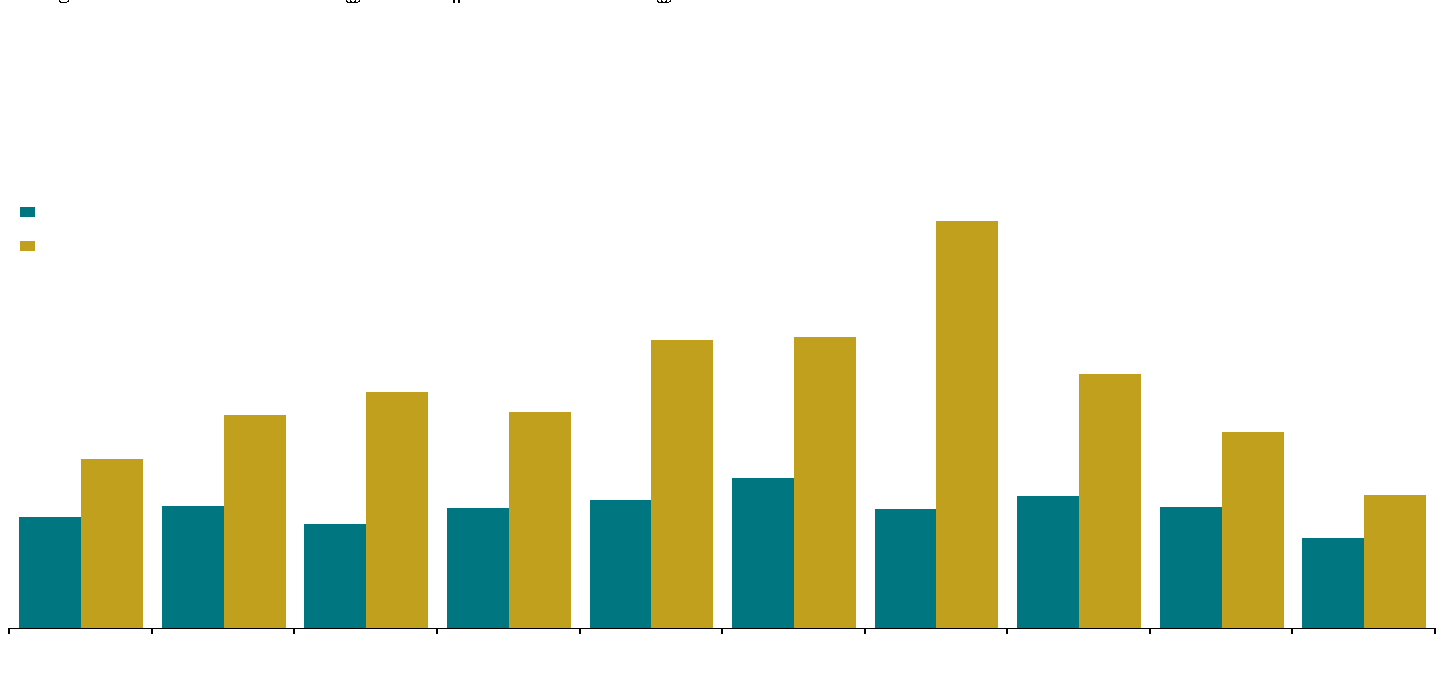

Rule 10b-5 Claims and “Simplified Tiered Damages”

“Simplified tiered damages” uses simplifying assumptions to estimate per-share damages and trading behavior for cases involving Rule 10b-5 claims. It provides a measure of potential shareholder losses that allows for consistency across a large volume of cases, thus enabling the identification and analysis of potential trends. 6

Cornerstone Research’s analysis finds this measure to be the most important factor in estimating settlement amounts. 7 However, this measure is not intended to represent actual economic losses borne by shareholders. Determining any such losses for a given case requires more in-depth economic analysis.

-

Similar to settlement amounts, the median “simplified tiered damages” in 2022 increased 125% compared to 2021 and was over 100% higher than the median of settled cases for the prior nine years.

-

In 2022, nearly half of settlements with Rule 10b-5 claims involved “simplified tiered damages” over $500 million, an all-time high.

-

Higher “simplified tiered damages” are typically associated with larger issuer defendants. Consistent with this, the median total assets of issuer defendants in 2022 settled cases was 97% higher than the median total assets for 2021 settled cases.

-

Higher “simplified tiered damages” are also generally associated with larger disclosure dollar losses. In 2022, the median DDL grew by more than 160% compared to 2021, reaching an all-time high.

Median “simplified tiered damages” reached an all-time high in 2022.

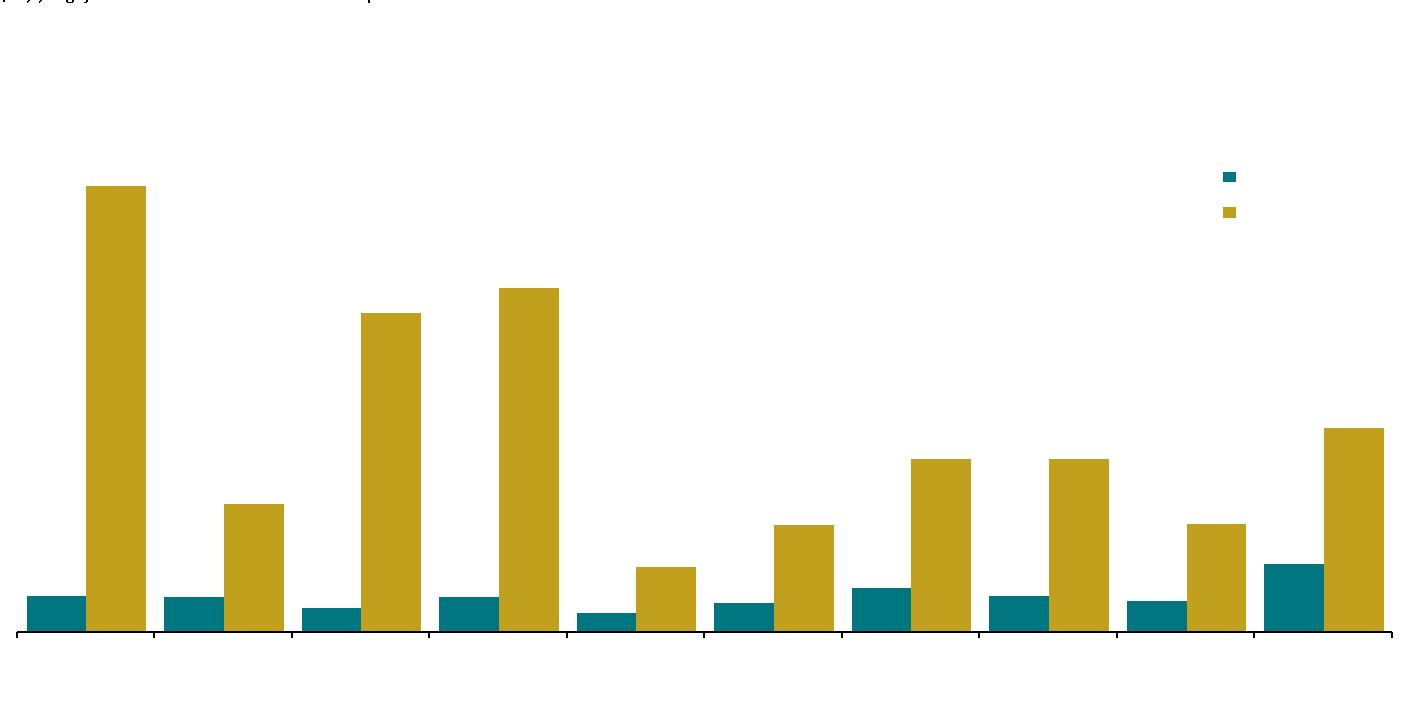

Figure 4 : Median and Average “Simplified Tiered Damages” in Rule 10b-5 Cases

2013–2022

(Dollars in millions)

Note: “Simplified tiered damages” are adjusted for inflation based on class period end dates for common stock only; 2022 dollar equivalent figures are presented. Damages are estimated for cases alleging a claim under Rule 10b-5 (whether alone or in addition to other claims).

-

Only 4% of settlements in 2022 had “simplified tiered damages” less than $25 million, the lowest observed to date.

-

Cases with smaller “simplified tiered damages” are more likely to be associated with issuers that had been delisted from a major exchange and/or declared bankruptcy prior to settlement. In 2022, the percentage of such issuers for settled cases was at an all-time low (11%).

-

The 2022 median and average settlement as a percentage of “simplified tiered damages” of 3.6% and 5.4%, respectively, are all-time lows. (See Appendix 5 for additional information on median and average settlements as a percentage of “simplified tiered damages.”)

'33 Act Claims and “Simplified Statutory Damages”

For Securities Act of 1933 (’33 Act) claim cases—those involving only Section 11 and/or Section 12(a)(2) claims—potential shareholder losses are estimated using a model in which the statutory loss is the difference between the statutory purchase price and the statutory sales price, referred to here as “simplified statutory damages.” Only the offered shares are assumed to be eligible for damages. 8

-

In 2022, there were nine settlements for cases with only ’33 Act claims, in line with the average from 2017 to 2020 and well below the historically high number of 16 settlements observed in 2021.

-

The median settlement as a percentage of simplified statutory damages in 2022 and 2021 were 4.7% and 4.4%, respectively—the lowest levels since 2002. (See Appendix 6 for additional information on median and average settlements as a percentage of “simplified statutory damages.”)

-

The average settlement amount for cases with only ’33 Act claims was $7.3 million in 2022, compared to $14.9 million during 2013-2021.

In 2022, the median settlement amount for cases with only ’33 Act claims was $7.0 million, the lowest since 2013.

Figure 6 : Settlements by Nature of Claims

2013–2022

(Dollars in millions)

|

Number of Settlements |

Median Settlement |

Median “Simplified Statutory Damages” |

Median Settlement as a Percentage of “Simplified Statutory |

|

|

Section 11 and/or |

82 |

$9.2 |

$145.2 |

8.7% |

|

Number of Settlements |

Median Settlement |

Median “Simplified Tiered Damages” |

Median Settlement as a Percentage of “Simplified Tiered |

|

|

Both Rule 10b-5 and |

123 |

$15.4 |

$355.7 |

6.3% |

|

Rule 10b-5 Only |

581 |

$9.0 |

$250.1 |

4.5% |

Note: Settlement dollars and damages are adjusted for inflation; 2022 dollar equivalent figures are presented.

-

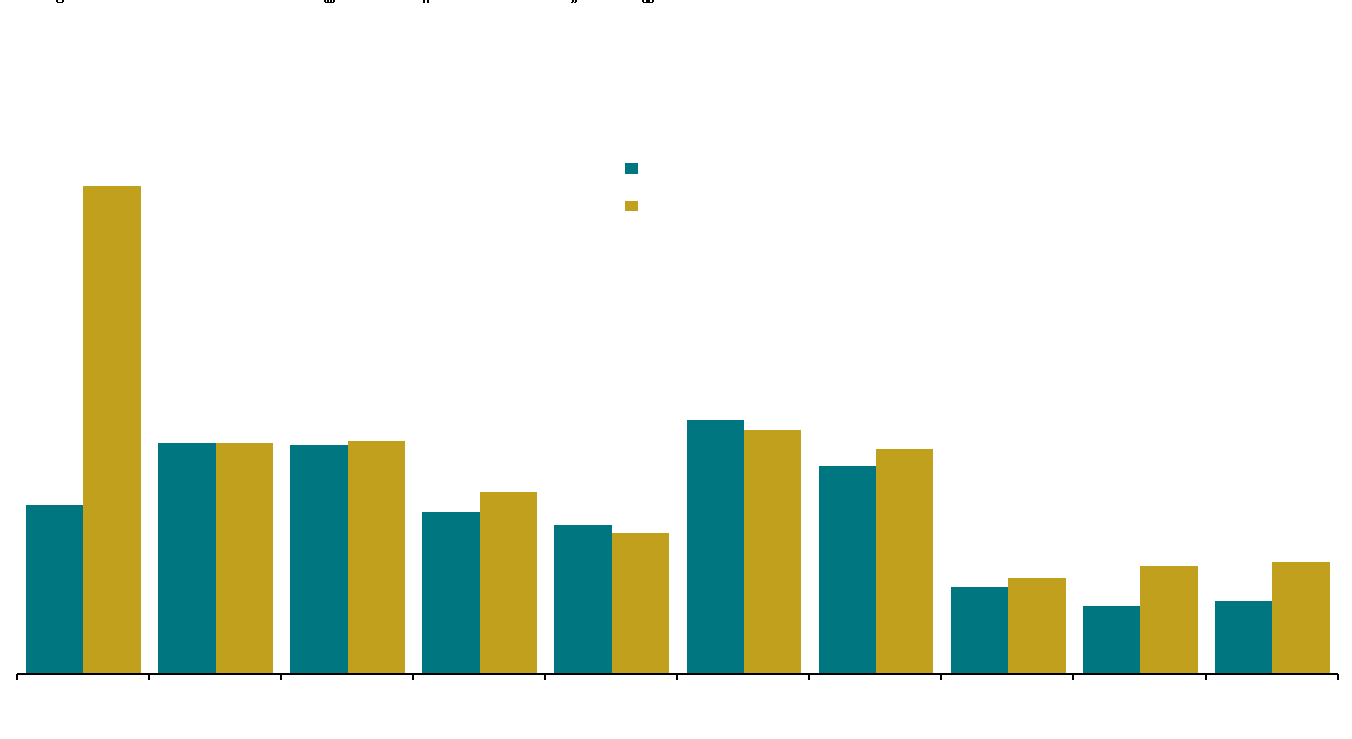

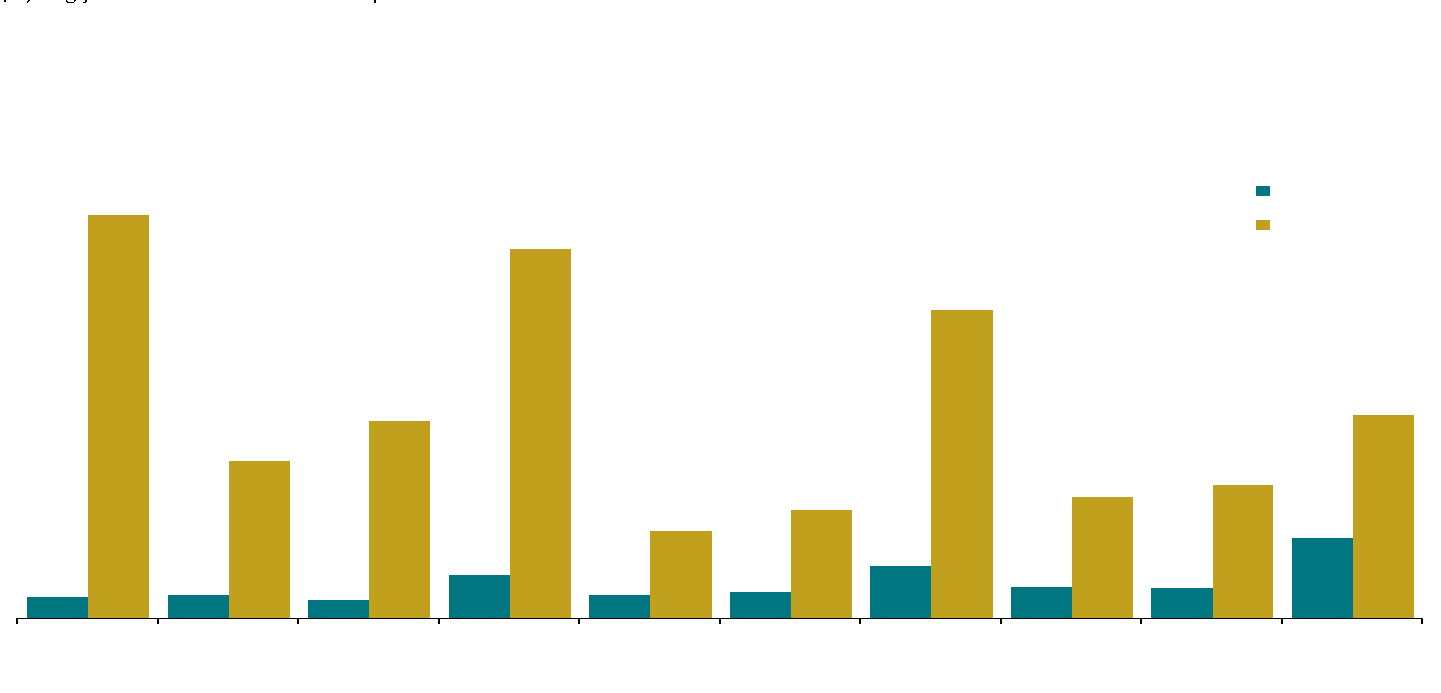

Settlements as a percentage of the simplified proxies for potential shareholder losses used in this report are typically smaller for cases that have larger estimated damages. As with cases with Rule 10b-5 claims, this finding holds for cases with only ’33 Act claims.

-

In the past decade, over 85% of the settled '33 Act claim cases involved an underwriter (or underwriters) as a named codefendant.

-

Over 80% of ‘33 Act claim cases that settled in 2013–2022 involved an initial public offering (IPO).

Consistent with the lower median settlement amount among ’33 Act claim cases, the median “simplified statutory damages” in 2022 declined by 61% from the median in 2021 and was the lowest since 2016.

Figure 7 : Median Settlement as a Percentage of “Simplified Statutory Damages” by Damages Ranges in ’33 Act Claim Cases

2013–2022

(Dollars in millions)

Jurisdictions of Settlements of ’33 Act Claim Cases

|

|

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|

State Court |

1 |

0 |

2 |

4 |

5 |

4 |

4 |

7 |

6 |

6 |

|

Federal Court |

7 |

2 |

2 |

6 |

3 |

4 |

5 |

1 |

10 |

3 |

Note: “N” refers to the number of cases. This analysis excludes cases alleging Rule 10b-5 claims..

Analysis of Settlement Characteristics

GAAP Violations

This analysis examines allegations of GAAP violations in settlements of securities class actions involving Rule 10b-5 claims, including two sub-categories of GAAP violations—financial statement restatements and accounting irregularities. 9 For further details regarding settlements of accounting cases, see Cornerstone Research’s annual report on Accounting Class Action Filings and Settlements. 10

-

For the first time since 2017, the median settlement amount for cases involving GAAP allegations was larger than that for non-GAAP cases. Notably, in 2022 the median settlement amount for GAAP cases was more than double that of non-GAAP cases.

-

As noted in prior years, settlements as a percentage of “simplified tiered damages” for cases involving GAAP allegations are typically higher than for non-GAAP cases. This result has continued despite a relatively low number of cases involving a financial restatement. For example, only 11% of settlements in 2022 involved a restatement of financial statements.

-

Auditor codefendants were involved in only 3% of settled cases, consistent with 2021 but substantially lower than the average from 2013 to 2021.

-

The infrequency of cases alleging accounting irregularities continued in 2022 at less than 2% of settled cases.

The proportion of settled cases in 2022 with Rule 10b-5 claims alleging GAAP violations remained at a historically low level.

Figure 8 : Median Settlement as a Percentage of “Simplified Tiered Damages” and Allegations of GAAP Violations

2013–2022

Note: “N” refers to the number of cases. This analysis is limited to cases alleging Rule 10b-5 claims (whether alone or in addition to other claims).

Derivative Actions

-

Securities class actions often involve accompanying (or parallel) derivative actions with similar claims, and such cases have historically settled for higher amounts than securities class actions without corresponding derivative matters. 11

-

In 2022, the median settlement amount for cases with an accompanying derivative action was approximately 28% higher than for cases without ($14.1 million versus $11.0 million, respectively).

-

For cases settled during 2018–2022, 38% of parallel derivative suits were filed in Delaware. California and New York were the next most common venues for such actions, representing 22% and 15% of such settlements, respectively.

Although the proportion of cases involving accompanying derivative actions in 2022 was higher compared to 2021, it was below the average for 2018–2021.

-

It is commonly understood that most parallel derivative suits do not settle for monetary amounts (other than plaintiffs’ attorney fees). However, the likelihood of a monetary settlement among parallel derivative actions is higher when the securities class action settlement is large, as shown in Cornerstone Research’s Parallel Derivative Action Settlement Outcomes . 12

Figure 9: Frequency of Derivative Actions

2013–2022

Corresponding SEC Actions

-

Historically, cases with an accompanying SEC action have typically been associated with substantially higher settlement amounts. 13 However, this pattern did not hold in 2022.

-

The median settlement amount in 2022 for cases that involved a corresponding SEC action was less than 5% higher than the median for cases without such an action. In contrast, in 2021, the median settlement amount for cases with an accompanying SEC action was more than double that for cases without such an action.

Settled cases involving SEC actions in 2022 were considerably smaller than cases without accompanying SEC actions.

-

Both “simplified tiered damages” and DDL were lower in 2022 for cases with a corresponding SEC action when compared to those without, at 72% and 83% lower, respectively.

-

Settled cases in 2022 with a corresponding SEC action were nearly 10% quicker to reach settlement, on average, compared to cases without such an action. In contrast, in 2021, cases with corresponding SEC actions took over 20% longer to reach a settlement than cases without corresponding SEC actions.

-

The number of settled cases in 2022 involving either a corresponding SEC action or criminal charge remained below 13%, compared to an average of 24% for the years 2013–2021.

Figure 10: Frequency of SEC Actions

2013–2022

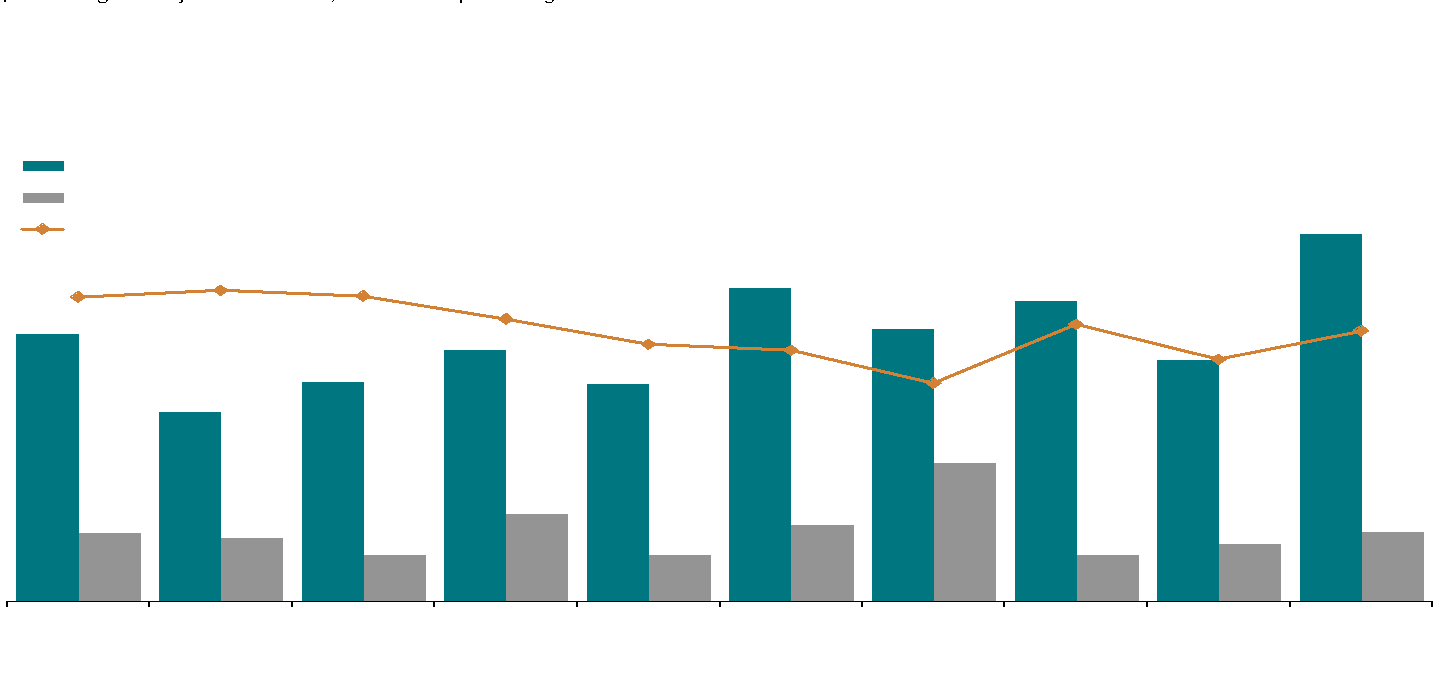

Institutional Investors

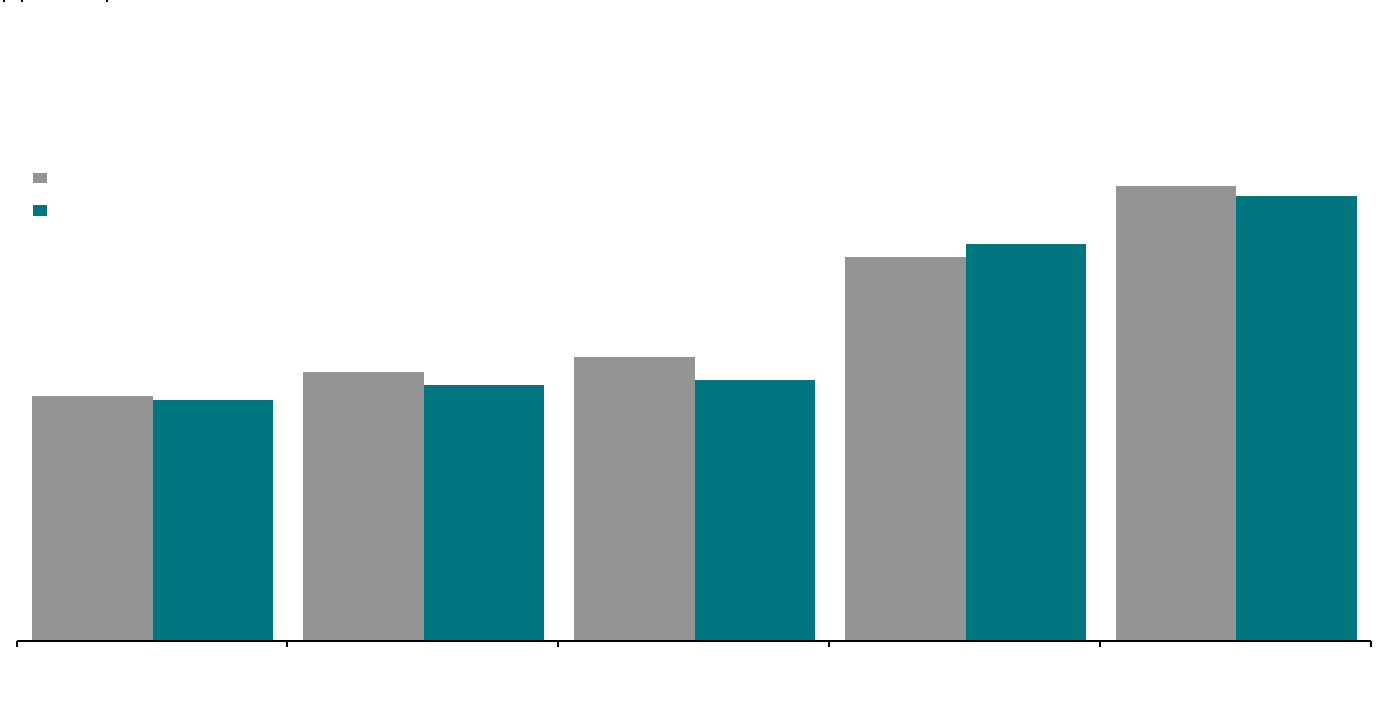

As discussed in prior reports, increasing institutional participation as lead plaintiffs in securities litigation was a focus of the Reform Act. 14 Indeed, in years following passage of the Reform Act, institutional investor involvement as lead plaintiffs did increase, particularly in larger cases, that is, cases with higher “simplified tiered damages.”

-

In 2022, for cases involving an institutional investor as lead plaintiff, median “simplified tiered damages” and median total assets were five times and eight times higher, respectively, than the median values for cases without an institutional investor as a lead plaintiff.

-

Since passage of the Reform Act, public pension plans have been the most frequent type of institutional lead plaintiff.

Of the eight mega settlement cases in 2022, seven included an institutional lead plaintiff.

-

In 2022, a public pension plan served as lead plaintiff in two-thirds of cases with an institutional lead plaintiff. Moreover, in six of the seven mega settlement cases in 2022 involving an institutional lead plaintiff, the institutional investor was a public pension plan.

-

Institutional participation as lead plaintiff continues to be associated with particular plaintiff counsel. For example, an institutional investor served as a lead plaintiff in 2022 in over 85% of settled cases in which Robbins Geller Rudman & Dowd LLP and/or Bernstein Litowitz Berger & Grossmann LLP served as lead plaintiff counsel. In contrast, institutional investors served as lead plaintiffs in 21% of cases in which The Rosen Law Firm, Pomerantz LLP, or Glancy Prongay & Murray LLP served as lead plaintiff counsel.

Figure 11: Median Settlement Amounts and Institutional Investors

2013–2022

(Dollars in millions)

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented.

Time to Settlement and Case Complexity

-

Overall, the median time from filing to settlement hearing date in 2022 was longer—3.2 years for 2022 settlements, compared to 2.9 years for 2013–2021 settlements.

-

Cases involving an institutional lead plaintiff continued to take longer to settle. In particular, settlements in 2022 with institutional lead plaintiffs took 33% longer to settle than cases not involving an institutional lead plaintiff.

Only 42% of cases in 2022 reached a settlement hearing date within three years of filing, the lowest percentage in the prior nine years.

-

Larger cases (as measured by higher “simplified tiered damages”) often take longer to resolve. Consistent with this, in 2022, the median time to settlement for cases that settled for at least $100 million was over 5.5 years—an all-time high for such cases.

Figure 12: Median Settlement by Duration from Filing Date to Settlement Hearing Date

2013–2022

(Dollars in millions)

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented. “N” refers to the number of cases.

Case Stage at the Time of Settlement

In collaboration with Stanford Securities Litigation Analytics (SSLA), 15 this report analyzes settlements in relation to the stage in the litigation process at the time of settlement.

-

Cases settling at later stages continue to be larger in terms of total assets and “simplified tiered damages.”

-

In particular, the median issuer defendant total assets for 2022 cases that settled after the ruling on a motion for class certification was over four times the median for cases that settled prior to such a motion being ruled on.

-

In 2022, cases where a motion for class certification was filed were nearly three times as likely to have either Robbins Geller Rudman & Dowd LLP and/or Bernstein Litowitz Berger & Grossmann LLP as lead plaintiff counsel than The Rosen Law Firm, Pomerantz LLP, or Glancy Prongay & Murray LLP.

-

Cases settling at later stages often included an institutional investor lead plaintiff. For example, in 2022, an institutional investor served as lead plaintiff 69% of the time for cases that settled after the filing of a motion for class certification (slightly higher than the percentage over the prior four years), compared to 44% for cases that settled prior to the filing of a motion for class certification (38% in the prior four years)

-

Overall, compared to settlements in 2021, a larger proportion of cases in 2022 did not reach settlement until after a motion for class certification was filed. In addition, 14% of 2022 settled cases were resolved after a summary judgment motion, compared to less than 9% for 2018–2021 settlements.

Figure 13: Median Settlement Dollars and Resolution Stage at Time of Settlement

2018–2022

(Dollars in millions)

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented. “N” refers to the number of cases. MTD refers to “motion to dismiss,” CC refers to “class certification,” and MSJ refers to “motion for summary judgment.” This analysis is limited to cases alleging Rule 10b-5 claims (whether alone or in addition to other claims).

Cornerstone Research’s Settlement Analysis

This research applies regression analysis to examine the relations between settlement outcomes and certain securities case characteristics. Regression analysis is employed to better understand the factors that are important for estimating what cases might settle for, given the characteristics of a particular securities class action.

Determinants of Settlement Outcomes

Based on the research sample of cases that settled from January 2006 through December 2022, important determinants of settlement amounts include the following:

-

“Simplified tiered damages”

-

Maximum Dollar Loss (MDL)—the dollar-value change in the defendant firm’s market capitalization from its class period peak to the trading day immediately following the end of the class period.

-

Most recently reported total assets of the issuer defendant firm

-

Number of entries on the lead case docket

-

Whether there were accounting allegations

-

Whether there was a corresponding SEC action against the issuer, other defendants, or related parties

-

Whether there were criminal charges against the issuer, other defendants, or related parties with similar allegations to those included in the underlying class action complaint

-

Whether there was an accompanying derivative action

-

Whether Section 11 and/or Section 12(a) claims were alleged in addition to Rule 10b-5 claims

-

Whether the issuer defendant was distressed

-

Whether an institution was a lead plaintiff

-

Whether securities other than common stock/ADR/ADS, were included in the alleged class

Cornerstone Research analyses show that settlements were higher when “simplified tiered damages,” MDL, issuer defendant asset size, or the number of docket entries was larger, or when Section 11 and/or Section 12(a) claims were alleged in addition to Rule 10b-5 claims.

Settlements were also higher in cases involving accounting allegations, a corresponding SEC action, criminal charges, an accompanying derivative action, an institution involved as lead plaintiff, or securities in addition to common stock included in the alleged class.

Settlements were lower if the issuer was distressed.

More than 75% of the variation in settlement amounts can be explained by the factors discussed above.

Research Sample

-

The database compiled for this report is limited to cases alleging Rule 10b-5, Section 11, and/or Section 12(a)(2) claims brought by purchasers of a corporation’s common stock. The sample contains only cases alleging fraudulent inflation in the price of a corporation’s common stock.

-

Cases with alleged classes of only bondholders, preferred stockholders, etc., cases alleging fraudulent depression in price, and mergers and acquisitions cases are excluded. These criteria are imposed to ensure data availability and to provide a relatively homogeneous set of cases in terms of the nature of the allegations.

-

The current sample includes 2,116 securities class actions filed after passage of the Reform Act (1995) and settled from 1996 through 2022. These settlements are identified based on a review of case activity collected by Securities Class Action Services LLC (SCAS). 16

-

The designated settlement year, for purposes of this report, corresponds to the year in which the hearing to approve the settlement was held. 17 Cases involving multiple settlements are reflected in the year of the most recent partial settlement, provided certain conditions are met. 18

Data Sources

In addition to SCAS, data sources include Dow Jones Factiva, Bloomberg, the Center for Research in Security Prices (CRSP) at University of Chicago Booth School of Business, Standard & Poor’s Compustat, Refinitiv Eikon, court filings and dockets, SEC registrant filings, SEC litigation releases and administrative proceedings, LexisNexis, Stanford Securities Litigation Analytics (SSLA), Securities Class Action Clearinghouse (SCAC), and public press.

Endnotes

Appendices

Appendix 1: Settlement Percentiles

(Dollars in millions)

|

Year |

Average |

10th |

25th |

Median |

75th |

90th |

|

2013 |

$90.8 |

$2.4 |

$3.8 |

$8.2 |

$27.9 |

$103.6 |

|

2014 |

$22.5 |

$2.1 |

$3.5 |

$7.4 |

$16.3 |

$61.8 |

|

2015 |

$48.6 |

$1.6 |

$2.7 |

$8.0 |

$20.1 |

$116.1 |

|

2016 |

$86.1 |

$2.3 |

$5.1 |

$10.4 |

$40.2 |

$178.0 |

|

2017 |

$22.0 |

$1.8 |

$3.1 |

$6.3 |

$18.2 |

$42.3 |

|

2018 |

$75.6 |

$1.8 |

$4.2 |

$13.1 |

$28.8 |

$57.3 |

|

2019 |

$32.3 |

$1.7 |

$6.4 |

$12.6 |

$22.9 |

$57.2 |

|

2020 |

$62.3 |

$1.6 |

$3.6 |

$11.1 |

$22.9 |

$60.3 |

|

2021 |

$22.2 |

$1.9 |

$3.4 |

$8.9 |

$19.3 |

$63.3 |

|

2022 |

$36.2 |

$2.0 |

$5.0 |

$13.0 |

$33.0 |

$71.8 |

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented.

Appendix 2: Settlements by Select Industry Sectors

2013–2022

(Dollars in millions)

|

Industry |

Number of |

Median |

Median |

Median Settlement |

|

Financial |

92 |

$14.8 |

$293.3 |

5.0% |

|

Healthcare |

20 |

$14.2 |

$189.4 |

6.4% |

|

Pharmaceuticals |

119 |

$7.6 |

$237.6 |

3.8% |

|

Retail |

50 |

$13.2 |

$294.2 |

4.8% |

|

Technology |

103 |

$9.3 |

$315.9 |

4.6% |

|

Telecommunication |

26 |

$10.5 |

$311.0 |

4.4% |

Note: Settlement dollars and “simplified tiered damages” are adjusted for inflation; 2022 dollar equivalent figures are presented. “Simplified tiered damages” are calculated only for cases involving Rule 10b-5 claims (whether alone or in addition to other claims).

Appendix 3: Settlements by Federal Circuit Court

2013–2022

(Dollars in millions)

|

Circuit |

Number of Settlements |

Median Settlement |

Median Settlement as a Percentage of |

|

First |

21 |

$12.4 |

3.0% |

|

Second |

202 |

$9.0 |

5.0% |

|

Third |

81 |

$7.5 |

4.9% |

|

Fourth |

26 |

$22.9 |

3.8% |

|

Fifth |

38 |

$10.7 |

4.9% |

|

Sixth |

32 |

$13.5 |

7.4% |

|

Seventh |

37 |

$15.5 |

3.6% |

|

Eighth |

14 |

$46.4 |

5.1% |

|

Ninth |

191 |

$7.6 |

4.6% |

|

Tenth |

17 |

$10.2 |

5.8% |

|

Eleventh |

37 |

$11.9 |

4.9% |

|

DC |

5 |

$33.7 |

2.4% |

Note: Settlement dollars are adjusted for inflation; 2022 dollar equivalent figures are presented. Settlements as a percentage of “simplified tiered damages” are calculated only for cases alleging Rule 10b-5 claims (whether alone or in addition to other claims).

Appendix 4: Mega Settlements

2013–2022

Note: Mega settlements are defined as total settlement funds equal to or greater than $100 million.

Appendix 5: Median and Average Settlements as a Percentage of “Simplified Tiered Damages”

2013–2022

Note: “Simplified tiered damages” are calculated only for cases alleging Rule 10b-5 claims (whether alone or in addition to other claims).

Appendix 6: Median and Average Settlements as a Percentage of “Simplified Statutory Damages”

2013–2022

Note: “Simplified statutory damages” are calculated only for cases alleging Section 11 (’33 Act) claims and no Rule 10b-5 claims.

Appendix 7: Median and Average Maximum Dollar Loss (MDL)

2013–2022

(Dollars in millions)

Note: MDL is adjusted for inflation based on class period end dates; 2022 dollar equivalents are presented. MDL is the dollar value change in the defendant firm’s market capitalization from the trading day with the highest market capitalization during the class period to the trading day immediately following the end of the class period. This analysis excludes cases alleging ’33 Act claims only.\

Appendix 8: Median and Average Disclosure Dollar Loss (DDL)

2013–2022

(Dollars in millions)

Note: DDL is adjusted for inflation based on class period end dates; 2022 dollar equivalents are presented. DDL is the dollar-value change in

the defendant firm’s market capitalization between the end of the class period and the trading day immediately following the end of the class

period. This analysis excludes cases alleging ’33 Act claims only.

Appendix 9: Median Docket Entries by “Simplified Tiered Damages” Range

2013–2022

(Dollars in millions)

Note: “Simplified tiered damages” are calculated only for cases alleging Rule 10b-5 claims (whether alone or in addition to other claims).

FOOTNOTES

1 Reported dollar figures and corresponding comparisons are adjusted for inflation; 2022 dollar equivalent figures are analyzed.

2 ”Simplified tiered damages” are calculated for cases that settled in 2006 or later, following the U.S. Supreme Court’s 2005 landmark decision in Dura Pharmaceuticals Inc. v. Broudo, 544 U.S. 336. “Simplified tiered damages” is based on the stock-price drops on alleged corrective disclosure dates as described in the settlement plan of allocation.

3 Disclosure Dollar Loss or DDL is the dollar-value change in the defendant firm’s market capitalization between the end of the class period and the trading day immediately following the end of the class period.

4 Accounting irregularities reflect those cases in which the defendant has reported the occurrence of accounting irregularities (intentional misstatements or omissions) in its financial statements.

5 Securities Class Action Filings—2022 Year in Review, Cornerstone Research (2023).

6 The “simplified tiered damages” approach used for purposes of this settlement research does not examine the mix of information associated with the specific dates listed in the plan of allocation, but simply applies the stock price movements on those dates to an estimate of the “true value” of the stock during the alleged class period (or “value line”). This proxy for damages utilizes an estimate of the number of shares damaged based on reported trading volume and the number of shares outstanding. Specifically, reported trading volume is adjusted using volume reduction assumptions based on the exchange on which the issuer defendant’s common stock is listed. No adjustments are made to the underlying float for institutional holdings, insider trades, or short-selling activity during the alleged class period. Because of these and other simplifying assumptions, the damages measures used in settlement outcome modeling may differ substantially from damages estimates developed in conjunction with case-specific economic analysis.

7 Laarni T. Bulan, Ellen M. Ryan, and Laura E. Simmons, Estimating Damages in Settlement Outcome Modeling, Cornerstone Research (2017).

8 The statutory purchase price is the lesser of the security offering price or the security purchase price. Prior to the first complaint filing date, the statutory sales price is the price at which the security was sold. After the first complaint filing date, the statutory sales price is the greater of the security sales price or the security price on the first complaint filing date. Similar to “simplified tiered damages,” the estimation of “simplified statutory damages” makes no adjustments to the underlying float for institutional holdings, insider trades, or short-selling activity.

9 The two sub-categories of accounting issues analyzed in Figure 8 of this report are (1) restatements—cases involving a restatement (or announcement of a restatement) of financial statements; and (2) accounting irregularities.

10 Accounting Class Action Filings and Settlements—2022 Review and Analysis, Cornerstone Research (2023), forthcoming in spring 2023.

11 To be considered an accompanying or parallel derivative action, the derivative action must have underlying allegations that are similar or related to the underlying allegations of the securities class action and either be active or settling at the same time as the securities class action.

12 Parallel Derivative Action Settlement Outcomes, Cornerstone Research (2022).

13 As noted previously, it could be that the merits in such cases are stronger, or simply that the presence of a corresponding SEC action provides plaintiffs with increased leverage when negotiating a settlement. For purposes of this research, an SEC action is evidenced by the presence of a litigation release or an administrative proceeding posted on www.sec.gov involving the issuer defendant or other named defendants with allegations similar to those in the underlying class action complaint.

14 See, for example, Securities Class Action Settlements—2006 Review and Analysis, Cornerstone Research (2007) and Michael A. Perino, “Have Institutional Fiduciaries Improved Securities Class Actions? A Review of the Empirical Literature on the PSLRA’s Lead Plaintiff Provision,” St. John’s Legal Studies Research Paper No. 12-0021 (2013).

15 Stanford Securities Litigation Analytics (SSLA) tracks and collects data on private shareholder securities litigation and public enforcements brought by the SEC and the U.S. Department of Justice. The SSLA dataset includes all traditional class actions, SEC actions, and DOJ criminal actions filed since 2000. Available on a subscription basis at https://sla.law.stanford.edu/.

16 Available on a subscription basis. For further details see https://www.issgovernance.com/securities-class-action-services/.

17 Movements of partial settlements between years can cause differences in amounts reported for prior years from those presented in earlier reports.

18 This categorization is based on the timing of the settlement hearing date. If a new partial settlement equals or exceeds 50% of the then-current settlement fund amount, the entirety of the settlement amount is re-categorized to reflect the settlement hearing date of the most recent partial settlement. If a subsequent partial settlement is less than 50% of the then-current total, the partial settlement is added to the total settlement amount and the settlement hearing date is left unchanged.