/>i

/>iThe challenges facing traditional banks over the last 12 months have proved to be golden opportunities for private lending.

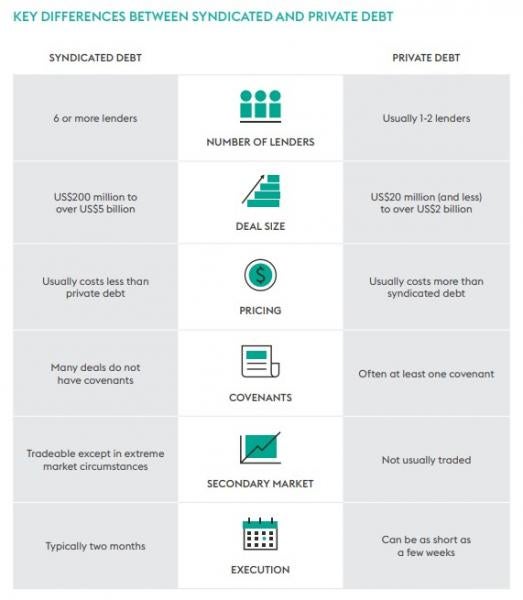

The words “sophisticated capital”, “alternative capital”, and “private credit” once carried at least a hint of differing meanings. Those words would now, however, appear to have converged to reference non-bank (in its traditional sense) lending being extended directly to a borrowing business unit e.g., debt issued by private equity firms, specialty finance firms, hedge funds, and the like.

These loans once had a limited range of uses or were linked to areas of financial distress owing to their higher pricing, but now they dominate the private equity markets and across (among other areas), capital investment and leveraged buy-outs, plus they have increased relevance in the corporate space. Private credit has gone from supplementing the traditional commercial lending industry to taking market share and, in some cases, even supplanting those traditional lending houses.

Today is arguably a golden era for this asset class, as the traditional banks, battered by the financial crisis and subsequent increased regulation, have progressively shied away from certain types of risk and been forced to operate without the flexibility over terms and capital structuring offered by private credit. Contrastingly, private credit managers have become more sophisticated, as they are able to participate in a wide variety of complex structures and less traditional business types, offering flexibility on terms, and greater speed of execution and pricing.

The opportunities are now attractive, perhaps even compelling, for businesses and private equity houses. A number of private equity players are now establishing successful private credit businesses, not just affording investors a further avenue of return, but also potentially creating an independent yet friendly anchor investor for future business.

During the first quarter of 2020, as a few infections progressed into a fully-fledged worldwide pandemic, certain sectors faced significant challenges. Some of those sectors were under considerable stress even before the pandemic; retail, for example, was already struggling to adapt to the changing spending habits of consumers. In the second and third quarters of 2020, banks found themselves inundated with the trifecta of government-guaranteed paper, inconsistent regulatory messaging, and significant pressure to fund revolvers, not to mention the portfolio pressure that always arises in uncertain times.

As traditional lending worked through these challenges, the private credit markets were white-hot, quickly reacting to their portfolio but also looking forward with vast available liquidity. The increasing ability of credit funds to execute on larger and more complex deals without market or syndication risk saw increased large-cap activity for private credit.

Private credit offers increased confidentiality and greater certainty with a faster turnround time.

Private credit worked proactively with existing clients to navigate the turbulence, even underscoring the strength and value of relationships and partnerships with their clients. An industry previously feared for behaving like vulture capital was showing patience and polishing its reputation. This emboldened the confidence of private equity and corporate borrowers alike. It wasn’t just the size or execution capability that was impressing everyone, it was the true nature of patient capital, which became plain to see, and the flexibility, willingness, and creativity in structuring that provided borrowers with real solutions whether through regular performing credit, stretched leverage flexibility or “specialty” lending.

More and more, private equity firms looking to finance big leveraged buyouts are using traditional lenders less and less. Recent examples of larger deals coming through the market from private credit include the US$2.6 billion stamps.com transaction or the US$2.3 billion loan for the buyout of Calypso Technology Inc. Only a few years ago, these loans rarely exceeded US$500 million and we may now see more top tier sponsor transactions for top credits “clubbing” together a number of private lenders to provide jumbo financings.

From an investment perspective, private credit provides a strong opportunity.

Despite low-interest rates making secured lending cheap, traditional financing still remains a popular avenue for financing buy-outs; for the right credit, with the right leverage, banks may still represent the cheaper option. Nonetheless, the loans and bonds that banks are underwriting are typically sold on to a wide group of lenders as collateralized loan obligations, or to other institutions, and are therefore priced according to that market. Any shift in investor sentiment or socio-economic jitters can alter the certainty of execution or even the financing terms of a deal. Pricing can be impacted at both ends, either making debt expensive or making debt cheap enough to allow even distressed investors to buy in. Neither is attractive to private equity. In addition, private credit offers increased confidentiality and greater certainty with a faster turnaround time to securing funding. Whilst there may be an incremental cost to private credit, buy-out firms are willing to pay for certainty, speed, flexibility, and their growing relationship.