/>i

/>iAhead of the new Failure to Prevent Fraud Offence[1] (“FTPFO”) coming into force on Monday 1 September 2025, the Serious Fraud Office (“SFO”) and the Crown Prosecution Service (“CPS”) have updated their Joint Prosecution Corporate Guidance (“Joint Guidance”). The Joint Guidance serves as a timely reminder to organisations that their grace period to implement, review, and improve their fraud prevention frameworks is coming to an end.

Following the Joint Guidance, the announcements from the prosecution authorities [2] suggest they are taking Failure to Prevent Fraud (“FTPF”) enforcement very seriously. Nick Ephgrave, the Director of the SFO, has stated that “now is the time to take action. Corporations must get their house in order or be ready to face investigation.”

Reflecting a similar urgency, Hannah von Dadelszen, Chief Crown Prosecutor at the CPS explained:

“Preventing fraud is essential to protecting the public and our economy. The public are entitled to have confidence that companies will be held to account for wrongdoing…. Large companies, charities and other organisations need to act now to make sure they have proper fraud prevention systems in place.”

Therefore, taking a relaxed approach and failing to act now may be a risky strategy for preventing fraud. In particular:

- The “base” offences [3] that may result in an organisation being prosecuted for FTPF are wide ranging, covering a multitude of dishonest conduct, including fraud by false representation, fraud by abuse of position, false accounting and false statements by company directors. Liability can also arise from assisting or encouraging these offences;

- Fraud offences are subject to more frequent and rigorous prosecution than tax evasion offences (which are often subject to civil settlement);

- The FTPFO’s focus on fraud committed with the intention of benefitting the organisation that can be held liable means that existing fraud prevention controls (which often seek to prevent fraud being perpetrated on the company) may not constitute reasonable fraud prevention procedures for the purpose of the FTPFO; and

- The Economic Crime and Corporate Transparency Act 2023 (“ECCTA”) amends the Criminal Justice Act 1987,[4] enabling the SFO to use its investigative powers to compel individuals and companies to provide information in cases of suspected fraud at the pre-investigation stage.

Organisations investigated or prosecuted for FTPFO face significant legal, financial, and reputational jeopardy. Organisations can defend themselves by showing that reasonable fraud prevention procedures were in place. Accordingly, organisations should:

- Determine if they are within the scope of the FTPFO, either individually or as part of a group.[5]

- Conduct a risk assessment and gap analysis to understand the risks they face from fraud being committed by an Associated Person with the intention of benefiting the organisation or their clients; and

- Implement reasonable fraud prevention procedures to mitigate the risk of investigation and prosecution under the FTPFO.

Outlined below are important factors identified in the Joint Guidance that organisations should carefully consider when preparing to comply with the FTPFO regime:

Associated Persons

As set out in our earlier client alert on the FTPFO, a large organisation can be held liable for FTPF if a fraud offence is committed by an “Associated Person” for, or on behalf of, the organisation with the intention of benefiting the organisation or its clients.

The Joint Guidance reiterates that an Associated Person is someone who “performs services for or on behalf of a relevant organisation within the scope of the relevant offence” (the “Associated Person Test”). This may include directors, employees, agents, subsidiaries, intermediaries, contractors or consultants.[6]

The Joint Guidance explains that the Associated Person Test is “purposive rather than formal,”[7] meaning that prosecutors will focus on whether the individual was acting in the capacity of performing services for or on behalf of the organisation, regardless of their contractual status or title. They will examine the individual’s relationship to the organisation and the true nature of their role.

If organisations fail to map, assess, and monitor all such relationships proactively, they risk being held responsible for misconduct they neither authorised nor were aware of.

UK Nexus

For an organisation to be prosecuted for FTPFO, there must be a UK nexus. The Economic Crime and Corporate Transparency Act 2023: Guidance to organisations on the offence of failure to prevent fraud (the “FTPF Guidance”) sets out the following examples of a UK nexus:

- One of the acts which was part of the underlying fraud must have taken place in the UK, or the gain or loss occurred in the UK.

- If a UK-based employee commits fraud, the employing organisation could be prosecuted, wherever it is based.

- If an employee or associated person of an overseas-based organisation commits fraud in the UK, or targets victims in the UK, the organisation could be prosecuted.[8]

The Joint Guidance stipulates that prosecutors are encouraged to engage in early coordination with relevant agencies or jurisdictions in situations where cases contain international elements.[9]

Therefore, organisations must know exactly where they and their Associated Persons are conducting business. By plotting out operations and conducting thorough due diligence, organisations will be able to assess their compliance risk in each jurisdiction. In an increasingly global environment, clear oversight will be key to helping organisations mitigate risk and respond to cross-border issues.

Bribery v Fraud

The Joint Guidance stipulates that in some cases there will be a close factual nexus between bribery and fraud offences. For example, an organisation may make improper payments to obtain or retain business (bribery), and, at the same time, it may engage in false accounting, make misrepresentations, or conceal information to deceive another party (fraud).

Prosecutors are encouraged to consider carefully whether the facts support a charge under the FTPFO in a situation where it is not possible to proceed under section 7 of the UK Bribery Act 2010.[10] The Joint Guidance encourages a well-thought-out prosecution strategy and makes clear to organisations that prosecutors should ensure that serious misconduct is addressed, even if it is not possible to use the charge that was intended initially.

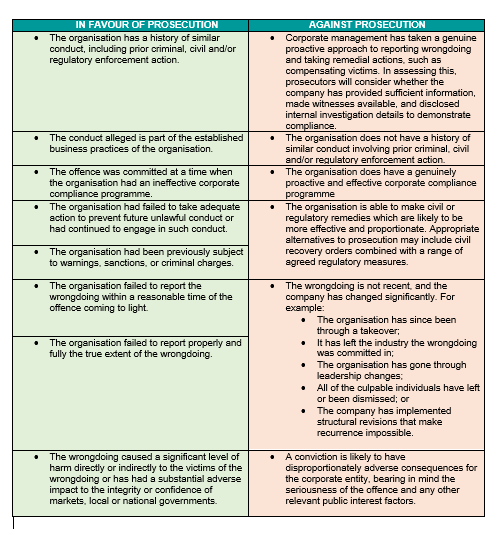

Public Interest Factors

The Joint Guidance also outlines public interest factors both in favour of and against prosecution.[11] The factors highlighted in the Joint Guidance are set out below:

Considering the above factors, it is clear that prosecution authorities expect organisations to adopt a robust approach to compliance from the outset. If not, organisations may struggle to make representations based on the public interest factors against prosecution if they do not have the infrastructure to quickly identify wrongdoing, detect the full extent of misconduct to disclose, report the wrongdoing promptly, or take swift action to limit harm to victims.

Government Guidance

It also recommends that prosecutors may wish to consider calling witnesses to adduce the FTPF Guidance as evidence to help the jury understand the statutory defence.[12]

Consequently, adhering to the FTPF Guidance will be crucial to an organisation if it is investigated. An organisation that can demonstrate it has followed the FTPF Guidance’s prescribed principles may significantly strengthen its defence position, as it will be able to evidence and authenticate the adequacy of its fraud prevention procedures.

The Joint Guidance directs prosecutors to refer to the FTPF Guidance throughout their investigations, including when interviewing witnesses, identifying lines of inquiry, and examining any weaknesses or omissions in an organisation’s prevention procedures.

Footnotes

[1] Section 199 of the Economic Crime and Corporate Transparency Act 2023.

[2] The Crown Prosecution Service, “Organisations must prepare now for new fraud prevention law”.

[3] Criminal offences listed in Schedule 12 of the Economic Crime and Corporate Transparency Act 2023.

[4] Section 2A of the Criminal Justice Act 1987.

[5] Section 202(1) of the Economic Crime and Corporate Transparency Act 2023.

[6] Section 4.3 Associated Persons of the Joint Prosecution Corporate Guidance.

[7] Section 4.3 Associated Persons of the Joint Prosecution Corporate Guidance.

[8] Section 2.5 Territoriality of the Economic Crime and Corporate Transparency Act 2023: Guidance to organisations on the offence of failure to prevent fraud.

[9] Section 6.2 International Investigations and Coordination of the Joint Prosecution Corporate Guidance.

[10] Section 5.1 Charging Strategy: Bribery-Fraud Nexus of the Joint Prosecution Corporate Guidance.

[11] Section 7.1 and 7.2 Charging Corporate Entities- Additional Public Interest Factors to be Considered of the Joint Prosecution Corporate Guidance.

[12] Section 4.4 Reasonable / Adequate Procedures of the Joint Prosecution Corporate Guidance.