i

iOn March 6, 2024, the U.S. Securities and Exchange Commission (SEC) adopted the long-anticipated Climate-Related Disclosure Rules aimed at enhancing transparency and disclosure around climate-related risks and opportunities for U.S. public companies and most foreign private issuers. The SEC received more than 24,000 comments following publication of the proposed rules in March 2022.

While the final rules are meaningfully scaled back from the proposed rules, notably eliminating the proposed requirement to disclose Scope 3 greenhouse gas emissions, the final rules are still some of the most sweeping and controversial ever passed by the SEC. The SEC adopted delayed and staggered compliance dates for the final rules that vary according to the filing status of the registrant. Immediately upon adoption, the final rules were met with lawsuits that challenge their validity and enforceability. While states and businesses claim the new rules go too far, environmental groups say the rules do not go far enough.

Notwithstanding the numerous legal challenges to the Climate-Related Disclosure Rules that could delay or prevent implementation that are described below, companies should consider taking these recommended actions now:

1. Educate Management and the Board

- Consider a presentation to management and the company’s board on the new rules. Do not assume that directors are aware of these rules or their significance to the organization.

2. Assess Climate-Related Disclosure Readiness

- Public companies that have not started to do so already should assess what climate information they have and how it is collected, tracked, measured, and monitored.

- Does the company have the right third-party experts to assist from an auditing and compliance standpoint? In addition to in-house teams, these specialists can help ensure that companies have the appropriate processes in place needed to identify, analyze and disclose all information required by the Climate-Related Disclosure Rules. The costs associated with complying with these rules is anticipated to be significant. We expect that, since many companies will be in the market for the same greenhouse gas (GHG) emissions attestation service providers at the same time, costs may end up being more expensive than for current attestation services.

- Public companies should be aware that the Climate-Related Disclosure Rules will affect their filings with the SEC meaningfully. Companies should begin to assess where and how climate-related disclosures will be presented in annual reports (Form 10-K or 20-F) or in registration statements. Other than the financial statement footnote, the narrative and quantitative disclosures will be tailored for each company. For example, the disclosure may be best accumulated in a new, standalone section identified by the adopting release under the caption “Climate-Related Disclosures”, or a company may prefer to weave in disclosure across existing sections, such as Business, Risk Factors, and MD&A.

- The Climate-Related Disclosure Rules are expected to require significant changes in internal control over financial reporting and disclosure controls and procedures. These changes should be considered now, as public company CEOs and CFOs will be required to certify to the disclosures beginning with the report for the first fiscal quarter of 2025.

- From a governance standpoint, companies should take stock of experience and oversight. Does management have the right mix of experience to assess and manage risk? Which committee has oversight, and are those duties accurately delegated in committee charters? Does the company have an adequate policy for reporting climate-related risks to management, the board or a board committee?

- With respect to a company’s overall ESG approach, companies should review existing statements, goals and targets (whether in SEC reports, CSR reports, on corporate websites, or otherwise), or consider whether to adopt any such goals or targets.

3. Consider the Interplay of the Climate-Related Disclosure Rules With Other Applicable Climate Disclosure Rules

- Public companies should evaluate whether they are required to report climate or related information under other laws, including the three 2023 California climate disclosure laws (Senate Bills 253 and 261 and Assembly Bill 1305) and the EU’s Corporate Sustainability Reporting Directive (CSRD).

4. Continue to Monitor Developments and Other Regulatory and Government Efforts

- While companies do not have the luxury to adopt a wait-and-see approach to see how the lawsuits are resolved, they should nonetheless be mindful of the challenges from both sides. We will keep you abreast of significant developments in this area.

Enhanced Disclosure Requirements

One of the central pillars of the Climate-Related Disclosure Rules is the requirement for companies to provide comprehensive disclosure regarding their climate-related risks and opportunities. This includes detailing the effect of climate change on their business operations, financial performance, and strategies for mitigating associated risks. Some key disclosure items are:

- New Subpart 1500 – Climate-Related Disclosure in Regulation S-K

- Greenhouse Gas Emissions:

- Scope 1 and 2 emissions will be required, “if such emissions are material,” for registrants that qualify as a large accelerated filer (LAF) or an accelerated filer (AF). Smaller reporting companies and emerging growth companies are exempt from this disclosure requirement.

- Compared to the proposal, the final rules modified the proposed assurance requirement covering Scope 1 and Scope 2 emissions for AFs and LAFs by extending the reasonable assurance phase in period for LAFs and requiring only limited assurance for AFs.

- Meaningfully, the SEC eliminated the proposed requirement to provide Scope 3 emissions disclosure, which the proposal would have required in certain circumstances. Scope 3 emissions are indirect greenhouse gas (GHG) emissions by the various components of a company’s supply chain. The EPA describes Scope 3 emissions as follows: “Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly affects in its value chain. Scope 3 emissions include all sources not within an organization’s scope 1 and 2 boundary. The scope 3 emissions for one organization are the scope 1 and 2 emissions of another organization. Scope 3 emissions, also referred to as value chain emissions, often represent the majority of an organization’s total greenhouse gas (GHG) emissions.”

- Governance:

- The SEC eliminated the proposed requirement to describe board members’ climate expertise.

- New Item 1501(a) of Reg. S-K states, “If there is a climate-related target or goal disclosed pursuant to [Item 1504 of Reg. S-K] or transition plan disclosed pursuant to [Item 1502(e)(1) of Reg. S-K], describe whether and how the board of directors oversees progress against the target or goal or transition plan.”

- New Item 1501(b) of Reg. S-K states, “Describe management’s role in assessing and managing the registrant’s material climate-related risks.”…

- In providing such disclosure, provide …. “the relevant expertise of such [management positions or committees responsible for assessing and managing climate-related risks] in such detail as necessary to fully describe the nature of the expertise”

- New Item 1504(a) of Reg. S-K states, “A registrant must disclose any climate-related target or goal if such target or goal has materially affected or is reasonably likely to materially affect the registrant’s business, results of operations, or financial condition.”

- Greenhouse Gas Emissions:

- New Subpart 14 of Regulation S-X

- In a new footnote to the audited financial statements:

- “[If meeting the disclosure threshold described below], disclose the aggregate amount of expenditures expensed as incurred and losses, excluding recoveries, incurred during the fiscal year as a result of severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures, and sea level rise. For example, a registrant may be required to disclose the amount of expense or loss, as applicable, to restore operations, relocate assets or operations affected by the event or other natural condition, retire affected assets, repair affected assets, recognize impairment loss on affected assets, or otherwise respond to the effect that severe weather events and other natural conditions had on business operations.” (emphasis added)

- Disclosure will be required only when and if the aggregate amount of expenditures expensed as incurred and losses equals or exceeds one percent of the absolute value of income or loss before income tax expense or benefit for the relevant fiscal year (i.e., not required if less than $100,000). (emphasis added)

- Also, “[d]isclose whether the estimates and assumptions the registrant used to produce the consolidated financial statements were materially impacted by exposures to risks and uncertainties associated with, or known impacts from, severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures, and sea level rise, or any climate-related targets or transition plans disclosed by the registrant. If yes, provide a qualitative description of how the development of such estimates and assumptions were impacted by such events, conditions, targets, or transition plans.”

- In a new footnote to the audited financial statements:

Materiality Assessment

The Climate-Related Disclosure Rules emphasize the importance of materiality in climate-related disclosures and, in a departure from the proposed rules, the final rules are generally less prescriptive and include additional materiality qualifiers for certain climate risk disclosures. With respect to GHG disclosures, even if the registrant is confident its GHG emissions are not material, it appears that the SEC expects them to be tracked in order to make such a determination, and such tracking will need to be covered by disclosure controls and procedures maintained in accordance with the Sarbanes-Oxley Act of 2002.

Integration into Reporting Frameworks

The adopting release acknowledges that, where consistent with the SEC’s objectives and the authority Congress granted, certain provisions in the new rules are similar to existing reporting frameworks, such as the Task Force on Climate-related Financial Disclosures (TCFD) recommendations and the World Business Council for Sustainable Development and World Resources Institute Greenhouse Gas Protocol (GHG Protocol). The adopting release states that “[t]he TCFD framework focuses on matters that are material to an investment or voting decision and is grounded in concepts that tie climate-related risk disclosure considerations to matters that may affect the results of operations, financial condition, or business strategy of a registrant.” Accordingly, to streamline reporting and ensure consistency, the SEC encourages companies to align their climate disclosures with these existing frameworks.

The SEC also anticipates that because many companies already adhere to TCFD standards, leveraging those “reporting frameworks will mitigate those registrants’ compliance burdens and help limit costs.” This alignment should facilitate comparability and allow investors to better evaluate companies’ climate-related performance.

The adopting release also summarizes competing reporting regimes, including ISSB standards (which some foreign jurisdictions have adopted or plan to adopt); the European Union’s Corporate Sustainability Reporting Directive; California’s Climate-Related Financial Risk Act, which requires all U.S. companies that do business in California with over $500 million in annual revenues to make certain climate-related disclosures; and California’s Climate Corporate Data Accountability Act, which requires U.S. companies that do business in California with over $1 billion in annual revenues to disclose GHG emissions.

The SEC notes that the other laws and regulations may overlap with its climate change rules, could reduce compliance and cost burdens, and require separate disclosure outside of the SEC’s public disclosure regime.

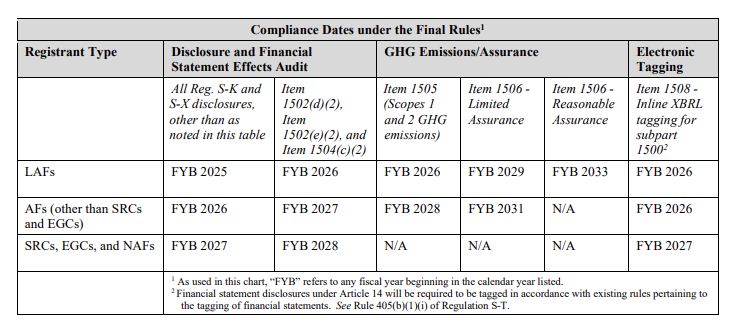

Compliance Timeline

This table on compliance dates was included in the adopting release:

For example, an LAF with a Dec. 31 fiscal year end will not be required to comply with the climate disclosure rules (other than those pertaining to GHG emissions and those related to Reg. S-K Item 1502(d)(2), Item 1502(e)(2), and Item 1504(c)(2), if applicable) until its Form 10-K for fiscal year ended December 31, 2025, due in March 2026. If required to disclose its Scopes 1 and/or 2 emissions, such a filer will not be required to disclose those emissions until its Form 10-K for fiscal year ended Dec. 31, 2026, due in March 2027, or in a registration statement that is required to include financial information for fiscal year 2026. Such emissions disclosures would not be subject to the requirement to obtain limited assurance until its Form 10-K for fiscal year ended Dec. 31, 2029, due in March 2030, or in a registration statement that is required to include financial information for fiscal year 2029.

The registrant would be required to obtain reasonable assurance over such emissions disclosure beginning with its Form 10-K for fiscal year ended Dec. 31, 2033, due in March 2034, or in a registration statement that is required to include financial information for fiscal year 2033. If required to make disclosures pursuant to Reg. S-K Item 1502(d)(2), Item 1502(e)(2), or Item 1504(c)(2), such a filer will not be required to make such disclosures until its Form 10-K for fiscal year ended Dec. 31, 2026, due in March 2027, or in a registration statement that is required to include financial information for fiscal year 2026.

As an accommodation, the final rules provide that any GHG emissions metrics required to be disclosed pursuant to Item 1505 in an Annual Report on Form 10-K may be incorporated by reference from the registrant’s Form 10-Q for the second fiscal quarter in the fiscal year immediately following the year to which the GHG emissions disclosure relates, or may be included in an amended annual report on Form 10-K no later than the due date for such Form 10-Q. The extension of the deadline for the filing of GHG emissions metrics also applies to the deadline for the filing of an attestation report, which should accompany the GHG emissions disclosure to which the report applies.

The SEC stated in its adopting release that this additional time – an additional two fiscal quarters – should provide registrants subject to Item 1505 and their GHG emissions attestation providers with sufficient time to measure GHG emissions, provide assurance, and prepare the required attestation report. The final rules provide that a registrant that elects to incorporate by reference its attestation report from its Form 10-Q for the second fiscal quarter or to provide its attestation report in an amended annual report must include an express statement in its Annual Report on Form 10-K indicating its intention to either incorporate by reference the attestation report from a quarterly report on Form 10-Q or amend its annual report to provide the attestation report by the due date specified in Item 1505.

Legal Challenges

Immediately after the SEC released the new rules, 10 states (Alabama, Alaska, Georgia, Indiana, New Hampshire, Oklahoma, South Carolina, Virginia, West Virginia and Wyoming) brought an action in the U.S. Court of Appeals for the Eleventh Circuit arguing that the SEC’s Climate Rules exceed the agency’s authority and are arbitrary, capricious, an abuse of discretion, and not in accordance with law. The states asked the court to declare the new rules unlawful and vacate the SEC’s Climate Rules.

Since then, eight more cases have been filed in the Second, Fifth, Sixth, Eighth, Eleventh and District of Columbia circuits by Republican attorneys General, oil and gas industry groups, and environmental advocacy organizations. While petitioners generally chose to file in circuits that they perceived as sharing their political perspective, following a request by the SEC on March 19, the Judicial Panel on Multidistrict Litigation conducted a lottery and the Eighth Circuit was selected to hear all of the consolidated cases.

On March 15, on motion of petitioners Liberty Energy Inc. and Nomad Proppant Services LLC, the Fifth Circuit granted an administrative stay of the rules pending review. It is anticipated that this stay will remain in effect at least until the cases are consolidated in a single circuit. If a court other than the Fifth Circuit is chosen, that court can determine whether to maintain or dissolve the stay.

Based on public comments and statements since the final climate rule was approved by the SEC, the bases for some substantive challenges by attorneys general and business interests are likely to include the Administrative Procedures Act (the APA) (i.e., the rule is arbitrary and capricious, and contrary to law); the rule exceeds the SEC’s statutory rulemaking authority: the Major Questions Doctrine (climate disclosures are matters of “vast economic and political significance” and there is no clear Congressional authorization to regulate them); and the First Amendment (i.e., the required disclosures are unconstitutional speech).

Similar arguments doomed the SEC’s issuer share repurchase rules, which were vacated at the end of 2023. Depending on the decisions the Supreme Court makes later this term on pending cases challenging the Chevron deference, these petitioners may also be in a position to assert that no deference is due to the SEC decision, and that the reviewing court has the power to weigh the evidence in the record on its own.

At the other end of the spectrum, the Natural Resources Defense Council and the Sierra Club, which filed petitions in the Second Circuit and D.C. Circuit, respectively, are planning to argue that the climate rule does not go far enough, Both are expected to argue that the SEC’s decision to drop Scope 3 disclosures from the final rule and soften Scope 1 and 2 disclosure requirements does not satisfy the SEC’s obligations to protect investors and provide them with the information they need to manage climate-related financial risks.

Of no small interest, all of the petitioners may pursue the same kind of procedural challenge that was suggested by dissenting SEC Commissioners Hester Pierce and Mark Uyeda in their comments prior to the March 6 vote on the new rules. In short, the changes made from the proposed rule were so substantial that instead of going final, under the APA the SEC was required to give the public adequate notice of those changes and another opportunity to comment.